Use one of the links below to go directly to that chapter:

Chapter 1

The University of California Undermined Its Commitment to California Resident Students in Exchange for Revenue Generated by Nonresidents

Chapter Summary

The University of California’s (university) desire to increase its nonresident supplemental tuition revenue (nonresident revenue) appears to have significantly influenced its admission decisions, at times at the expense of residents. In fact, while the university admitted 2,600 more residents in academic year 2014–15 than it did in academic year 2010–11, a 4 percent increase, at the same time it increased the number of nonresidents it admitted by 182 percent, or 17,200 students.1 This significant increase in nonresidents coincided with the university’s decision in 2011 to lower its admission standard for nonresidents. As a likely result, over the past three years, the university admitted nearly 16,000 nonresidents who were less qualified on every academic score we evaluated than the median scores for admitted residents. Further, the university made it less appealing for the residents it did admit to attend the university by denying an increasingly large percentage of them admission to a campus of their choice. In contrast, nonresidents, if admitted, are never denied admission to a campus of their choice. The university’s admission decisions have also hampered its efforts to meet its own and the Legislature’s desire that the university’s student body reflect the diversity of the State because, as of academic year 2014–15, only 11 percent of domestic undergraduate nonresidents were from underrepresented minorities.2

In addition, since academic year 2005–06 the university has increased mandatory fees—base tuition and the student services fee—for residents six times, resulting in an overall increase of 99 percent, from $6,141 to $12,240; however, the university has not conducted a usable study to determine the costs of educating its students, thereby limiting its ability to appropriately justify these tuition increases. Although the university objects to using cost studies, other states’ public university systems have developed cost studies upon which decision makers base those institutions’ tuition and funding, suggesting that such an approach is both feasible and beneficial. By using a cost study, the university would have a reasonable basis for the amount it charges for tuition.

According to the university, losses in state funding necessitated its increase in nonresident enrollment and tuition. Based on the university’s assertion that it increased nonresident enrollment because of decreased state funding and rising costs, we expected it would have decreased—or at least held constant—its nonresident enrollment when state funding began to increase; however, that was not the case. Because the university’s actions have had significant adverse repercussions for residents and their families, we believe that legislative intervention is not only warranted but necessary to ensure that a university education once again becomes attainable and affordable for all residents who are qualified and desire to attend.

On a Variety of Academic Indicators, the University Has Admitted Thousands of Nonresidents Who Were Less Qualified Than the Upper Half of the Residents It Admitted

