Introduction

Background

The Orange County Great Park (Great Park) is a park under development on the grounds of the former Marine Corps Air Station El Toro (air station). In 1993 the United States Department of Defense recommended closing the air station, and it officially closed in July 1999. In 1994 Orange County voters approved a measure to change Orange County’s General Plan for air station property to use it as an airport. However, in March 2002, following a multiyear legal and political battle, Orange County voters approved the Orange County Central Park and Nature Preserve Initiative, overturning the previous measure and amending Orange County’s General Plan to create a park instead of an airport at the site of the former air station. The city of Irvine annexed the former air station in January 2004, giving itself control of zoning and other powers over much of the property. According to the 2009‑2020 Strategic Business Plan (business plan) of the Orange County Great Park Corporation (park corporation), in September 2004 the Navy issued an invitation for bids for the 3,700‑acre site. An auction was held for four parcels and closed in February 2005. A developer purchased all four parcels. Irvine entered into an agreement with the developer that granted the developer rights to build on a portion of the land in exchange for transferring more than 1,300 acres to public use and contributing $200 million to the development of Great Park. According to the business plan of the park corporation, the agreement also included $201 million through a bond sale, secured by taxes levied on the development’s properties, to provide funding for public infrastructure and facilities. Thus, Irvine was to receive $401 million for the development and maintenance of Great Park.

Irvine established the park corporation in July 2003 to develop and operate Great Park. Until 2013 the park corporation’s board consisted of nine directors, including all five members of Irvine’s city council. In January 2013, the city council eliminated the four members who were not part of the city council and consolidated Great Park employees under the authority of the Irvine city manager. Finally, in November 2014, Irvine voters approved a measure that reaffirmed and expanded upon a previous city council resolution giving Irvine the final authority over all financial matters concerning Great Park.

Development of Great Park

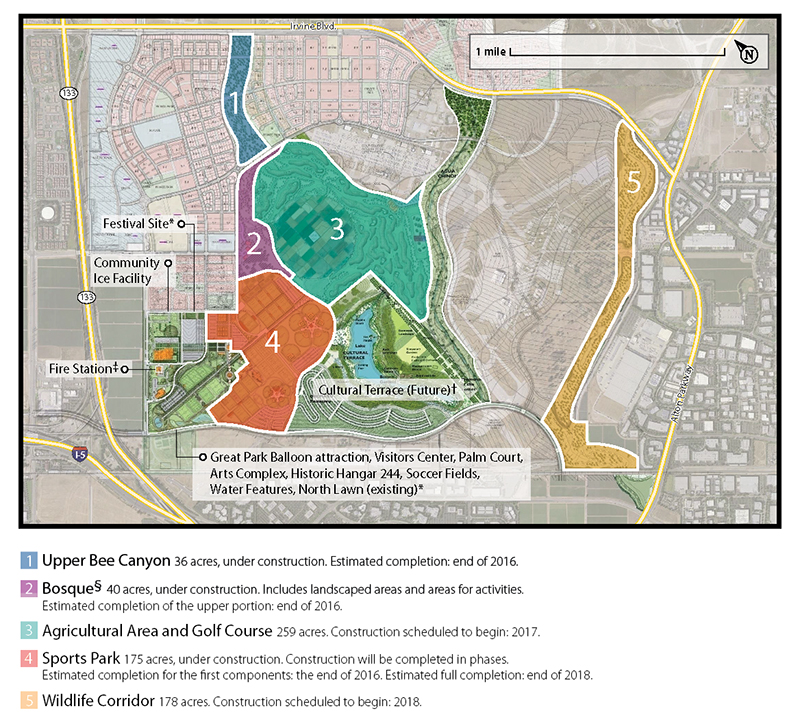

According to a 2015 report of the Orange County Grand Jury, when in 2007 home construction started grinding to a halt, the developer told Irvine that its agreement to provide $201 million to Irvine toward Great Park infrastructure was not possible. According to the business plan, in 2009 the developer agreed to provide about $60 million in revenue over five years and additional revenue for park maintenance as needed beginning in fiscal year 2014–15. According to city staff, as of the beginning of 2013, an area encompassing 88 acres of attractions had been developed. Figure 1 shows a map of Great Park, including current and planned developments.

In November 2013, Irvine approved a new development plan for a portion of Great Park. According to a staff report filed with the agenda for the November 2013 meeting, Irvine approved a proposal to develop 688 acres of Great Park for $172 million in improvements. This new plan included a wooded area, a golf course, and a sports park. According to city staff, the master plan was updated in 2014 to reflect the plans for the development of the 688 acres, but for those portions of Great Park outside of the 688 acres, the master plan did not change.

