Audit Results

The State Could Improve the Effectiveness of Corporate Income Tax Expenditures by Implementing Best Practices From Other States

Adopting methods that other states use to oversee their corporate income tax expenditures (tax expenditures) could improve the effectiveness of the State’s current and future tax expenditures. As part of our audit, we reviewed how other states oversee these expenditures, and we identified best practices not consistently followed in California. Unlike other forms of direct government spending, which come under legislative oversight during the annual budget process, tax expenditures may go many years without state evaluation; in addition, the amount of forgone revenue is not typically limited. As shown in Table 5, adopting the best practices for tax expenditure oversight would provide the Legislature with more information and a better account of the effectiveness and impact of tax expenditures. These practices include the use of clearly stated policy objectives to define the Legislature’s purpose in enacting the tax expenditures, performance metrics to allow the Legislature to measure their effectiveness, sunset provisions to prompt legislative review and allow the Legislature to more easily modify or repeal them if necessary, and an evaluation process that creates recommendations that tie back to the Legislature’s policymaking process. By following best practices for tax expenditure oversight, the State can improve the effectiveness of tax expenditures, and such improvements would reduce the risk of not achieving the public purposes intended and forgoing needed revenue.

Corporate Income Tax Expenditure Legislation Does Not Consistently Include Policy Goals, Performance Metrics, or Sunset Provisions

The State does not consistently define the purposes of its tax expenditures or create specific metrics to measure their performance. To create a foundation for stronger oversight, all tax expenditures should include measurable policy objectives and corresponding performance measures. Measurable policy objectives should explicitly provide the tax expenditure’s intended effects, while performance measures should define how the State will evaluate whether the tax expenditure is achieving its purpose. Having this foundation in place will prevent the kind of problems we found with some of the tax expenditures we reviewed.

| Best Practice | Example of How a State Implemented the Best Practice | Implementation in California |

|---|---|---|

| Clearly define and periodically update measurable policy objectives. | Vermont lawmakers adopted goals for certain tax expenditures and required all future tax expenditures to include a clearly stated purpose. | The Legislature passed a law in 2014 requiring all new tax credit bills to include specific goals, purposes, and objectives, and detailed performance indicators that measure whether the tax credit meets its goals, purposes, and objectives. However, this requirement is limited only to tax credits and is not always followed. |

| Establish performance measures to help monitor the effectiveness of all tax expenditures. | Washington passed a law in 2013 requiring every new tax expenditure bill to include a performance statement that specifies a legislative purpose and performance metrics to allow the legislature to measure its effectiveness. | |

| Establish sunset dates for tax expenditures to encourage reviews. | Oregon passed a bill in 2009 to assign sunset dates to many tax credits and designated a default sunset date of six years after the effective date of new tax credits, unless stated otherwise. | California does not always establish sunset dates for tax expenditures and does not have systematic sunset laws for all tax expenditures. |

| Require comprehensive, systematic evaluations of all tax expenditures by a state entity with the necessary resources for analysis. | Under state law enacted in 2006, Washington’s Joint Legislative Audit and Review Committee evaluates some of the state’s tax expenditures over a 10‑year schedule that the state’s Citizens Commission for Performance Measurement of Tax Preferences developed. | California does not have a process to systematically evaluate the effectiveness of its tax expenditures. Some evaluations are conducted for individual tax expenditures when required by law or on an ad hoc basis, but no state agency reviews all tax expenditures over a defined time frame. |

| Develop policy‑relevant conclusions and recommendations to continue, modify, or repeal each tax expenditure, and connect results to the policymaking process. | Maryland established a legislative evaluation committee in 2012 responsible for evaluating tax incentives and recommending whether incentives should be continued, modified, or ended. For example, staff reported on Maryland’s Enterprise Zone tax credit and found that it was not effective in creating jobs for zone residents who are chronically unemployed or live in poverty, and recommended that changes be made to better meet the needs of unemployed job seekers in the enterprise zone. |

Sources: California State Auditor’s analysis of California and other states’ laws, and reports from the U.S. Government Accountability Office, the Pew Charitable Trusts, and the Institute for Taxation and Economic Policy.

State law requires certain tax expenditure legislation to include policy goals and performance metrics. In 2014 the Legislature enacted Section 41 of the Revenue and Taxation Code (Section 41), which requires bills introduced on or after January 1, 2015, that authorize a new income tax credit to include specific information that can satisfy what we consider to be a best practice for such legislation. Section 41 only applies to bills authorizing new income tax credits, and it does not apply to legislation proposing other types of tax expenditures, such as exemptions and elections. Section 41 requires new income tax credit bills to include specific goals, purposes, and objectives that the credit will achieve as well as detailed performance indicators and data collection requirements so that the Legislature can gauge how effectively the credit meets the goals, purposes, and objectives. However, California courts have consistently stated that because the Legislature may modify or abolish laws such as Section 41, one legislative body may not limit or restrict its own power or that of subsequent legislatures. In fact, only two of the nine bills introduced in 2015 that proposed new corporate income tax credits included policy objectives and performance measures to gauge the effectiveness of the credits, as required by Section 41.3 The seven bills that did not include that information and were silent regarding these requirements, stated that the credits authorized by the bills were allowed notwithstanding Section 41, or stated the Legislature’s intent to enact the provisions required by Section 41. These bills illustrate several methods that legislators may employ to modify—and effectively negate—the requirements of Section 41. Nevertheless, we believe that to enable better oversight, the Legislature should consistently provide policy objectives and performance measures for all types of newly proposed corporate income tax expenditures, including tax credits.

One way to increase the likelihood that future legislatures will include specific provisions in tax expenditures and periodically review them is for the Legislature to enact a joint legislative rule requiring this best practice and a vote of the Legislature to modify the requirement. Joint rules can bind the way a legislator behaves. For example, the Joint Rules of the Senate and Assembly for the 2015–16 Regular Session (2015–16 joint rules) contain numerous provisions governing the contents of bills, including a rule that requires that a bill amending more than one section of existing law contain a separate section for each section amended. Another 2015–16 joint rule prohibits a bill from adding a title that names a current or former member of the Legislature. The 2015–16 joint rules also specify that, unless otherwise provided, a two‑thirds vote of each house of the Legislature is required to dispense with a joint rule. In contrast, each of the new corporate income tax expenditure bills introduced in 2015 that we reviewed required only a majority vote of the Legislature for passage. Therefore, a two‑thirds vote to dispense with a joint rule containing requirements similar to those in Section 41 might have increased the likelihood that all of these bills contained the goals and performance metrics required by Section 41.