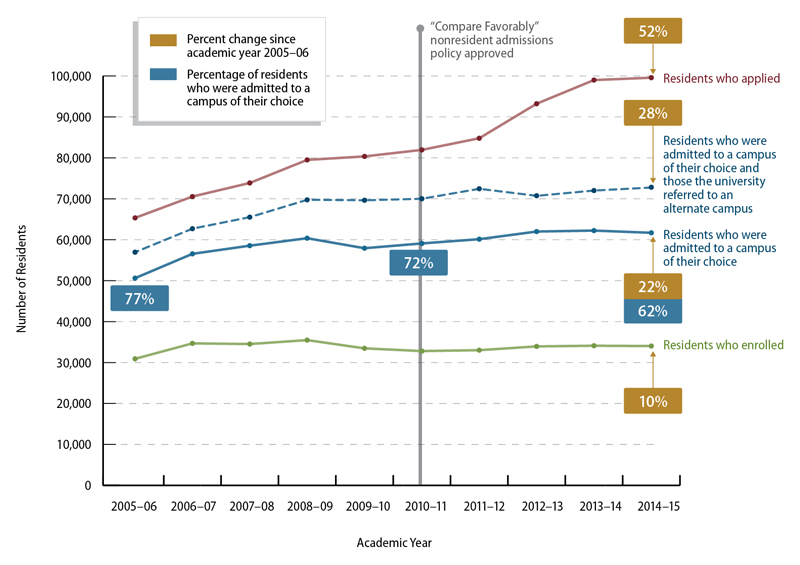

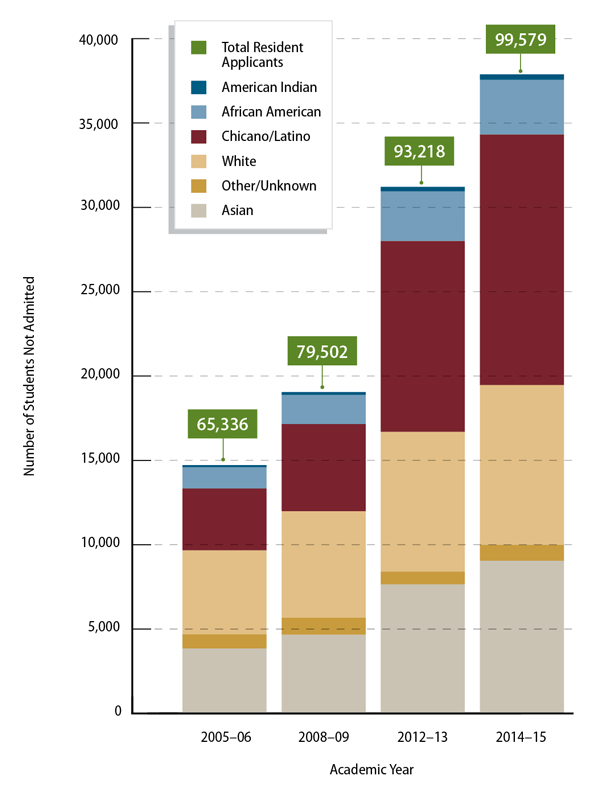

Over the past 10 years, the university has admitted thousands of nonresidents who were less qualified than the upper half of residents it admitted on every academic indicator we evaluated. At the same time, the university reduced the percentage of residents it admitted from 77 to 62 percent, and increased the percentage of nonresidents it admitted from 48 to 56 percent—nearly 21,700 nonresidents. As a result, nearly one-third of the students the university admitted in academic year 2014–15 were nonresidents. These trends cannot be attributed to a decrease in residents’ demand for a university education. On the contrary, the number of resident applications increased by nearly 22 percent from academic years 2010–11 through 2014–15, from about 82,000 applicants to nearly 100,000 applicants.

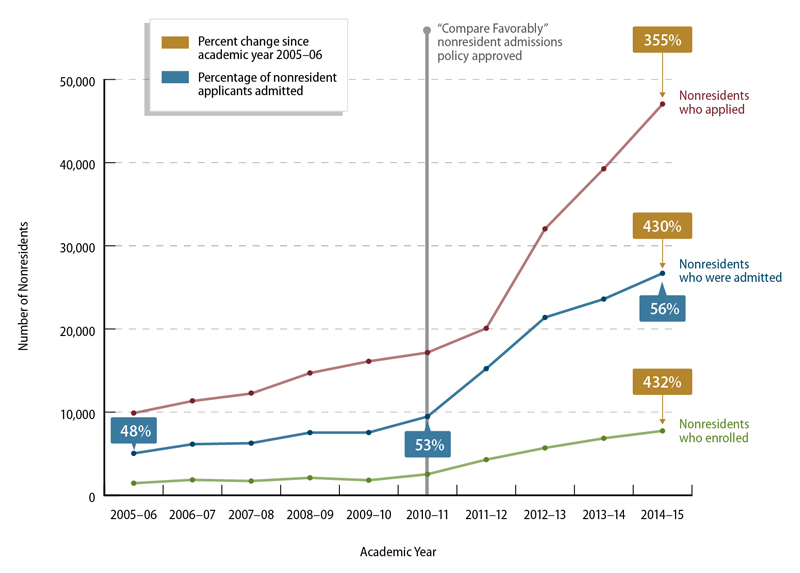

Beginning in academic year 2010–11, the trends became especially stark: The university admitted only about 2,600 more residents to a campus of their choice in academic year 2014–15 than it did in academic year 2010–11, a 4 percent increase, while during the same time it increased the number of nonresidents it admitted by more than 17,200 students, or 182 percent. Moreover, the percentage of residents the university admitted actually decreased from 72 percent in academic year 2010–11 to 62 percent in academic year 2014–15, as depicted in Figure 4. Conversely, as shown in Figure 5, over the same period the trends for nonresidents show significant increases in applications, admissions, and enrollment.

Figure 4

Despite an Increase in Resident Applicants, the University of California Has Kept Resident Undergraduate Enrollment Flat

Sources: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Undergraduate Admissions System and other operational data.

Note 1: Before academic year 2011–12, the university admitted nearly all of its referral pool to either the Merced or Riverside campus. Beginning in academic year 2011–12, the university only referred applicants to its Merced campus, and Merced began contacting referral applicants to confirm their interest in attending the campus before admitting them.

Note 2: Because an applicant can apply to multiple campuses, we count an applicant only once, regardless of the number of campuses to which the applicant applied.

Figure 5

The University of California Has Admitted and Enrolled Increasing Numbers of Nonresident Undergraduates

Sources: California State Auditor’s analysis of data obtained from the University of California Office of the President’s Undergraduate Admissions System and other operational data.

Note: Because an applicant can apply to multiple campuses, we count an applicant only once, regardless of the number of campuses to which the applicant applied.

These trends are in part caused by university policy changes. In 2011 the university revised its admission standard for nonresidents, which had the effect of making it easier for nonresidents to gain admission. The Board of Admissions and Relations with Schools (BOARS)—an entity within the university’s academic senate charged with developing admission criteria—developed the university’s policy related to nonresident undergraduate admission principles in 2009. One of the principles in the policy reflected the Master Plan’s recommendation that nonresidents should demonstrate stronger admission credentials than residents by generally requiring that nonresidents possess academic qualifications in the upper half of residents who were eligible for admission. However, BOARS made changes in 2011 that lowered the standard necessary for nonresident admission.

According to BOARS, at the time the Master Plan was written, eligibility was essentially synonymous with admission, indicating that campuses were admitting all eligible residents. However, because campuses became more selective over time, with some admitting one-quarter or fewer of their eligible applicants, in 2011 BOARS eliminated the wording in its 2009 nonresident undergraduate admission principles that nonresidents “should demonstrate stronger admissions credentials than California residents by generally being in the upper half of those ordinarily eligible” for admission. Instead, BOARS revised this principle to state that admitted nonresidents should “compare favorably to California residents admitted.” The revised principle left the application of the “compare favorably” standard up to the campuses, which BOARS believed were capable of making appropriate admission judgments. BOARS did specify, however, that as campuses recruited more nonresidents in difficult financial times, they should remember two other principles for nonresident enrollment: That nonresident enrollment should not be an exclusively revenue-producing strategy and that fiscal considerations should not be a primary factor guiding admission decisions.

