Introduction

Background

Corporate income tax is a large contributor to the State’s General Fund. The three largest sources of revenue to the General Fund are personal income taxes, sales and use taxes, and corporate income taxes. The Corporation Tax Law, which is administered by the Franchise Tax Board (tax board), generally requires corporations doing business in California to pay taxes to the State on a percentage of their net income. As shown in Table 1, the State received more than $7 billion in tax revenue from corporations in fiscal year 2012–13. Certain exceptions to the normal tax structure, referred to as corporate income tax expenditures (tax expenditures), substantially reduced this revenue. As detailed in the Appendix, this forgone revenue totaled more than $5 billion in fiscal year 2012–13.2

| Source of Funds | Amount Collected (in billions) | Percentage of Total Contributions |

|---|---|---|

| Personal income taxes | $66.2 | 67% |

| Sales and use taxes | 20.4 | 20 |

| Corporate taxes | 7.3 | 7 |

| Other sources* | 5.5 | 6 |

| Totals | $99.4 | 100% |

Source: State of California Comprehensive Annual Financial Report for Year Ended June 30, 2013.

* Other sources include insurance taxes, permits, fees, and other sources of revenue.

Tax Expenditures Explained

According to the U.S. Government Accountability Office (GAO), tax expenditures are exceptions to the normal tax structure that can have the same effect as government spending programs. Tax expenditures can include credits, deductions, exclusions, and exemptions, as shown in Table 2. They are available for both individuals and corporations, and they reduce taxpayers’ overall tax liability while encouraging certain behaviors. For example, California exempts corporations from the minimum franchise tax in their first year of operation, and is intended to improve the State’s business climate and encourage new businesses to incorporate. However, tax expenditures also limit the amount of revenue the State collects, and they represent a significant amount of forgone state revenue.

| Tax Expenditure | Description | Examples |

|---|---|---|

| Credit | Reduces tax liability dollar for dollar. Additionally, some credits are refundable, meaning that a credit in excess of tax liability results in a cash refund. | The state research and development credit allows taxpayers to claim a credit for increases in their current‑year research and development expenses relative to sales. |

| Deduction | Reduces gross income due to expenses taxpayers incur. | Taxpayers may be able to deduct state and local income taxes and property taxes from federal income taxes. |

| Deferral | Delays recognition of income or accelerates some deductions otherwise attributable to future years. | Taxpayers may defer paying taxes on interest earned on certain savings bonds until the bonds are redeemed. |

| Election | Allows taxpayers to choose between two or more tax treatments. | The State allows corporations to elect to compute income attributable to the State based on domestic sources rather than on worldwide sources. |

| Exclusion | Excludes income that would otherwise constitute part of a taxpayer’s gross income. | Employees generally pay no income taxes on contributions their employers make on their behalf for medical insurance premiums. |

| Exemption | Reduces gross income for taxpayers because of their status or circumstances. | Qualifying nonprofit and charitable organizations may be exempt from corporate income taxes. |

| Preferential tax rate | Reduces tax rates on some forms of income. | Capital gains on certain income are subject to lower tax rates under the federal individual income tax. |

Source: Government Accountability Office’s report Tax Expenditures: Background and Evaluation Criteria and Questions and the Franchise Tax Board’s 2010 income tax expenditures report.

Tax expenditures can be advantageous for the State in advancing policy objectives, and they are advantageous for corporations as they reduce tax liability. For example, the low‑income housing credit provides funds to developers to make more low‑income housing projects financially feasible. Additionally, the Legislative Analyst’s Office (LAO) found that tax expenditures can require little administrative effort as the State often has no need to hire employees and maintain the equipment and facilities required to administer a public program.

However, many tax expenditures are subject to limited legislative oversight and budgetary control, making it difficult to determine whether they are cost‑effectively achieving their objectives. The State does not directly administer some of the tax expenditures it authorizes. According to the LAO, for some tax expenditures, hard data are limited, so measuring whether they are cost‑effective is made more difficult by problems in identifying their direct impacts and uncertainty about the behavioral effects they can produce. Furthermore, according to the GAO, if a tax expenditure has no effect on taxpayer behavior, the taxpayer gets a windfall savings for activity that would have occurred without the tax expenditure. For example, the California Film Commission found that from 2010 through 2015, some projects that applied for credits but did not receive them still incurred some production spending in the State. Had these projects been awarded credits, they might have received a benefit for activity that they would have done even without the incentive.