Another best practice not consistently included in the California tax expenditures we reviewed is a sunset provision, which can limit the time the tax expenditures are applicable. Specifically, the Legislature did not include sunset provisions in three of the nine tax credit bills it introduced in 2015. Sunset provisions allow the Legislature to review and more easily modify or repeal tax expenditures, which otherwise may go many years without evaluation. Inclusion of a sunset provision prompts the Legislature to review periodically a tax expenditure’s effectiveness and actively decide whether it should be renewed in its current form, allowed to continue with modifications, or allowed to expire because it is not performing as expected. For example, in 2009 Oregon enacted a law that assigned a default repeal date of six years for any new tax credit. By consistently including a sunset provision, the Legislature can better ensure that all tax expenditures receive evaluations and require legislative action for them to continue.

The State Does Not Conduct Regular Comprehensive Reviews of Corporate Income Tax Expenditures

Two other best practices not currently required by the State would improve oversight of tax expenditures: requiring a state entity to periodically conduct comprehensive evaluations of tax expenditures and tasking a legislative body with reviewing those evaluations and providing conclusions and recommendations to the Legislature. By requiring periodic reviews of tax expenditures and then connecting the reviewing entities’ conclusions and recommendations to the policymaking process, the Legislature would create a valuable tool that could improve tax expenditures and reduce the risks of tax expenditures not achieving their intended purposes and forgoing needed revenue.

California’s efforts to review tax expenditures have been sporadic. In 1985 the Legislature enacted a resolution that directed the Legislative Analyst’s Office (LAO) to review all state tax expenditures and produce a report every two years. However, in 1990, Proposition 140 limited the Legislature’s budget, which, according to the chief deputy legislative analyst, significantly reduced the office’s staff. Although the LAO continues to review specific tax expenditures as the law requires and as the Legislature requests, it discontinued its periodic reporting on all tax expenditures. Additionally, although the current tax expenditure reports issued by the Department of Finance and the Franchise Tax Board (tax board) provide useful compilations of tax expenditure data, these entities are not required to evaluate their effectiveness or to draw conclusions or make recommendations related to each tax expenditure.

Washington State has integrated many of the best practices for tax expenditure oversight through its Citizen Commission for Performance Measurement of Tax Preferences (tax preference commission). Established in 2006, the tax preference commission consists of five voting members appointed by Washington’s legislature and governor, and two nonvoting members, the Washington State Auditor and the chair of that state’s Joint Legislative Audit and Review Committee. Washington’s Joint Legislative Audit and Review Committee is tasked with advising the tax preference commission and making recommendations to continue, modify, or repeal tax expenditures. The tax preference commission must review certain tax expenditures at least once every 10 years and allow public comments during its deliberation. In doing so, the tax preference commission must consider the tax expenditure’s public policy objectives, evidence whether the tax expenditure is fulfilling its objectives, any unintended consequences of the tax expenditure, its fiscal and economic impacts, and any other relevant factors regarding the tax expenditure.

In 2012 Washington’s tax preference commission reviewed 26 tax expenditures and recommended that the legislature review and clarify the purpose of five, that it eliminate seven, and that it continue 14 without modification. For example, the tax preference commission determined that Washington’s high‑technology research and development (R&D) credit was not creating jobs in a cost‑effective manner and recommended that the legislature allow the credit to expire. According to the tax preference commission, Washington’s legislature ultimately implemented some of its recommendations. For example, as of December 2015, the legislature reviewed and clarified one tax expenditure and allowed the high technology R&D credit to expire.

By establishing an evaluation process for tax expenditures and connecting it with legislative hearings as Washington does, California could improve its oversight of corporate tax expenditures, and this improvement would lead to more informed decisions about whether to continue, modify, or repeal tax expenditures. Moreover, this enhanced oversight would also provide better assurance that the State is receiving the value it expects from these expenditures.

It Is Unclear Whether Two Tax Expenditures Are Fulfilling Their Purposes Because Sufficient Evidence and Effective Oversight Are Lacking

Because no state entities oversee or regularly evaluate the R&D credit or the minimum franchise tax exemption (franchise exemption), we found insufficient evidence to determine whether these tax expenditures are fulfilling their purposes. Economic literature provides conflicting evidence on the effectiveness of state‑level R&D credits for stimulating additional state R&D activity or on how well small state‑level tax reductions, like the franchise exemption, affects such economic activity as business formation. Without appropriate evidence to confirm their effectiveness, it is not clear whether the amount of forgone revenue associated with these tax expenditures—$1.5 billion alone for the R&D credit in fiscal year 2012–13—is being well used or whether it could be better allocated to fulfill the same or similar policy objectives.

Evidence Supporting the Effectiveness of the Research and Development Credit Is Mixed

We were unable to determine the R&D credit’s effectiveness because no state entity oversees or regularly evaluates it. The R&D credit is intended to encourage R&D activity by allowing corporations to claim a portion of their R&D expenses as a credit against their tax liability. Although the tax board audits corporations to ensure that they are properly documenting the expenses they use to claim the credit, it is difficult to determine how much R&D activity results from the credit. Further, although the R&D credit is the State’s largest corporate income tax expenditure, its effectiveness is not regularly evaluated. The credit was last reviewed in 2003 by the LAO, which determined that the tax expenditure is likely costly relative to the benefits it provides, but the LAO was unable to estimate more precisely the costs and benefits. With no in‑depth analysis, insufficient evidence exists to determine whether and how effectively the R&D credit is fulfilling its purpose or benefitting the state economy.