Irvine’s Previously Commissioned Reviews of Great Park

In December 2011, Irvine engaged another accounting firm to conduct a compliance review of Great Park’s schematic design contract. This review, published in June 2012, did not yield any significant or material findings. However, the firm’s review did detect some discrepancies between the insurance information that contractors provided and the contract’s requirements for insurance. It also detected about $4,000 in overpayments to the Great Park Design Studio. According to the review, the city received reimbursement for the overpayments.

Figure 1

Current and Planned Development of Orange County Great Park

Sources: The city of Irvine’s website and statements from Irvine staff.

* According to city staff, the festival site and the area encompassing the balloon, visitors center, and other facilities cover 88 acres already developed as of the beginning of 2013.

† According to city staff, the cultural terrace is part of the original master plan for Great Park. There is no timeline for development of the terrace.

‡ Construction of the fire station is to begin in fiscal year 2016–17.

§ Bosque is a Spanish word meaning forest.

The Great Park Review and Its Subcommittee

In January 2013, the city council unanimously approved a motion directing city staff to solicit proposals for a comprehensive compliance/forensic audit performance review of Great Park contracts. The city council also appointed a two‑member subcommittee to receive periodic updates on the findings from the consultant performing the park review and to bring such information to the full city council.

The city council approved the draft request for proposal (RFP) for a contract performance review of Great Park (park review) in a March 2013 meeting, and Irvine contracted with the forensics firm of Hagen, Streiff, Newton & Oshiro, Accountants, PC (HSNO) in June 2013 to conduct the park review. In January 2014, HSNO presented a report of its findings and recommendations in a city council meeting. This report included findings that contracts contained excessive uses of change orders and inaccurately defined project scopes and that Irvine improperly used sole‑source contracts. The report also contained tables of revenues and expenses and reported that Irvine had spent more than $210 million on Great Park as of the end of 2012. HSNO recommended that the city council compel the testimony of certain individuals whom HSNO deemed uncooperative. Further, HSNO made numerous recommendations that Irvine conduct additional reviews of Great Park.

Two weeks following the release of HSNO’s report, the city council authorized the city manager to execute an agreement with HSNO to perform the second phase of the park review. The city council also adopted a resolution giving the subcommittee subpoena power to compel the testimony of certain Great Park contractors and city staff and requiring the city manager and staff to cooperate fully with the investigation. In June 2014, one subcommittee member announced that the law firm of Aleshire & Wynder, LLC (Aleshire) would replace the law firm of Jones & Mayer as the city’s special counsel for the park review. Aleshire conducted most of the depositions for the park review, which Irvine subsequently published on its website.