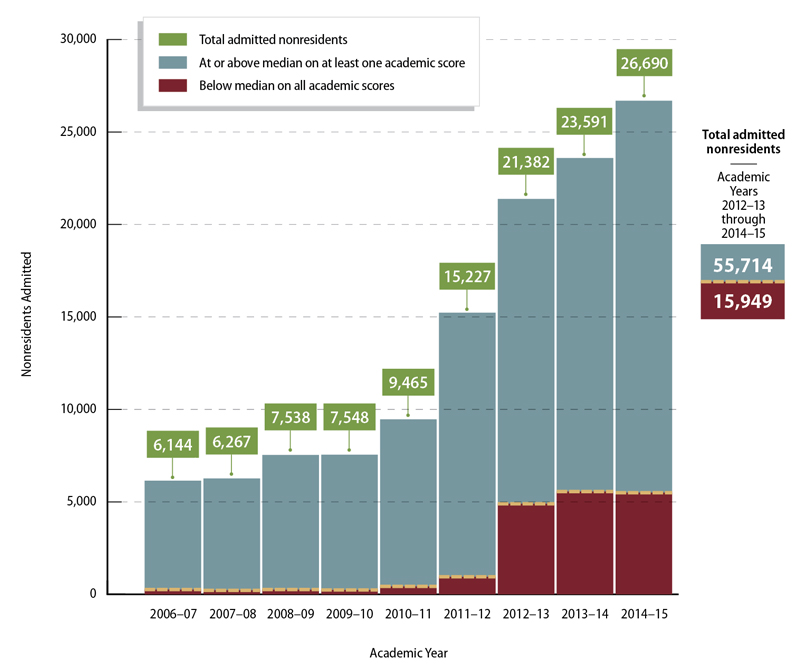

In part as a consequence of BOARS’ revision, the university admitted nearly 16,000 nonresidents from academic years 2012–13 through 2014–15 who were less academically qualified on every academic indicator we evaluated—grade point averages (GPA), SAT, and ACT scores—than the upper half of residents whom it admitted at the same campus, as shown in Figure 6. Had the university followed the Master Plan, it would not have admitted these nonresidents and could have instead admitted additional residents.

Figure 6

The University of California Admitted Nearly 16,000 Nonresident Undergraduates Over the Past Three Academic Years With Grade Point Averages and Scores on All Tests That Fell Below the Median of Admitted Residents

Sources: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Undergraduate Admissions System and other operational data.

Note 1: Academic scores include ACT Composite, ACT English Writing, ACT Math, ACT Reading, ACT Science, SAT Subject 1, SAT Subject 2, SAT Critical Reading, SAT Reading Math, SAT Writing, SAT Math, unweighted, and weighted grade point averages.

Note 2: To be consistent with Table 6, we did not include academic year 2005–06.

Note 3: We conducted our analysis based on applicants’ scores and grade point averages at each campus. If a nonresident was admitted at more than one campus with all scores and grade point averages below the median of admitted residents, we counted that nonresident only once. We included nonresidents in the “At or above median on the least one academic score” category if they had at least one score at or above the median for every campus to which they were admitted. We also included 98 nonresidents for whom the university did not provide any scores or grade point averages as at or above the median.

Furthermore, the university places extra weight on high school GPAs as a predictor of college performance. The average GPA for admitted domestic nonresidents for six of nine campuses has been lower than the GPA for admitted residents since academic year 2010–11.3 As we show in Table 5, the university’s practice of admitting domestic nonresidents with lower GPAs became widespread beginning in academic year 2010–11.

| Academic Year | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Campus | 2005–06 | 2006–07 | 2007–08 | 2008–09 | 2009–10 | 2010–11 | 2011–12 | 2012–13 | 2013–14 | 2014–15 |

| Berkeley | ||||||||||

| Resident | 4.14 | 4.15 | 4.15 | 4.16 | 4.16 | 4.18 | 4.19 | 4.19 | 4.20 | 4.20 |

| Nonresident | 4.21 | 4.22 | 4.22 | 4.23 | 4.19 | 4.13 | 4.09 | 4.13 | 4.17 | 4.18 |

| Davis | ||||||||||

| Resident | 3.88 | 3.84 | 3.89 | 3.93 | 3.99 | 4.01 | 4.03 | 4.06 | 4.10 | 4.11 |

| Nonresident | 4.03 | 3.94 | 3.98 | 4.02 | 4.01 | 3.90 | 3.86 | 3.98 | 4.00 | 3.99 |

| Irvine | ||||||||||

| Resident | 3.88 | 3.88 | 3.92 | 3.94 | 4.00 | 4.01 | 4.00 | 4.05 | 4.07 | 4.09 |

| Nonresident | 3.93 | 3.95 | 4.00 | 4.01 | 4.04 | 3.89 | 3.85 | 4.01 | 3.94 | 3.95 |