Most of the R&D credits are claimed by large corporations, and those corporations have generated billions in unused credits that represent a large future liability for the State. As shown in Table 6, in 2012, the State’s largest corporations claimed 85 percent of the R&D credits. Further, those corporations are allowed to carry their unused R&D credits forward indefinitely to offset future tax liabilities. The tax board estimates indicate that corporations generated but did not claim more than $2.7 billion in R&D credits in tax year 2012. Moreover, since the credit’s inception in 1987, the tax board estimates that corporations have generated but not claimed more than $14 billion in credits. These unclaimed credits potentially represent a large future liability for the State. However, because no state agency has evaluated the appropriateness of allowing corporations to carry forward their unused R&D credits indefinitely, the State is unable to determine whether the R&D credits should be modified to prevent corporations from holding them for an unlimited period of time.

| Distribution of Research and Development Credits | Number of Claims | Percentage of total | Total Amount Claimed (in Millions) | Percentage of total | Average Amount Claimed (in Thousands) |

|---|---|---|---|---|---|

| By Gross Revenue | |||||

| $0 to 10 million | 2,098 | 69% | $62 | 5% | $30 |

| 10 to 50 million | 344 | 11 | 18 | 2 | 52 |

| 50 to 100 million | 88 | 3 | 14 | 1 | 162 |

| 100 to 500 million | 183 | 6 | 43 | 4 | 233 |

| 500 million to 1 billion | 96 | 3 | 35 | 3 | 369 |

| 1 billion or more | 227 | 8 | 949 | 85 | 4,179 |

| Totals | 3,036 | 100% | $1,121 | 100% | $369 |

| All Corporations | Corporations with Gross Revenue of $1 Billion or more | ||||

|---|---|---|---|---|---|

| Number of Claims | Percentage of total | Number of Claims | Percentage of total | ||

| By Industry | |||||

| Construction | 90 | 3% | 5 | 2% | |

| Finance and insurance, health care and social assistance | 75 | 3 | 4 | 2 | |

| Information | 136 | 4 | 17 | 7 | |

| Management of companies (holding companies) | 100 | 3 | 31 | 14 | |

| Manufacturing | 1,260 | 42 | 106 | 47 | |

| Professional, scientific, and technical services | 824 | 27 | 24 | 11 | |

| Retail trade | 50 | 2 | 3 | 1 | |

| Wholesale trade | 255 | 8 | 14 | 6 | |

| Other industries | 246 | 8 | 23 | 10 | |

| Totals | 3,036 | 100% | 227 | 100% | |

Source: California State Auditor’s analysis of unaudited Franchise Tax Board data for tax year 2012.

Moreover, the economic literature provides mixed evidence on the effectiveness of state‑level R&D credits, requiring further analysis. We reviewed 10 recent studies of how R&D credits work at the state level; six show some qualified evidence that the credits produce some positive change in state R&D activity, economic growth, and job creation, and four indicate that the credit has little to no influence on R&D spending. For example, an economic impact analysis of Texas’s R&D credit commissioned by the trade group Texans for Innovation indicates that the state’s 2006 repeal of its credit resulted in large job losses and a negative impact to the state’s economy. Alternatively, as mentioned previously, the state of Washington recently allowed its R&D credit to expire after a study found that the credit was not creating new jobs in a cost‑effective manner, as described in the text box.

Washington’s 2012 Study on Its Research and Development Credit

Washington established a business and occupation tax credit for qualified research and development expenditures (R&D credit) to encourage the formation of high‑wage, high‑skilled jobs and to stimulate the growth of high‑technology businesses within the state. In 2012 economic consultants analyzed the employment impact of the R&D credit for Washington’s Joint Legislative Audit Review Committee.

Using taxpayer data and statistical methods, economic consultants isolated the effect of the R&D credit on job creation, excluding such other factors as business decisions to expand output or employment for reasons other than R&D spending.

The study estimated that Washington’s R&D credit created 454 new jobs from 2005 to 2009 at a cost of between $17.4 to 24.3 million, or about $40,000 to $50,000 per new job. Washington’s Citizen Commission for Performance Measurement of Tax Preferences judged the R&D credit to be too costly given its benefits and recommended the legislature allow the credit to expire. The credit expired on January 1, 2015.

Source: California Department of Transportation headquarters division of maintenance organization chart.

Additional analysis would allow California’s Legislature to determine whether the R&D credit is fulfilling its purpose. Our review of several state‑level studies showed several options for evaluating the R&D credit, including requiring a state entity to study whether the credit is cost‑effective in stimulating additional R&D activity and new jobs and to evaluate its economic impact on the state economy. A detailed analysis could also determine whether the R&D credit is creating a windfall for some corporations, whether corporations should be able to carry forward the credit indefinitely, whether it should be modified to target smaller businesses, or whether it should be repealed. The analysis could also define the performance metrics needed to better gauge the R&D credit’s effectiveness. These performance metrics could include the benefit‑cost ratio of additional R&D spending resulting from the credit compared to the amount of forgone revenue for the State and the cost‑effectiveness of the number of jobs the R&D credit creates. By evaluating the R&D credit’s success and by defining performance metrics, the Legislature will be better able to ensure that the credit benefits the State.

Insufficient Evidence Exists to Support the Minimum Franchise Tax Exception’s Effectiveness in Encouraging New Businesses to Incorporate in California