Our Review of Six State‑Only Corporate Income Tax Expenditures

We reviewed the six largest state‑only corporate income tax expenditures. From the three most recent tax expenditure reports by the Department of Finance (Finance), we selected the six tax expenditures with the highest forgone revenue that were at least partially unique to the State, that had at least three years of tax data available, and that the Legislature had not yet either repealed or allowed to sunset. These six tax expenditures, which are described in Table 3, are still in effect and have existed long enough to provide several years of data so we could provide a more meaningful analysis to the Legislature.

| Tax Expenditure Provision | Purpose | Forgone Revenue In Fiscal Year 2012–13 (in millions) |

|---|---|---|

| Research and development (R&D) credit | To increase R&D activity undertaken in California | $1,500 |

| Water’s edge election | To provide corporations an option not to be subject to tax on their worldwide income | 700 |

| Subchapter S corporation election | To simplify the tax preparation process by conforming with federal legislation and to allow state businesses to be competitive with those located elsewhere | 220 |

| Film and television credit | To increase production spending, jobs, and tax revenues in the State | 100 |

| Low‑income housing credit | To fund low‑income housing in the State that would otherwise not have been economically viable | 50 |

| Minimum franchise tax exemption* | To encourage new businesses to incorporate in the State | 45 |

| Total | $2,615 |

Sources: California State Auditor’s analysis, the tax expenditure report by the Department of Finance (Finance) for fiscal year 2014–15, and information obtained from the Franchise Tax Board.

* In its tax expenditure reports, Finance refers to this tax expenditure as the tax exempt status for qualifying corporations but includes forgone revenue from organizations deemed tax‑exempt by Internal Revenue Code Section 501, such as churches and nonprofits. We have only included forgone revenue from corporations claiming the exemption. This amount is for calendar years because this amount is derived from new corporations formed each calendar year. For added clarity, we also refer to this tax expenditure as the minimum franchise tax exemption.

Research and Development Credit

The research and development (R&D) credit allows corporations to claim a portion of their R&D expenses as a credit, which reduces their tax liability, based on the amount they spent on R&D conducted in California. The state R&D credit is modeled after a federal R&D credit, but the state credit allows some taxpayers to use a different method for calculating the amount of the credit the corporation can claim.