| Los Angeles | ||||||||||

| Resident | 4.11 | 4.12 | 4.13 | 4.15 | 4.16 | 4.18 | 4.18 | 4.19 | 4.21 | 4.21 |

| Nonresident | 4.17 | 4.16 | 4.17 | 4.19 | 4.17 | 4.09 | 4.06 | 4.07 | 4.11 | 4.12 |

| Merced | ||||||||||

| Resident | 3.53 | 3.53 | 3.54 | 3.52 | 3.55 | 3.56 | 3.54 | 3.58 | 3.60 | 3.63 |

| Nonresident | 3.86 | 3.88 | 3.87 | 3.82 | 3.75 | 3.70 | 3.82 | 3.74 | 3.83 | 3.74 |

| Riverside | ||||||||||

| Resident | 3.58 | 3.56 | 3.54 | 3.55 | 3.63 | 3.64 | 3.68 | 3.72 | 3.73 | 3.78 |

| Nonresident | 3.88 | 3.85 | 3.84 | 3.84 | 3.81 | 3.78 | 3.78 | 3.68 | 3.72 | 3.77 |

| San Diego | ||||||||||

| Resident | 4.05 | 4.03 | 4.06 | 4.06 | 4.09 | 4.10 | 4.13 | 4.15 | 4.17 | 4.18 |

| Nonresident | 4.10 | 4.10 | 4.12 | 4.14 | 4.11 | 4.00 | 3.99 | 3.95 | 4.00 | 4.07 |

| Santa Barbara | ||||||||||

| Resident | 3.91 | 3.89 | 3.90 | 3.93 | 3.92 | 3.99 | 4.00 | 4.00 | 4.03 | 4.05 |

| Nonresident | 4.02 | 4.02 | 4.02 | 4.04 | 4.00 | 3.90 | 3.86 | 3.89 | 3.93 | 3.98 |

| Santa Cruz | ||||||||||

| Resident | 3.68 | 3.67 | 3.66 | 3.70 | 3.75 | 3.77 | 3.76 | 3.79 | 3.87 | 3.87 |

| Nonresident | 3.89 | 3.81 | 3.93 | 3.94 | 3.92 | 3.81 | 3.80 | 3.79 | 3.72 | 3.68 |

Sources: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Undergraduate Admissions System and other operational data.

Note 1: Red highlights represent average domestic nonresident weighted grade point averages that are lower than those of resident weighted averages.

Note 2: We did not include international nonresidents in this analysis to address the university’s concern that weighted grade point averages are not comparable to those of residents.

When evaluating all academic indicators separately in the context of the Master Plan’s recommendations, the university’s admission decisions have favored nonresidents. For example, as shown in Table 6, the university has admitted nearly 61,000 nonresidents with unweighted GPA scores that fell below the upper half of residents since academic year 2006–07—nearly 36,000 of those in the past three academic years after changing its admission standard. Moreover, in academic year 2014–15 alone, the university admitted more than 9,400 nonresidents whose SAT reading math scores and more than 11,200 nonresidents whose SAT writing scores fell below the upper half of residents’ scores.

According to the university’s associate president and chief policy advisor (associate president), GPAs and test scores do not necessarily correlate to campuses’ admission decisions, largely because of the campuses’ comprehensive review processes. Moreover, she expressed concerns with the reliability of nonresident GPA data because students self-enter these data when they apply to the university. She stated that the university operates under the concept that the State must fund each resident enrolled, and because of state funding cuts, it has become more difficult for residents to gain admission. In contrast, she acknowledged that the university has made it easier for nonresidents to gain admission. Furthermore, she told us that campuses are still coming to understand how to interpret BOARS’ “compare favorably” principle and do not always interpret it correctly. She also acknowledged that the university has provided no written guidance to campuses related to interpreting the “compare favorably” principle. Nevertheless, the data suggest that the university has admitted many nonresidents who appear to be less academically qualified than residents.

| Academic Year | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Test Scores or Grade Point Averages (GPA) | 2006–07 | 2007–08 | 2008–09 | 2009–10 | 2010–11 | 2011–12 | 2012–13 | 2013–14 | 2014–15 | Total* |

| ACT Composite | 2,717 | 3,033 | 3,265 | 9,015 | ||||||

| ACT English Writing | 461 | 588 | 820 | 906 | 1,264 | 2,095 | 2,685 | 2,992 | 3,224 | 15,035 |

| ACT Math | 468 | 662 | 909 | 1,023 | 1,281 | 2,060 | 6,403 | |||

| ACT Reading | 479 | 576 | 965 | 991 | 1,320 | 2,115 | 6,446 | |||

| ACT Science | 403 | 528 | 834 | 777 | 1,105 | 1,764 | 5,411 | |||

| SAT Subject 1 | 2,538 | 2,404 | 2,864 | 2,643 | 3,547 | 5,888 | 19,884 | |||

| SAT Subject 2 | 2,439 | 2,291 | 2,728 | 2,613 | 3,631 | 6,006 | 19,708 | |||

| SAT Critical Reading | 2,549 | 2,498 | 3,138 | 3,054 | 4,237 | 7,475 | 22,951 | |||

| SAT Reading Math | 8,601 | 9,597 | 9,448 | 27,646 | ||||||

| SAT Writing | 2,645 | 2,631 | 3,162 | 3,050 | 4,248 | 7,199 | 10,267 | 10,950 | 11,241 | 55,393 |

| SAT Math | 1,983 | 1,932 | 2,330 | 2,208 | 2,734 | 4,349 | 15,536 | |||

| Unweighted GPA | 2,586 | 2,507 | 3,125 | 3,217 | 4,710 | 8,729 | 11,025 | 11,988 | 12,826 | 60,713 |

| Weighted GPA† | 2,025 | 1,813 | 2,155 | 2,352 | 4,111 | 7,468 | 9,024 | 9,148 | 9,461 | 47,557 |

Sources: California State Auditor’s analysis of data obtained from University of California’s (university) Office of the President’s Undergraduate Admissions System and other operational data.