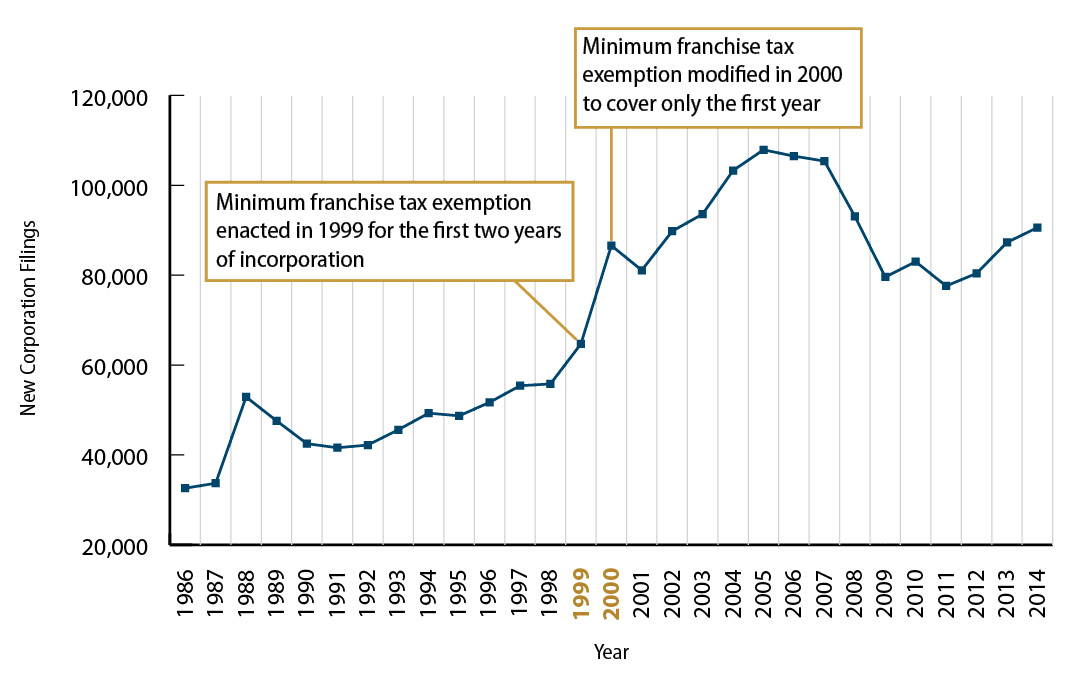

It is not clear whether the franchise exemption, which cost the State $45 million in forgone revenue in tax year 2012, had a noticeable effect on the formation of new corporations in California. Under California tax law, corporations are generally subject to a minimum franchise tax of a percentage of their income or $800, whichever is greater. The franchise exemption, which was enacted in 1999 and modified in 2000, eliminates this minimum franchise tax for corporations that incorporate or qualify to do business in the State on or after January 1, 2000, during their first taxable year. Citing the unfair burden of paying the minimum tax during a corporation’s first year, one of the authors of the bill enacting the franchise exemption suggested that the franchise exemption would help create or encourage corporate formation within California. As shown in Figure 2, although the number of new corporations formed in the State increased annually from around 90,000 in 2000 to around 110,000 in 2005, this trend may have occurred for a number of reasons other than the franchise exemption; these reasons include booms and contractions associated with the business cycle. Notably, the number of new corporations formed in 2014 returned to around 90,000. Without information showing why corporations formed in any given year, it is unclear whether the franchise exemption is fulfilling its purpose.

Figure 2

Filings in California for New Domestic and Foreign Stock Corporations

From 1986 Through 2014

Source: Unaudited data from the Secretary of State’s business programs division.

Because no state entity currently oversees or monitors the effectiveness of the franchise exemption, it is unclear if it is having any benefit on the California economy or whether it is encouraging additional businesses to incorporate within the State. We reviewed the statutes relevant to the franchise exemption as well as its enacting legislation and found no requirement for any state agency to monitor whether the exemption is having any effect on these new corporations.

In addition, we found insufficient evidence that the franchise exemption would have a noticeable effect on business formation or entrepreneurial activity. We did not locate any research relating specifically to the franchise exemption, but we reviewed studies that evaluate the effectiveness of small tax cuts, whose effects are similar to those of the franchise exemption. These studies provided conflicting evidence on the effectiveness of small tax cuts in improving state economic growth or business formation. For example, one study found that tax rates have a statistically significant effect on the rate of business formation. However, several other studies provided evidence that changes in state tax policies do not appear to have a significant effect on business formation and that a prohibitively large tax rate change would be required to generate a noticeable change in self‑employment activity. It is not clear that the current franchise exemption of $800 is large enough to have a noticeable effect on the rate of business incorporation within the State or whether the exemption’s forgone revenue would be better spent in another way.

Evaluation Options for the Minimum Franchise Tax Exemption

- “Hypothetical Firm” Method: Analysts develop theoretical income statements and tax returns for a hypothetical corporation and determine how state and local tax structures in different locations affect it.

- Statistical Approach: Analysts use real historical corporation data to model business formation behavior and to distinguish the effects of external factors like the minimum franchise tax exemption from other nontax factors such as general economic growth or a firm’s decision to expand for reasons not related to the exemption.

- Economic Modeling: Analysts use economic data and assumptions about the structural relationships and interactions between and among economic variables, including tax incentives, to anticipate their effect on corporations.

Source: California State Auditor’s analysis of the Legislative Analyst Office’s alternative options to study the impacts of the manufacturer’s investment credit and the research and development credits.

Further analysis of the franchise exemption would allow the Legislature to determine whether this exemption is achieving its purpose effectively and to consider whether it should be modified. A detailed study may be able to detect the effect of the franchise exemption or other small tax decreases on business formation, for example, by employing analytical methods that control for important nontax factors such as expansions or recessions associated with the business cycle. As the text box shows, some methods of evaluation include simulating the effect of the franchise exemption on a hypothetical firm’s performance or using statistical methods to estimate the impact of the exemption separately from other nontax factors on business formation. As part of the evaluation, some potential performance metrics could include the cost‑effectiveness of the number of companies or jobs the exemption has created. By evaluating the effectiveness of the franchise exemption according to desired performance metrics, the State could better determine whether the franchise exemption is achieving its purpose or whether it requires modification or repeal.

Three Tax Expenditures Appear to Be Fulfilling Their Purposes but Could Be Improved

Three of the tax expenditures we reviewed—the water’s edge election, the low‑income housing credit, and the film and television credit—appear to be achieving their respective purposes, but improvements would make them more effective. The water’s edge election has reduced international concern over California’s default method of corporate taxation, but it may provide corporations with unintended benefits that reduce state revenue, such as allowing corporations to shield income in offshore tax havens. In addition, the low‑income housing credit is subsidizing housing that would not otherwise be built, while modifications to the credit could increase the number of low‑income housing units built without increasing the total amount of the credits the State awards. Finally, although the film and television credit is keeping film and television productions from moving to other states, some of its benefits may be going to projects that would have filmed in the State without the credit.

Changes to the Water’s Edge Election Would Increase State Revenue While Continuing to Fulfill the Election’s Purpose

The water’s edge election could be improved by no longer allowing corporations to select between two tax structures and by taxing corporate profits kept in offshore tax havens. The water’s edge election allows multinational corporations to limit their taxable base to income derived from sources within the United States, so this income excludes earnings or losses from foreign portions of their business. According to the tax board, this election was enacted in response to controversy over California’s application of a worldwide unitary business tax concept to multinational corporations. However, the election’s current structure goes beyond this purpose and allows corporations to choose the most advantageous tax treatment of their income, thus lowering their tax bills and increasing forgone revenue to the State.