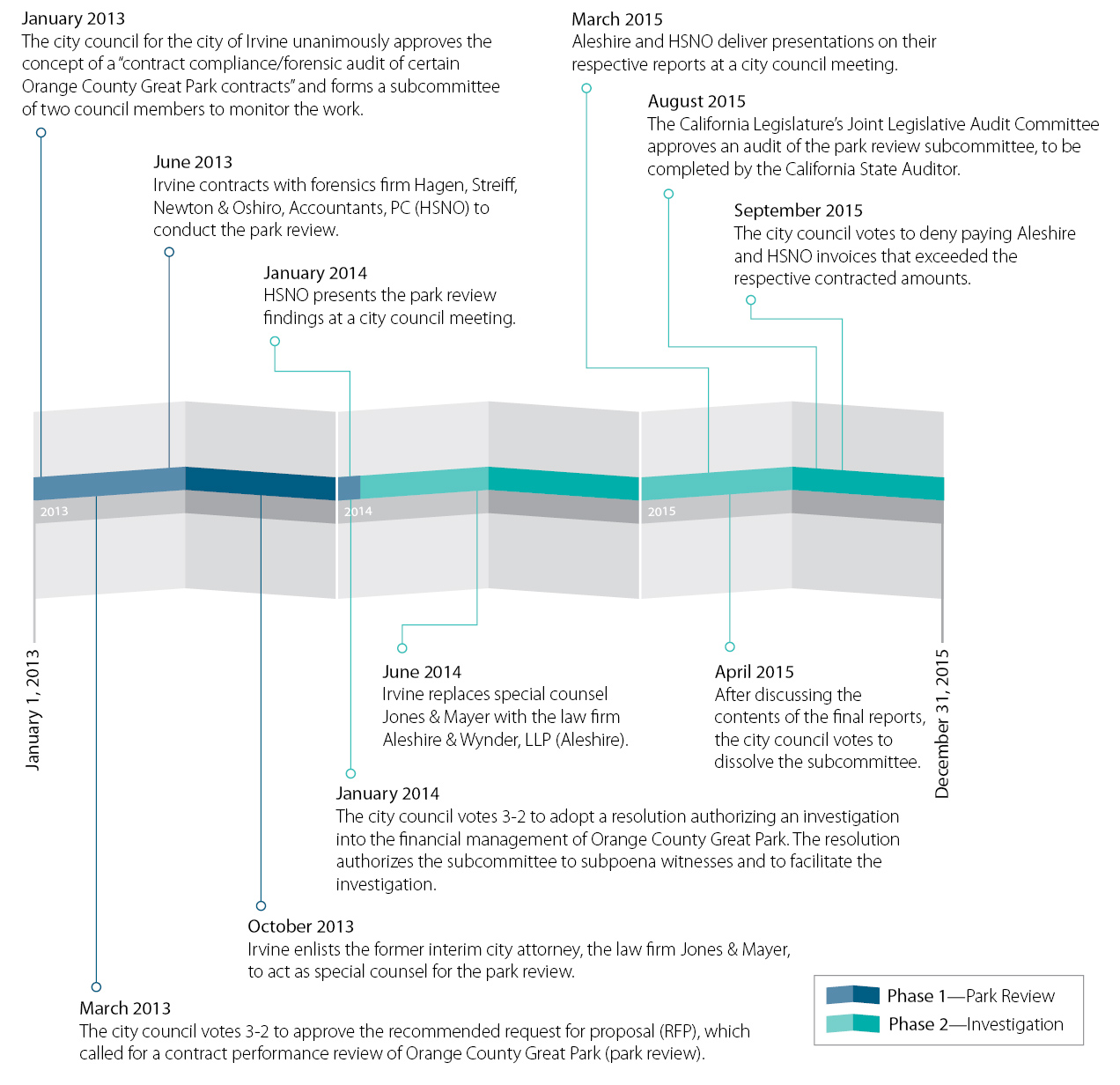

Aleshire and HSNO each delivered final reports to the city council in March 2015. Aleshire’s report included a discussion about the actions of a city council member—defeated in a bid for reelection in November 2014—stating that this member largely directed the management of the Great Park project and that he chose to describe the project as being far less costly than the estimated cost he had been quoted by the Great Park Design Studio. Aleshire’s report also stated that Great Park contractors had undisclosed conflicts of interest. HSNO’s report stated that it superseded HSNO’s January 2014 report and included findings related to the lack of a budget constraint for design and construction of Great Park, to the influence of the city council member defeated in November 2014, and to work a public relations consultant performed that was not consistent with the purpose of the funds used to pay that consultant. Figure 2 shows the timeline of key contracts and events related to the park review.

Figure 2

Summary of Key Contracts and Events Related to the Orange County Great Park Review

January 2013 Through December 2015

Sources: The city of Irvine’s city council meetings, minutes, and resolutions; contracts related to the park review; city correspondence; and the California Joint Legislative Audit Committee minutes.

Table 1 shows Irvine’s decisions and appropriations, by consultant, related to the park review, between February 2013 and October 2015. Further, Table 1 indicates that as of December 2015, the city had spent roughly $1.7 million on the park review and related activities. According to Irvine’s records, the city paid for the park review and related activities from the Great Park Fund and from its general fund and did not use state funds. According to the city’s financial statements, between fiscal years 2012–13 and 2014–15, revenue for the Great Park fund came primarily from developers and charges for services. Revenue for Irvine’s general fund came largely from taxes, such as local property taxes.

| Decisions and Appropriations related to the performance Review of the Orange County Great Park Contracts (park review) | |||

|---|---|---|---|

| Month and Year | Hagan, Streiff, Newton & Oshiro, Accountants, PC (HSNO) | Aleshire & Wynder, LLP (Aleshire) | Other Consultants |

| February 2013 | Irvine spends $1,650 for consulting services to create the request for proposal (RFP), approved by the city council in March 2013. | ||

| June 2013 | Irvine contracts with HSNO to complete the park review. HSNO receives $240,000 of the money appropriated for the park review in January 2013. | ||

| October 2013 | Irvine enlists the services of its former interim city attorney Jones & Mayer to provide special counsel legal services for the park review. | ||

| January 2014 | Irvine city council authorizes the appropriation of $400,000 for phase 2 of the park review. HSNO receives the entirety of this appropriation. | ||

| February 2014 | The city requests the services of a private judge to aid in phase 2 of the park review.* | ||

| June 2014 | At the request of the subcommittee, the city manager retains Aleshire’s services to replace Jones & Mayer as special counsel to the park review. Irvine contracts with Aleshire for $30,000 in services. | ||

| July 2014 | Irvine city council authorizes the appropriation of $333,000 to finalize the park review. In consultation with Aleshire, city staff designate $255,000 of this appropriation to Aleshire and $78,000 to HSNO. | ||

| December 2014 | Irvine city council authorizes an additional $60,000 for HSNO to complete the park review. | Irvine city council authorizes $180,000 for Aleshire to complete the park review. | |