Note 1: To count the number of nonresidents above, we compared the grade point averages (GPA) and test scores for each admitted nonresident to the median test scores of residents admitted to the same campus that year. If a nonresident was admitted to multiple campuses and had GPAs and test scores lower than the median GPAs and test scores at those campuses, we only counted the student once. We did not include academic year 2005–06 because the university used tests that were only applicable to that year of our audit scope.

Note 2: The absence of a nonresident count indicates that there were no scores for the test in the academic year.

* Nonresidents who had lower test scores or GPAs than the upper half of admitted residents.

† We did not include international nonresidents with lower weighted GPA scores in our count to address the university’s concern that those scores are not comparable to the scores of residents. However, if we had included these students, in academic year 2014–15 the total nonresidents with lower weighted GPAs would have been 17,533.

The University Established Financial Incentives That Led Campuses to Admit More Nonresidents

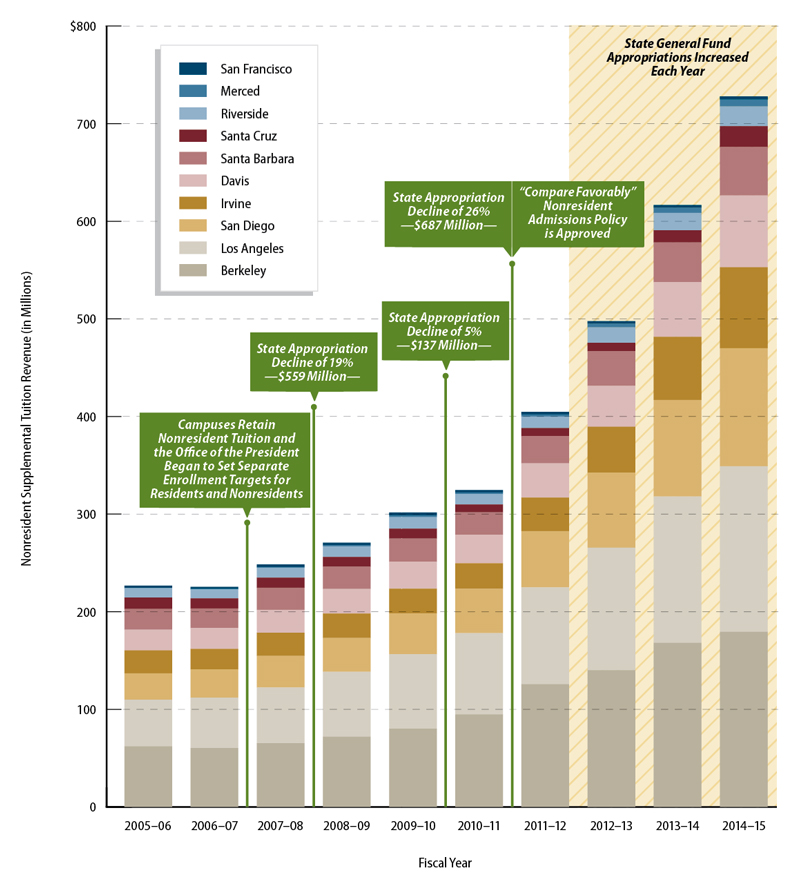

As discussed previously, many of the university’s admission decisions in recent years appear to have been significantly influenced by its desire to increase nonresident revenue. In addition to the mandatory fees—base tuition and student services fee—of $12,240 that both resident and nonresident undergraduates paid in 2015, each undergraduate nonresident paid a supplemental tuition of $24,708 for a total of about $37,000 annually. In fiscal year 2014–15, the total revenue the university generated from nonresident supplemental tuition amounted to $728 million. To maximize this revenue source, the university changed two key processes in 2008 that had the effect of incentivizing campuses to increase nonresident enrollment.

The university enacted the first key procedural change to allow campuses to retain the nonresident revenue they generated beginning with fiscal year 2007–08. Before that time, the university required campuses to return all nonresident revenue to the Office of the President for subsequent distribution among all campuses. Not surprisingly, when the Office of the President enacted this new policy, nonresident revenue began an unprecedented increase that continued into fiscal year 2014–15. Figure 7 shows the timing of the university’s 2008 procedure changes and its adoption of the “compare favorably” standard for nonresident admission in relation to its three reductions in state funding since fiscal year 2005–06.