Enacted by the Legislature in 1955, worldwide unitary taxation requires corporations to pay a tax based on income derived from or attributable to sources within California that is earned by the corporations’ combined business units, which include all subsidiaries and parent companies regardless of their location. According to the tax board, through the 1960s and 1970s, the State was increasingly aggressive in applying worldwide unitary taxation to multinational businesses. Corporations brought to the United States Supreme Court (Supreme Court) their objections to this practice; however, the Supreme Court found the practice lawful. Nevertheless, in 1985 the British Parliament enacted legislation that would have penalized foreign shareholders of British companies if those shareholders did business in California or any other state that employed worldwide unitary taxation. California subsequently passed a law in 1986 implementing the water’s edge election. Although the statutory language does not state that the law was passed in response to international governments’ and multinational businesses’ objections, the law appears to address these concerns. In fiscal year 2012–13, the water’s edge election resulted in estimated forgone revenue of $700 million to the State.

Although the water’s edge election appears to be achieving its purpose of addressing other countries’ concerns, it may be doing so inefficiently because it provides corporations a choice of the method of reporting their income that most reduces their taxes. A 2010 article from the Harvard Journal on Legislation indicates that corporations that do not elect the water’s edge option may do so because having the State consider their entire worldwide income in assessing their taxes leads to lower tax bills. For example, a hypothetical multinational corporation in the first situation shown in Table 7 could choose to file under the water’s edge election to minimize its tax liability because the income attributable to California would be lower than under worldwide unitary taxation. Conversely, in the second hypothetical situation shown in the table, the corporation would instead likely choose to report its worldwide income for tax purposes because its foreign subsidiaries' reported losses that result in a lower tax liability under worldwide unitary taxation. The State could potentially increase tax revenue by compelling corporations who take advantage of preferential tax treatment under worldwide unitary taxation by requiring all corporations to file using the water’s edge tax treatment.

Mandating that all corporations use the water’s edge election, as other states have done, could increase California tax revenue while continuing to fulfill the tax expenditure’s purpose. According to a November 2015 tax article, at least three states—Alaska, Oregon, and Rhode Island—require corporations to file on a water's edge basis.4 If some corporations are choosing to file under the worldwide unitary taxation because it is advantageous to do so, requiring that all corporations file under the water's edge provision in California would continue to fulfill the purpose of the water’s edge election while also preventing corporations from using worldwide unitary taxation to lower their tax burdens.

Another way to improve the effectiveness of the water’s edge election would be to limit corporations’ ability to abuse this tax expenditure by the corporations’ shifting income to offshore tax havens. According to the U.S. Government Accountability Office (GAO) and the November 2015 tax article, tax havens are described as countries that, among other things, have no requirement that the taxpayer have substantial business activity in the jurisdiction and impose a low or zero rate of tax on all or certain categories of income, thus presenting significant tax evasion opportunities. Several other states have revised their water’s edge provisions to consider income sheltered in offshore tax havens as inside the water’s edge and thus subject to state tax apportionment. Oregon did so in 2013, estimating that this would provide $18 million in additional revenue for fiscal year 2014–15.5 Three other states and Washington, D.C., have also taken similar measures. Like Oregon, Montana includes a specific list of jurisdictions as tax havens, including the Cayman Islands and Luxembourg, and a state body may update the lists periodically. Alaska, West Virginia, and Washington, D.C., instead define tax havens as jurisdictions that meet certain criteria, such as imposing no or low income tax rates and facilitating tax avoidance. The tax board has estimated that including tax havens within the water’s edge for California would result in additional state revenue of $20 million in the first fiscal year that the provision is in effect and increase to $40 million the following fiscal year. Doing so would not violate the purpose of the water’s edge election in addressing international concern over double taxation because it would only extend the water’s edge to countries known as tax havens.

| Corporation Filings | Sales* | Income | tax treatment | Income Apportioned to California | Tax Owed (Tax rate of 10%)† |

|---|---|---|---|---|---|

| Worldwide total | $800 | $160 | Worldwide unitary taxation | $160 x (100/800)=$20.0 | $20 x 10%=$2.0 |

| Foreign | 300 | 90 | |||

| United States | 500 | 70 | Water’s edge election | $70 x (100/500)=$14.0 | $14 x 10%=$1.4 |

| California | 100 | (Apportioned by sales and chosen tax treatment)* |

| Corporation Filings | Sales* | Income | tax treatment | Income Apportioned to California | Tax Owed (Tax rate of 10%)† |

|---|---|---|---|---|---|

| Worldwide total | $800 | $40 | Worldwide unitary taxation | $40 x (100/800)=$5.0 | $5 x 10%=$0.5 |

| Foreign | 300 | (30) | |||

| United States | 500 | 70 | Water’s edge election | $70 x (100/500)=$14.0 | $14 x 10%=$1.4 |

| California | 100 | (Apportioned by sales and chosen tax treatment)* |

Source: California State Auditor’s analysis using information provided by the chief economist of the Franchise Tax Board’s (tax board) Economic and Research Statistics Bureau and by California corporate tax law.

Light red = Not tax advantageousLight green = Tax advantageous

* According to the tax board’s chief economist, Proposition 39 (2012) caused the majority of corporations to apportion their income to California based only on their sales. Although some corporations can still apportion their income based on property, payroll, and sales factors, the hypothetical examples above only apply the sales factor for illustrative purposes.

† State law applies a different tax rate depending on the type of corporation. This hypothetical example uses a simplified tax rate for illustrative purposes only.

Changing Who Can Purchase Low‑Income Housing Credits May Increase Funding for Construction, Thus Providing Additional Housing Units

The low‑income housing credit, which helps fund rental housing projects for low‑income Californians, could be made more efficient with modifications to reduce its negative tax implications. This credit, in combination with its federal counterpart, is designed to cover only the expenses necessary to make a low‑income housing project economically viable. As shown in Figure 3, developers of low‑income housing—those who own the rehabilitated or newly constructed projects—apply for credits to cover gaps in funding, and credits are not awarded until after the housing is built. According to the California Tax Credit Allocation Committee (committee), which authorizes the credits, most credits are sold to corporate or individual investors in exchange for financing the capital costs of project construction. Award periods vary depending on the type of credit: four years for the state credit and 10 years for the federal credit. Since its inception in 1987, the state credit has funded the development of nearly 60,000 housing units at a cost of $1.8 billion, or around $30,000 per unit.

Federal Tax Implications for Investors Claiming the State’s Low‑Income Housing Tax Credits

Developers typically partner with investors to obtain credits. Investors provide up‑front funds for construction, and developers provide credits for investors to later use to lower their state taxes. Both the developer and investor own a stake in the housing project.