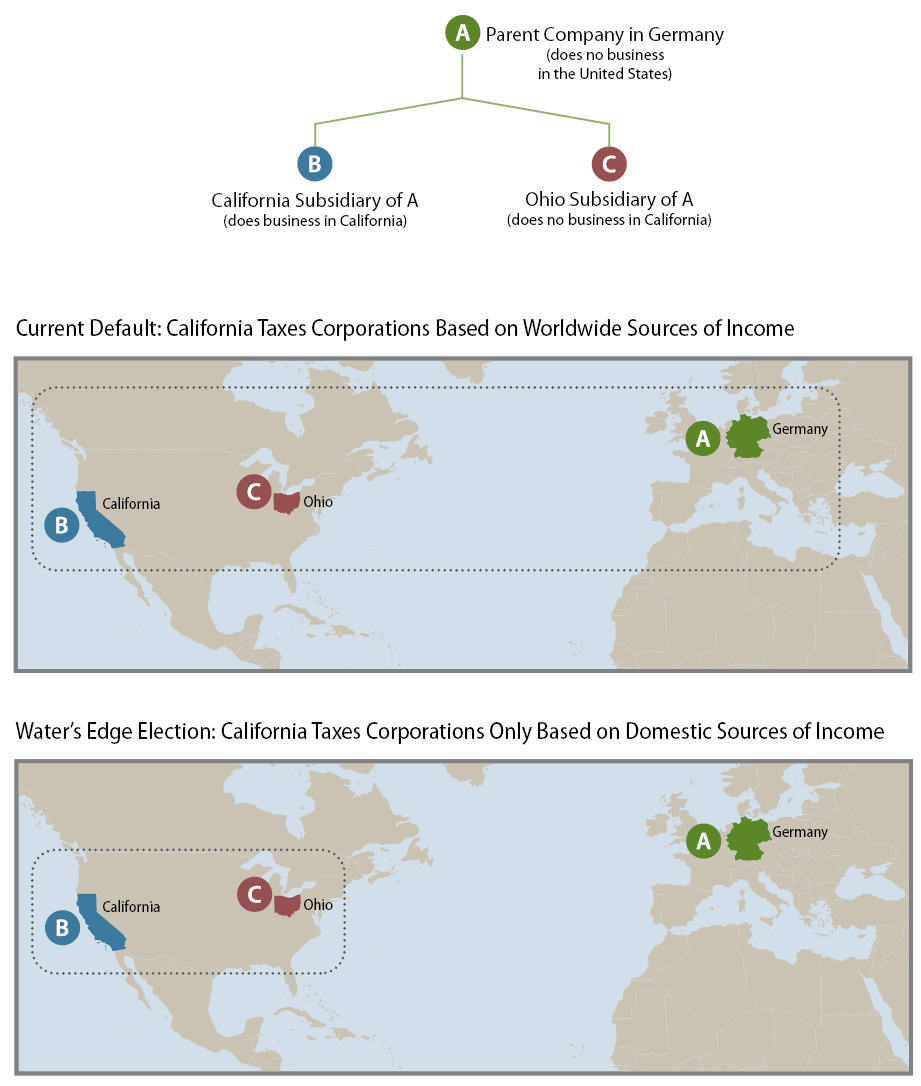

Water’s Edge Election

The water’s edge election allows multinational corporations to limit their taxable base to income derived from sources within the United States—which excludes earnings or losses from foreign portions of their business. As shown in Figure 1, the water’s edge election allows corporations that choose this tax expenditure generally to include only income from their domestic corporations to determine what income is subject to California tax. According to the tax board, the water’s edge election was enacted in response to controversy that arose over the application of the worldwide unitary tax business concept to multinational corporations. Worldwide unitary taxation requires corporations to pay a tax based on income derived from or attributable to sources within California that is earned by the corporations’ combined business units, which include all subsidiaries and parent companies regardless of their location.

Subchapter S Corporation Election

The Subchapter S corporation (S corporation) election offers businesses an alternative to the standard Subchapter C corporation (C corporation) filing status. Like C corporations, S corporations are legal entities that are generally separate and distinct from their owners, and with separate and distinct liabilities. Additionally, S corporations are limited to 100 shareholders who must be United States residents. California S corporations are taxed at a lower entity rate than C corporations, and S corporations pass income through to their shareholders, who may be subject to personal income taxes on those distributions.

Figure 1

California Department of Transportation Maintenance Program Funding Allocation for Fiscal Year 2014–15 (in Millions)

* Administration program costs are the indirect costs of a program, typically a share of the costs of the administrative units serving the entire department (for example, legal, personnel, and accounting). Distributed administration costs represent the distribution of the indirect costs to the various program activities of the department.

† Highway maintenance includes $231.7 million for major maintenance pavement contracts and $50.6 million for storm water discharge, appropriated separately in the Budget Act of 2014.

Film and Television Credit

The film and television credit is intended to encourage film and television production in California by providing credits to production companies seeking to film in the State. The credit was first enacted in 2009 and was given to production companies on a first‑come, first‑served basis. The newer version of the credit, implemented in fiscal year 2015–16, is equal to up to 25 percent of qualified production spending, including purchases and rental of supplies used on a film production set and payment of specified wages. The California Film Commission must award the credits on a competitive basis, and it collects data on corporations that apply for the credit.

Low‑Income Housing Credit

The low‑income housing credit provides funding for developers—those that rehabilitate existing housing or construct new projects—to construct low‑income housing in the State, and the state credit generally requires developers to use it in conjunction with a federal low‑income housing credit. Both the state and federal credits cover funding shortfalls for such projects, and state law specifies that the combined state and federal credits must not cover more expenses than needed to make the projects economically viable. The California Tax Credit Allocation Committee is required to administer both credits, to award them on a generally competitive basis, and to oversee previously awarded projects for continued compliance.

Minimum Franchise Tax Exemption

Corporations are generally required to pay the minimum franchise tax of $800. The minimum franchise tax exemption exempts every corporation that incorporates or qualifies to do business in California on or after January 1, 2000, from paying the minimum franchise tax for its first taxable year.