Certain campuses gained more from this opportunity than others. In particular, Berkeley, Los Angeles, and San Diego benefited because of their pre-existing ability to attract nonresidents. For example, in fiscal year 2007–08, the Berkeley campus generated $65 million in nonresident revenue, and by fiscal year 2014–15, that amount grew to $179 million. In contrast, the Santa Cruz campus generated $10 million in nonresident revenue in fiscal year 2007–08 and $21 million in fiscal year 2014–15. As we will discuss in Chapter 3, the disparity in the amount of nonresident revenue the campuses generate has exacerbated per-student funding inequities.

The second key procedural change occurred in 2008 when the Office of the President began to set systemwide enrollment targets for residents and nonresidents. An enrollment target is the number of students that the university and its campuses endeavor to enroll each year. Following this 2008 procedural change, three of the campuses we visited began setting separate enrollment targets for nonresidents in academic year 2010–11: Los Angeles, San Diego, and Santa Barbara; and Davis began setting nonresident enrollment targets in academic year 2011–12. This time frame corresponds to the beginning of a period of rapidly increasing nonresident enrollment at the university. The campuses we visited provided us information showing that during this period, each increased its nonresident enrollment targets more rapidly than it increased its resident enrollment targets.

Those campuses acknowledged that a desire for additional revenue was part of the reason they increased their nonresident enrollment targets. For example, the San Diego campus’s new resident freshman enrollment target increased by only 10 percent from fall 2011 through fall 2014—from 3,375 to 3,700. In contrast, it increased its new nonresident freshman enrollment target by 300 percent, from 300 to 1,200.

Figure 7

Nonresident Supplemental Tuition Revenue by Campus From Fiscal Years 2005–06 Through 2014–15

Sources: California State Auditor’s analysis of revenue data provided by the University of California’s Office of the President generated from its Corporate Financial System and other information provided by the Office of the President.

Factors That University of California Campuses May Consider When Admitting Students

- Grade point average for courses required by the University of California (university).

- Scores on the SAT Reasoning Test or ACT with Writing.

- Number, content, and performance in other high school academic courses.

- Number and performance in university-approved honors and Advanced Placement courses.

- Identification by the university that an applicant is in the top 9 percent of his or her high school class.

- Quality of senior-year course schedule.

- Quality of the applicant’s academic performance in relation to the opportunities available at his or her high school.

- Outstanding performance in one or more academic subject areas.

- Outstanding work in one or more special projects in any academic field of study.

- Recent, marked improvement in academic performance.

- Special talents, achievements, and awards in a particular field that demonstrate the applicant’s promise for contributing to the intellectual vitality of a campus.

- Completion of special projects in the context of the applicant’s high school curriculum or school events, projects, or programs.

- Academic accomplishments in light of the student’s life experiences and special circumstances.

- Location of the student’s secondary school and residence.

Source: The university’s website.

As a result of establishing separate enrollment targets, the campuses were able to admit nonresidents who were less academically qualified than residents, an outcome we substantiated in the previous section. The process for evaluating applications at a campus, known as the comprehensive review, involves ranking applicants on many different factors, as listed in the text box. These factors include GPA, test scores, and life experiences. After the campus has ranked applications, it selects applicants to admit in bands based on their holistic review scores and other campus‑specific factors, such as the need to fill enrollment targets for departments and majors. When the campus has selected a sufficient number of students to meet those enrollment targets, it then admits additional applicants if needed to ensure that it meets its overall campus targets for resident and nonresident enrollment. Conceivably, a campus could meet its resident enrollment target before meeting its nonresident enrollment target. If this happened, the campus could cut off admission of residents but continue to admit nonresidents who were ranked lower than residents until the campus met its nonresident enrollment target. Two of the four campuses we visited confirmed that such an outcome was possible although they believed it was not likely.

Finally, in 2008 the university informed campuses that they would be responsible for any lost revenue should they decide to reduce their nonresident enrollment targets. Moreover, when the university adopted its funding streams initiative in 2011, which directed campuses to retain all tuition funds they generate, one of the stated goals of the initiative was to incentivize campuses to maximize revenue.

The University Has Admitted Fewer Residents to the Campuses of Their Choice and Increasing Numbers of Nonresidents Have Enrolled in the Most Popular Majors

In addition to admitting nonresidents who are less academically qualified than the upper half of admitted residents, the university also admitted fewer residents to the campuses of their choice over the past several years. Specifically, the percentage of residents to whom the university denied admission to their campuses of choice increased from 23 percent in academic year 2005–06 to 38 percent in academic year 2014–15. If residents are eligible for admission to the university and the campuses of their choice do not offer them admission, the university offers them a spot at an alternative campus through what it calls a referral process. Under this process, eligible residents not admitted to any of the campuses to which they applied are placed into a referral pool. These residents can then accept admittance to an alternate campus, which is currently limited to Merced. According to the university, the referral process is critical to its meeting its Master Plan commitment to admit the top 12.5 percent of residents. However, very few residents actually enroll at the campus to which they are referred. Conversely, the university does not refer nonresidents to alternate campuses.