According to legislative analysis of Senate Bill 377 of 2015 (SB 377), the Internal Revenue Service has opined that state tax credits obtained by investors with an ownership interest in a low‑income housing project reduce the investors’ state tax liability, which can then increase federal taxes. Investors use the state tax liability to reduce their federal taxes, so lower state tax liability results in less reduction in federal taxes. Investors factor this calculation into the amount they are willing to pay developers for state tax credits.

Sources: California Tax Credit Allocation Committee’s description of the low‑income housing tax credit and an August 14, 2015, analysis of Senate Bill 377 of 2015 by the Assembly Committee on Revenue and Taxation.

The committee generally awards both the federal and state low‑income housing credits on a competitive basis to developers who meet the credits’ requirements. The state credit is generally only available to projects that receive, or qualify to receive, federal credits, and state law requires that state and federal credits combined do not exceed what is necessary for a project’s financial feasibility. We reviewed the process by which the committee allocates and oversees the state and federal credits and found it reasonable. The committee allocates credits to the most worthy projects according to a detailed scoring system and then monitors the projects after the housing units are built, ensuring that developers meet and continue to adhere to the state and federal credit requirements.

When developers partner with investors on low‑income housing projects, the investors do not typically pay the developers the full value of the state credits they expect to claim because of the negative federal tax implications. For example, investors paid developers, on average, only 70 cents for each dollar of the state credits awarded in 2014. As the text box describes, investors limit the amounts they are willing to pay for credits because claiming them increases their federal tax liabilities. Credits obtained through a partnership reduce investors’ state tax liabilities, which can cause corresponding increases in their federal taxes. Thus, investors pay developers only around 70 percent of each credit’s actual value, meaning that every state credit dollar does not provide a full dollar for construction.

Figure 3

How a Low‑Income Housing Project Is Funded

Source: California State Auditor’s analysis of the California Code of Regulations.

Reducing federal tax implications may be one way to increase the amount investors pay developers for state credits. Prior legislation has attempted to address the discrepancy between state and federal credits by allowing developers to sell state credits to investors instead of partnering with them. As discussed previously in the text box, according to the Assembly Committee on Revenue and Taxation’s analysis of Senate Bill 377 (2015), the bill’s author stated that it would eliminate the negative federal tax implications investors face under the current state credit. The committee analysis also indicated that proponents of Senate Bill 377 (2015) believed that the bill would result in investors’ willingness to pay more for the state credit, bringing the state credit closer to the dollar‑for‑dollar parity enjoyed by its federal counterpart. Improving the value of each state credit could ultimately lead to funding additional units of low‑income housing without additional forgone revenue to the State.

Further Study of the Film and Television Credit Could Limit Instances in Which It Benefits Projects That Would Have Filmed in the State Without the Credit

Although the film and television credit appears to be keeping some film and television production from moving to other states, some of its benefits may be going to projects that would have filmed in the State even in the absence of the credit. The credit was first enacted in 2009 and was given to production companies on a first‑come, first‑served basis. A newer version of the credit, first available on January 1, 2016, requires the commission to allocate the credit on a competitive basis, and to collect data on production companies that apply for, but do not receive, the new credit.