| April 2015 | The city manager engages Aleshire under a separate $10,000 contract to represent Irvine at hearings related to a state audit of the park review proposed to the Joint Legislative Audit Committee. | ||

| May 2015 | Irvine city council approves an amendment to Aleshire’s June 2014 contract to include preparing legal documentation related to the park review. The city council authorizes up to $80,000 for Aleshire to complete these services. | Under the city manager’s authority, Irvine engages a separate law firm for a maximum amount of $90,000 to, among other services, evaluate legal options related to results of the park review. | |

| June 2015 | Under the city manager’s authority, Irvine increases Aleshire’s April 2015 contract amount by $15,000 for services related to a requested state audit of the park review. Irvine further amends Aleshire’s April 2015 contract to include assisting with public records act requests and litigation efforts. Irvine appropriates $60,000 for these new services. | Under the city manager’s authority, Irvine engages special legal counsel for a maximum amount of $50,000 to evaluate options for addressing legal malpractice identified in the park review. | |

| July 2015 | Under the city manager’s authority, Irvine contracts with special legal counsel for a maximum amount of $25,000 to analyze various litigation options and corresponding potential consequences of those options. | ||

| September 2015 | Under the city manager’s authority, Irvine contracts for legal advice on payment of invoices for the park review. The contract amount is not to exceed $5,000. | ||

| October 2015 | Pursuant to the city council’s direction at its September 2015 meeting, Irvine amends Aleshire’s June 2014 contract to compensate the firm for an additional $56,174 in services. | ||

| Total Actual Expenditures for the Park Review as of December 2015, by Consultant | |||

| $778,000 | $671,700 | $229,600 | |

| Total Actual Expenditures for the Park Review as of December 2015 | |||

| $1,679,300 | |||

Note: Actual expenditures do not necessarily equal the total amounts appropriated or contracted. In some cases, consultants did not spend their entire authorized amounts.

* At the request of city staff, Jones & Mayer and later Aleshire subcontract with the private judge for services provided during the park review. According to invoices from Jones & Mayer and Aleshire, the firms paid about $18,400 for these services.

Public Scrutiny of the Park Review

The park review came under public scrutiny throughout the review’s duration and after the publication of the reports. Notably, a Great Park contractor created a website and video that criticized the findings HSNO made in its January 2014 report. In April 2015, another Great Park contractor published a 28‑page rebuttal to HSNO’s and Aleshire’s final March 2015 reports. Members of the public also attended multiple city council meetings to speak in support of or against the park review.

Scope and Methodology

The Joint Legislative Audit Committee (Audit Committee) directed the California State Auditor to perform an audit of the performance of Irvine city council’s subcommittee regarding the laws, regulations, and policies it followed and the actions it took during the consultant‑led investigation and review of Great Park. Table 2 lists the objectives that the Audit Committee approved and the methods used to address those objectives.

| Audit Objective | Method | |

|---|---|---|

| 1 | Review and evaluate the laws, rules, and regulations significant to the audit objectives. | Reviewed relevant state laws and regulations. |

| 2 | Determine whether the forensics firm Hagan, Streiff, Newton & Oshiro Accountants, PC (HSNO) and the law firm of Aleshire & Wynder, LLP (Aleshire), conducted their reviews in accordance with applicable audit standards and industry best practices when developing the January 2014 report and subsequent reports. In addition, determine whether any transfer of audit responsibilities related to the review complied with these guidelines and standards. |

|

|

||

|

||

|

||

|

||

| 3 | Determine whether the process for selecting the accountants, attorneys, and private judge involved with the investigation and audit complied with applicable laws, regulations, and policies. |

|

|

||

|

||

|

||

| 4 | Determine how the audit subcommittee publicly characterized the nature of the forensics firm’s and the law firm’s work. | Assessed the terminology used to describe the park review in Irvine’s contracts with the consultants, at city council meetings, in communications with constituents, and in the media. |

| 5 | Determine whether the city council and the audit subcommittee conducted the review in a transparent and open manner. For example, determine whether open meeting laws were followed. |

|

|

||

|

||

| 6 | Determine whether the audit subcommittee’s and city council’s use of government subpoena power complied with applicable laws, regulations, and policies. |

|

|

||

|

||

| 7 | Determine whether state funds were used for this review, and, if so, whether these funds were used appropriately. |

|

|

||

|

||

| 8 | To the extent possible, determine whether discussions took place between the audit subcommittee, attorneys, and auditors to time the public release of their reports and depositions to occur just prior to upcoming city or state elections. |

|

|

||

|

||

| 9 | Determine whether individuals or companies who raised concerns about the accuracy of the January 2014 report or subsequent reports were afforded whistleblower protections, if applicable. |

|

|

||

|

||

|

||

| 10 | Review and assess any other issues that are significant to the audit. |

|

|

||

|

||