From academic years 2005–06 through 2014–15, the number of residents offered admission through referral to alternate campuses increased by 79 percent—from about 6,000 to 10,700 applicants—as shown in Table 7. Of particular concern is that, over the same time period, the university’s campuses denied admission to nearly 4,300 residents whose academic scores met or exceeded all of the median scores for nonresidents whom the university admitted to the campus of their choice. Moreover, between academic years 2005–06 and 2010–11, when the university’s policy was to refer residents to both the Riverside and Merced campuses, an average of only 6 percent of those residents enrolled at the campus to which they were referred. Since academic year 2011–12, when the university began referring residents only to the Merced campus, the number of residents it placed in the referral pool increased to an average of 10,100 per year, but the average number of residents enrolling dropped to just over 2 percent, or an average of 155 enrollees per year. In comparison, when the university admitted residents to a campus to which they applied from academic years 2011–12 through 2014–15, 55 percent of residents accepted and enrolled at that campus.

| Academic Year | Number of Residents Admitted to a campus to which they applied | Number of residents In the Referral Pool | Number of residents in the Referral Pool Who Enrolled | Enrollment Rate for residents in the Referral Pool | Enrollment Rate for residents Admitted to a Campus to Which They Applied |

|---|---|---|---|---|---|

| 2005–06 | 50,614 | 5,981 | 357 | 6% | 60% |

| 2006–07 | 56,556 | 5,784 | 391 | 7 | 61 |

| 2007–08 | 58,549 | 6,606 | 434 | 7 | 58 |

| 2008–09 | 60,373 | 9,012 | 579 | 6 | 58 |

| 2009–10 | 57,927 | 11,348 | 706 | 6 | 57 |

| 2010–11 | 59,099 | 10,545 | 355 | 3 | 55 |

| 2011–12 | 60,136 | 11,940 | 159 | 1 | 55 |

| 2012–13 | 62,002 | 8,360 | 134 | 2 | 55 |

| 2013–14 | 62,238 | 9,411 | 131 | 1 | 55 |

| 2014–15 | 61,697 | 10,688 | 195 | 2 | 55 |

Source: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Undergraduate Admissions System and other operational data.

Note 1: Before academic year 2011–12, the university admitted nearly all of its referral pool to either the Merced or Riverside campus. Beginning in academic year 2011–12, the university only referred applicants to its Merced campus, and Merced began contacting referral applicants to confirm their interest in attending the campus before admitting them.

Note 2: The referral pool excludes residents who were referred but later admitted to a campus to which they applied. Instead, these residents are included in the column titled Number of Residents Admitted to a Campus to Which They Applied.

In addition to denying admission to the campuses of their choice to increasing numbers of residents, the university has also allowed increasing numbers of nonresidents to enroll in the most popular majors. As Table 8 illustrates, from academic year 2010–11 through 2014–15, the five most popular majors that the university offers saw significant increases in nonresident growth at Berkeley, Irvine, Los Angeles, and San Diego—between about 1,100 to 2,100 students coupled with generally declining resident enrollment—about 800 to 1,200 students in three of the four campuses. The university asserts that these enrollment changes may be the result of a mixture of student behavior, increasing nonresident applications, and evolving major offerings at the campuses. For example, the university noted that the addition of several health service majors at the Irvine campus may have resulted in decreases to campus-level enrollment in biological and life science majors.

| Residents | Nonresidents | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Berkeley | Academic Year 2010–11 | Academic Year 2014–15 | Change in Enrollment | Percent of change | Academic Year 2010–11 | Academic Year 2014–15 | Change in Enrollment | Percent of Change | |

| Biological/Life Sciences | 1,479 | 1,295 | (184) | (12)% | 126 | 264 | 138 | 110% | |

| Social Sciences | 2,371 | 2,123 | (248) | (10) | 272 | 668 | 396 | 146 | |

| Engineering | 2,697 | 2,357 | (340) | (13) | 603 | 1,077 | 474 | 79 | |

| Psychology | 519 | 508 | (11) | (2) | 33 | 79 | 46 | 139 | |

| Business and Management | 510 | 487 | (23) | (5) | 95 | 145 | 50 | 53 | |

| Irvine | |||||||||

| Biological/Life Sciences | 4,217 | 2,842 | (1,375) | (33)% | 90 | 158 | 68 | 76% | |

| Social Sciences | 2,881 | 2,759 | (122) | (4) | 98 | 350 | 252 | 257 | |

| Engineering | 2,440 | 2,954 | 514 | 21 | 91 | 357 | 266 | 292 | |

| Psychology | 1,884 | 1,933 | 49 | 3 | 50 | 138 | 88 | 176 | |

| Business and Management | 1,690 | 1,438 | (252) | (15) | 135 | 575 | 440 | 326 | |

| Los Angeles | |||||||||

| Biological/Life Sciences | 4,773 | 5,227 | 454 | 10% | 463 | 911 | 448 | 97% | |

| Social Sciences | 4,432 | 4,413 | (19) | 0 | 499 | 1,221 | 722 | 145 | |

| Engineering | 2,486 | 2,045 | (441) | (18) | 506 | 647 | 141 | 28 | |

| Psychology | 2,217 | 2,463 | 246 | 11 | 220 | 475 | 255 | 116 | |

| Business and Management | 920 | 1,126 | 206 | 22 | 227 | 731 | 504 | 222 | |

| San Diego | |||||||||

| Biological/Life Sciences | 5,036 | 5,252 | 216 | 4% | 215 | 703 | 488 | 227% | |

| Social Sciences | 3,309 | 2,178 | (1,131) | (34) | 376 | 824 | 448 | 119 | |

| Engineering | 3,414 | 4,070 | 656 | 19 | 238 | 784 | 546 | 229 | |

| Psychology | 1,495 | 966 | (529) | (35) | 45 | 155 | 110 | 244 | |

| Business and Management | 765 | 543 | (222) | (29) | 77 | 234 | 157 | 204 | |

Sources: California State Auditor’s analysis of data obtained from the University of California (university), Office of the President’s UC Information Center Enrollment Data Mart.