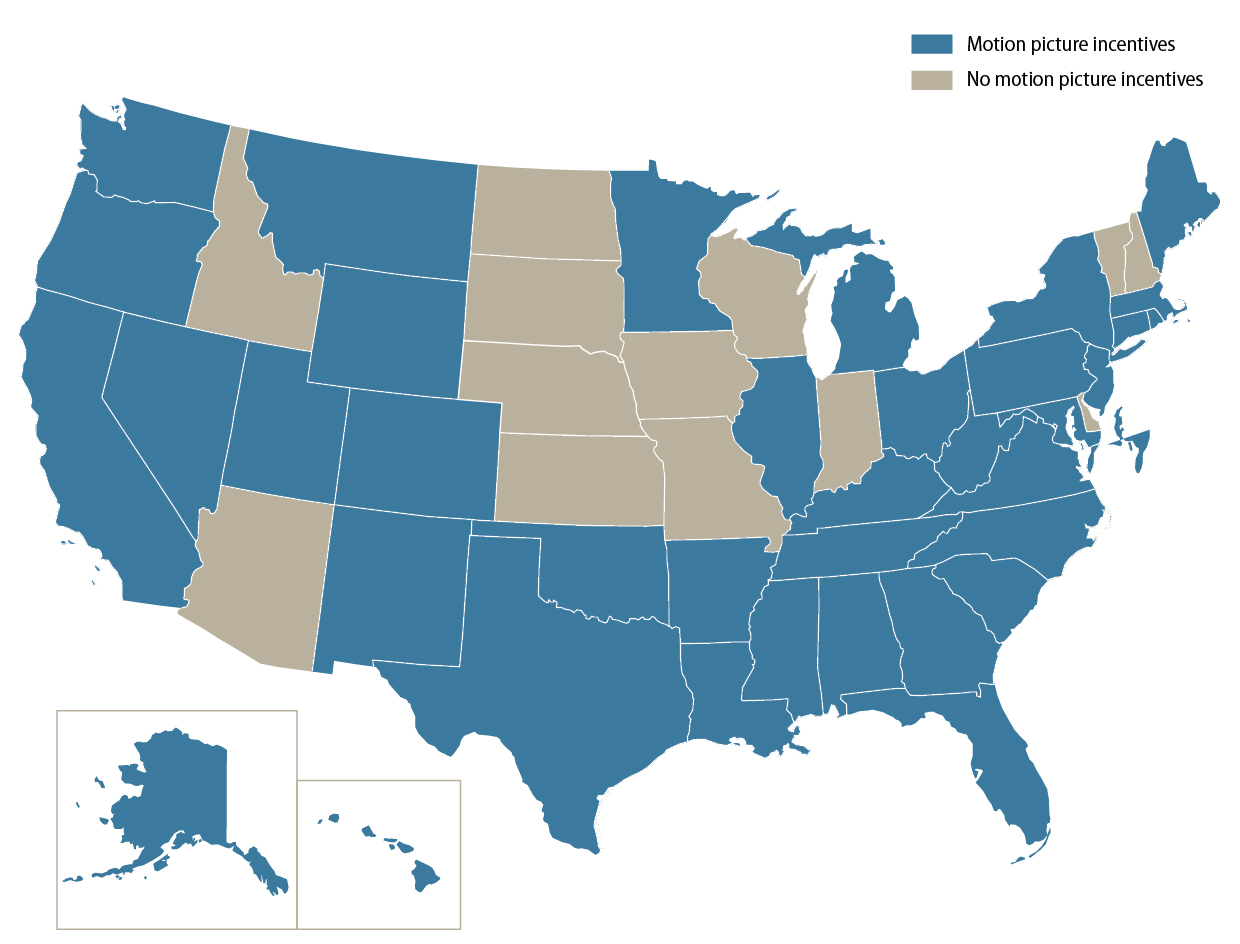

The film and television credit—a version of which many other states also offer—constituted $100 million in foregone revenues in fiscal year 2012–13 and is intended to encourage film and television production in California. As shown in Figure 4, the LAO found that credits incentivizing motion picture production existed in 37 states including California as of 2014. In its 2014 report on the film and television credit, the LAO stated that California is the historical home of the motion picture industry and provided more than half of the motion picture jobs in the nation in 2012. However, according to the report, California’s share of the motion picture industry’s national employment has steadily declined since 2004—when California accounted for 65 percent of the national film and television production jobs. This decline indicates that other states’ incentives may have captured jobs and production activity that otherwise might have occurred in California.

The film and television credit appears to have a positive effect on the state economy. The LAO indicates that the number of film and television production jobs in California declined from 124,000 in 2004 to 107,000 in 2014—a decrease of around 13 percent—as other states adopted film and television production subsidies. However, the commission, which allocates the credit, estimated that since the credit’s inception in 2009 through fiscal year 2015–16, it has allocated $757 million in credits to 326 applicants, and the commission also estimates that these credits will generate or have generated spending of $5.9 billion in the State. Further, the commission noted that the film and television credit has resulted in the aggregate hiring of 608,000 total crew members, cast members, and background actors. The film and television credit is therefore helping the State retain jobs that it might otherwise lose to other states.

Figure 4

States With Motion Picture Incentives as of March 2014

Source: The 2014 report from the California Legislative Analyst’s Office titled Film and Television Production: Overview of Motion Picture Industry and State Tax Credits.

However, a commission survey of film and television credit applicants who did not receive the old version of the credit indicates that the credit may be subsidizing some production activity that would have occurred in the State without the credit. State law requires, the commission, when possible, to obtain information from applicants who did not receive a credit. For fiscal years 2010–11 through 2014–15, the commission’s survey found that nearly a third of applicants denied credit nonetheless filmed in the State. These denied applicants spent approximately $600 million for film production that remained in the State, while the other two thirds of applicants denied the credit moved their projects elsewhere and spent $3.6 billion in production expenses outside of the State. However, this survey data only pertains to the old version of the credit as no survey data for the new credit was available during our audit. Because the new credits are issued on a competitive basis, the allocation structure may reduce the number of productions that receive credits but would have filmed in the state even without them. Nonetheless, the State may be providing benefits to projects that do not need them, and it may be limiting the credit’s ability to create additional economic activity.

Further analysis would allow the Legislature to determine the extent to which the film and television credit benefits projects that would have filmed in the State without the credit. No detailed data besides the commission’s survey exist to show the extent to which this situation is occurring. The commission’s survey of productions that filmed in the State after not receiving a credit does not specifically address how many productions that received a credit would have filmed in the State without the credit, nor are there any other surveys or studies that consider this aspect of the credit. The LAO is conducting an in‑depth analysis of the credit and expects to issue a report in the spring or summer of 2016. The results of this report may indicate that action is needed to modify the credit to prevent these windfalls.

The Subchapter S Corporation Election Appears to Be Functioning as Intended

Our review of the Subchapter S corporation (S corporation) election found that it appears to be achieving its purpose and does not need legislative changes to improve its effectiveness. Costing $220 million in forgone revenue in fiscal year 2012–13, the S corporation election offers businesses an alternative to the standard Subchapter C corporation (C corporation) filing status. Like C corporations, S corporations are legal entities that are generally separate and distinct from their owners, and with separate and distinct liabilities. Additionally, they are limited to 100 shareholders, and those shareholders must be United States residents. California S corporations are taxed at a lower entity rate than C corporations and S corporations pass income through to their shareholders, who may be subject to personal income taxes on those distributions. Legislative correspondence from the chair of the Senate Revenue and Taxation Committee at the time that state law recognized S corporations suggests that the State’s S corporation election is intended to conform state tax law with federal tax law and to help California businesses remain competitive with those located elsewhere. California recognizes the federal S corporation election but imposes a 1.5 percent tax on S corporations’ net income, and this tax mitigates some of the revenue loss from the S corporation election while preserving the incentive for small businesses to file in this manner.

Our review of academic and governmental literature found that small businesses primarily use S corporation filing, and this literature does not describe any potential ways to improve the S corporation election’s effectiveness. According to a report by the GAO, as of 2006, 94 percent of S corporations in the nation had three or fewer shareholders, indicating that most businesses electing to operate as S corporations are small. The GAO report and a study by the Journal of American Taxation Association found that small businesses frequently cite limited liability protection as an important reason to make this election. Our review of some State legislative proposals to modify the S corporation election did not identify any proposals that would substantially improve its performance or effectiveness.

Although Capping Tax Expenditures Offers Benefits, Doing So May Not Always Be Appropriate

Limits on tax expenditures allow the State to control the amount of revenue it forgoes; however, such limits—sometimes referred to as caps—are not applicable for each type of corporate tax expenditure. In fact, we found that three of the four corporate tax expenditures we reviewed that do not already have caps appear to be inappropriate candidates for such control mechanisms. As shown in Table 8, we evaluated the viability of placing caps on the amount of revenue the State forgoes for each of the six corporate tax expenditures we reviewed.6 State law has capped the film and television credit, which ranges from $100 million per fiscal year to $330 million for fiscal year 2019–20. State law also caps the low‑income housing credit; for 2015, the cap was approximately $94 million. 7 However, two of the other tax expenditures we reviewed—the water’s edge and the S corporation elections—are tax‑filing structures intended to be available for all qualifying corporate taxpayers; thus a cap on these expenditures appears inappropriate. Similarly, the franchise exemption is intended for all newly incorporated businesses; capping this expenditure would be appropriate if the purpose of this corporate tax expenditure was fundamentally changed to focus on certain sectors of new businesses, such as small businesses. We believe that—absent this type of fundamental change—a cap on this corporate tax expenditure would not be appropriate.

| Corporate Tax Expenditure | Is This Corporate Tax Expenditure Capped? | Cap Amount | Do viable options exist to cap the tax expenditure? |

|---|---|---|---|

| Research and development (R&D) credit | No | – | Yes—a cap could limit this credit to an annual amount or to a fixed amount per credit redeemed. |

| Water’s edge election | No | – | No—these tax expenditures cannot be capped because they affect the tax filing structures available to all corporations. |

| Subchapter S corporation election | No | – | |

| Film and television credit | Yes | $330 million annually | Yes—state law already caps these tax expenditures to annual amounts. |

| Low‑income housing credit | Yes | $94 million annually* | |

| Minimum franchise tax exemption | No | – | No—this tax expenditure cannot be capped because the exemption is designed to be available to all new corporations. |

Source: California State Auditor’s analysis of the Revenue and Taxation Code as well as the California Tax Credit Allocation Committee’s (committee) description of the low‑income housing tax credit.