Scope and Methodology

The Joint Legislative Audit Committee (audit committee) directed the California State Auditor to perform an audit of state‑only corporate income tax expenditures. Table 4 outlines the audit committee’s objectives and our methods for addressing them.

| Audit Objective | Method | |

|---|---|---|

| 1 | Review and evaluate the laws, rules, and regulations significant to the audit objectives. | We reviewed federal and state statutes and regulations related to the corporate tax expenditures identified in the 2014–15 tax expenditure report by the Department of Finance (Finance). |

| 2 | For a selection of at least the six largest state‑only corporate tax expenditures, as identified in Finance’s tax expenditure report during the last three fiscal years, to the extent possible, perform the following: | We reviewed Finance’s three most recent tax expenditure reports and selected the six largest state‑only corporate tax expenditures using tax data from fiscal years 2010–11 to 2012–13 obtained from the Franchise Tax Board (tax board). According to the tax board, these data are the most up‑to‑date information available. We compared Finance’s tax expenditure reports with data obtained from the tax board to verify its accuracy. |

| a. Identify the purpose of the corporate tax expenditures as outlined in state law and determine whether these tax expenditures are fulfilling their intended purpose. | We identified each corporate tax expenditure’s purpose by reviewing authorizing statutes, committee documents from bills enacting the authorizing statutes, and information from other sources. We interviewed staff at the agencies responsible for administering the corporate tax expenditures. We analyzed this information to determine whether the tax expenditures were achieving their purposes. | |

| b. Determine whether administering state agencies or other groups have performed any cost‑benefit studies assessing the effectiveness, benefits, or both to the state economy of the selected corporate tax expenditures. | We identified and reviewed studies performed by administering state agencies and others to determine the effectiveness and benefits to the state economy of the tax expenditures we selected for review. | |

| c. Determine whether certain types of corporate tax expenditures appear to be more effective or beneficial to the State’s economy than others. | We reviewed each of the six corporate tax expenditures we selected for review to compare their effectiveness and benefits to the state economy. We reviewed the structures put in place by other states to monitor the effectiveness of their corporate tax expenditures and determined whether California has similar processes. |

|

| d. Determine the impact on the State of placing a cap on each selected corporate tax expenditure. | To determine the advantages and disadvantages of capping tax expenditures, we conducted a review of research literature published by government agencies and other groups and interviewed staff from agencies responsible for administering the tax expenditures we selected for review. | |

| 3 | Review and assess any other issues that are significant to the audit. | We reviewed corporate tax expenditure legislation introduced in 2015 to determine whether the bills include language specifying goals, purposes, and objectives that the tax expenditures are intended to achieve as well as performance indicators, including data collection requirements and reasonableness determinations. |

Source: California State Auditor’s planning documents and analysis of information and documentation identified in the column titled Method.

Assessment of Data Reliability

The GAO, whose standards we are statutorily required to follow, requires us to assess the sufficiency and appropriateness of computer‑processed information that we use to support our findings, conclusions, or recommendations. The tax board gives forgone revenue data and estimates to Finance annually so Finance can prepare its tax expenditure report. We used Finance’s fiscal year 2012–13, 2013–14, and 2014–15 reports to select the six largest state‑only tax expenditures for the most recent three years that tax data were available. In performing this audit, we obtained data from the tax board’s Business Entity Tax System to determine whether the data Finance relied on in compiling its reports were accurate. However, for three of the six tax expenditures we selected, this information was not in the Business Entity Tax System but rather constituted estimates the tax board created by making adjustments to historical tax information. We reviewed the methodologies underlying these estimates and found them to be reasonable.

We tested the accuracy of data extracts from the tax board’s Business Entity Tax System for the remaining three tax expenditures by tracing key data elements to corporate tax records from tax years 2010 through 2012. We found no errors. We were unable to test the completeness of these data extracts because tax records are submitted in both paper and electronic formats. Ultimately, we found these data to be of undetermined reliability for the purpose of this audit. Although this determination may affect the precision of the numbers we present, we believe there is sufficient evidence in total to support our audit findings, conclusions, and recommendations.

Footnotes

2 According to the Department of Finance, the total amount of forgone revenue to these corporate tax expenditures does not necessarily reflect revenue the State would recover if it eliminated them because of the complicating factors of tax law interactions and taxpayer behavioral responses. Go back to text