* According to the committee, the cap for 2015 was approximately $94 million, which reflects the $70 million cap in state law adjusted for inflation since 2001 and includes any unused or returned credits from previous years.

The caps on the film and television credit and the low‑income housing credit are examples of how caps can limit benefits to corporations that most closely meet the credits’ criteria. For example, applicants for the low‑income housing credit must submit a detailed application to a state committee, identifying how much each housing unit will cost to construct, the project’s proximity to transit, and whether daycare is available, among other factors. The committee uses these criteria to rank applications, and it awards credits to the highest‑ranked projects. Because demand for the credit exceeds available credit funds, the State can limit the credit’s benefits to those projects that best achieve its purpose. Additionally, projects that are awarded low‑income housing credits are subject to routine monitoring by the committee to ensure that they continue to meet the terms agreed to in the credit application over a multiyear compliance period. Similarly, corporations that request film and television credits may not claim them until they submit additional information to the commission, including documentation of qualified expenditures to prove that filming activity occurred in the State. Once these entities have awarded the available credits for that year to qualifying corporations, no more can be awarded.

A similar cap could ostensibly be placed on the R&D credit. However, as discussed earlier in the report, it is not clear whether the R&D credit in its current form is fulfilling its purpose of stimulating additional R&D spending within the State. Capping the R&D credit without first having a clear understanding of whether and exactly how it creates economic benefit for the State would not be advisable. Once the R&D credit’s effectiveness has been evaluated, the Legislature could cap it, as some other states have done, by limiting either the total annual amount of the credits issued by the State, the amount per credit claimed by each corporation, or both. For example, New Hampshire’s state law limits the amount of its R&D credits issued to all taxpayers to $2 million annually, and limits each taxpayer's proportional share of the R&D credit to $50,000 each year. If, for example, the Legislature had also limited R&D credits to $50,000 per corporation annually during tax year 2012, and if taxpayer behavior had not changed under this cap, we estimate that the State’s forgone revenue from the R&D credit would have decreased from about $1.1 billion in tax year 2012 to about $58 million.

Alternatively, if the Legislature were to place a total annual cap on the R&D credit and required that corporations apply for this credit on a competitive basis, it would have to create an oversight entity, similar to the state committee that oversees the low‑income housing credit. However, we believe the Legislature should consider these options after a study has been conducted on the effectiveness of the R&D credit. Such a study would help clarify how to maintain much of the value created by the credit while mitigating the State’s currently unlimited exposure to decreased revenue occurring because of this credit.

Recommendations

To increase oversight of existing and future tax expenditures, the Legislature should consider following these best practices for that oversight:

- Enact a joint legislative rule requiring specific goals, purposes, and objectives as well as detailed performance indicators for all tax expenditure types, including elections and exemptions.

- Enact a joint legislative rule to require sunset dates for all future tax expenditures.

- Enact a law requiring a state entity to conduct a comprehensive evaluation of all tax expenditures and develop conclusions and recommendations to continue, modify, or repeal each of them. The state entity should have the necessary resources and a reasonable time frame for analysis.

- Enact a joint legislative rule requiring a legislative body to consider the state entity’s conclusions to aid it in developing recommendations to continue, modify, or repeal every tax expenditure.

To ensure that the R&D credit and franchise exemption are effectively fulfilling their purposes, the Legislature should consider doing the following:

- Commission a study on the cost‑effectiveness of the R&D credit for stimulating additional R&D activity or new jobs within the State, including an impact analysis on how the credit affects the state economy. The study should also define performance metrics for use in subsequent reports.

- Commission an evaluation of the franchise exemption to determine if it is effectively encouraging business formation within the State.

To improve the effectiveness of the water’s edge election and the low‑income housing credit, the Legislature should consider doing the following:

- Modify the water’s edge election to include tax havens within the water’s edge and thus subject to state tax apportionment.

- Make the water’s edge election mandatory and require all multinational corporations to exclude foreign income, except tax havens, from state tax apportionment.

- Allow low‑income housing developers to sell project credits to investors in a manner that reduces the federal tax implications for investors who claim the credit.

- If not otherwise addressed by the LAO's planned report on the film and television credit, the Legislature should commission a study to determine how to limit instances in which the credit benefits projects that would have filmed in the state without it.

We conducted this audit under the authority vested in the California State Auditor by Section 8543 et seq. of the California Government Code and according to generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives specified in the Scope and Methodology section of the report. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Respectfully submitted,

ELAINE M. HOWLE, CPA

State Auditor

Date:

April 12, 2016

Staff:

John Baier, CPA, Audit Principal

Aaron Fellner, MPP

Jerry A. Lewis, CICA

Oswin Chan, MPP, CIA

Taylor William Kayatta, JD, MBA

Legal Counsel:

Scott A. Baxter, Senior Staff Counsel

For questions regarding the contents of this report, please contact

Margarita Fernández, Chief of Public Affairs, at 916.445.0255.

Footnotes

3The Legislature did not pass several of these bills. Had it done so, legislators might have added language meeting this new requirement before they sent the bills to the governor.Go back to text

4Alaska requires oil and gas companies to file on a worldwide combined basis instead of a water's edge.Go back to text

5According to Oregon’s Legislative Revenue Office, it will not be able to calculate the total amount of additional revenue until all corporations have submitted their 2015 tax reports. It does not anticipate having this number until 2017.Go back to text

6Caps on the corporate tax expenditures we reviewed include all credits claimed against the personal and corporate income tax and the gross premiums tax.Go back to text

7The annual cap on the low‑income housing credit is determined based upon a formula set forth in state law.Go back to text