Notes: We defined the most popular majors as those with the largest total undergraduate enrollment systemwide.

We focused our analysis on campuses that had the highest percentage of undergraduate nonresidents (both domestic and international) within the last five academic years.

The resident enrollment column totals include certain students whom the university Board of Regents’ policy exempts from nonresident tuition consistent with Assembly Bill 540 (Chapter 814, Statutes of 2001).

Underrepresented Students Comprise Less Than 30 Percent of the University’s Undergraduate Student Population

The university’s recent emphasis on enrolling more nonresidents has hampered its efforts to meet its own and the Legislature’s desire that the university’s student body reflect the diversity of the State. A 1991 state law recommended that the university enroll a student body that reflected the cultural, racial, geographic, economic, and social diversity of the State. The university had issued a policy in 1988 stating a similar intention, noting its commitment to provide places for all eligible resident applicants and its desire to enroll a student body that, beyond meeting eligibility requirements, encompasses California’s broad diversity characteristics. In 1996, a constitutional amendment, Proposition 209, prohibited the university from admitting students based on a number of factors including race or ethnicity. Nonetheless, recognizing this prohibition, the university also acknowledged a need to remove barriers to the recruitment, retention, and advancement of students from underrepresented minorities.4

As shown in Table 9, since academic year 2005–06, the university has progressively increased the percentage of underrepresented minorities among the resident undergraduates that it enrolls, raising this percentage from 19 percent in academic year 2005–06, to 24 percent in academic year 2010–11, and most recently to 30 percent in academic year 2014–15. As also shown in Table 9, the percentages of underrepresented minorities for both resident and domestic nonresident graduate students grew slightly to 17 percent and 15 percent, respectively, by academic year 2014–15. The table also shows that the university’s graduate students predominantly identify their ethnicity as Asian or white.

| Percentage of Students by Academic Year | Growth in Undergraduate Enrollment From Academic Years 2010–11 Through 2014–15 | ||||

|---|---|---|---|---|---|

| 2005–06 | 2010–11 | 2014–15 | |||

| UNDERGRADUATES | |||||

| Residents* | |||||

| African American | 3% | 4% | 4% | (0.04)% | |

| American Indian | 1 | 1 | 1 | ||

| Asian | 38 | 39 | 39 | ||

| Chicano/Latino | 15 | 19 | 25 | ||

| Other/Unknown | 9 | 7 | 4 | ||

| White | 35 | 31 | 27 | ||

| Underrepresented Minorities† | 19 | 24 | 30 | ||

| Nonresidents (Domestic) | |||||

| African American | 2% | 3% | 4% | 80% | |

| American Indian | 1 | 1 | 1 | ||

| Asian | 37 | 41 | 46 | ||

| Chicano/Latino | 4 | 5 | 6 | ||

| Other/Unknown | 10 | 7 | 4 | ||

| White | 47 | 43 | 40 | ||

| Underrepresented Minorities† | 7 | 9 | 11 | ||

| Nonresidents (International) | |||||

| American Indian | 0% | 0% | 0% | 214% | |

| Asian | 83 | 87 | 91 | ||

| Black | 1 | 1 | 1 | ||

| Chicano/Latino | 2 | 1 | 1 | ||

| Other/Unknown | 7 | 5 | 3 | ||

| White | 8 | 6 | 4 | ||

| All Undergraduates | |||||

| African American | 3% | 4% | 4% | 9% | |

| American Indian | 1 | 1 | 1 | ||

| Asian | 39 | 41 | 44 | ||

| Black | 0 | 0 | 0 | ||

| Chicano/Latino | 14 | 18 | 22 | ||

| Other/Unknown | 9 | 6 | 4 | ||

| White | 35 | 31 | 25 | ||

| Percentage of Students by Academic Year | Growth in Graduate Enrollment From Academic Years 2010–11 Through 2014–15 | ||||

| 2005–06 | 2010–11 | 2014–15 | |||

| GRADUATES | |||||

| Residents* | |||||

| African American | 3% | 3% | 4% | (6)% | |

| American Indian | 1 | 1 | 1 | ||

| Asian | 21 | 21 | 23 | ||

| Chicano/Latino | 9 | 10 | 12 | ||

| Other/Unknown | 15 | 16 | 11 | ||

| White | 52 | 49 | 49 | ||

| Underrepresented Minorities† | 13 | 14 | 17 | ||

| Nonresidents (Domestic) | |||||

| African American | 4% | 5% | 6% | 18% | |

| American Indian | 1 | 1 | 1 | ||

| Asian | 14 | 16 | 16 | ||

| Chicano/Latino | 5 | 7 | 8 | ||

| Other/Unknown | 16 | 11 | 11 | ||

| White | 60 | 61 | 58 | ||

| Underrepresented Minorities† | 10 | 13 | 15 | ||

| Nonresidents (International) | |||||

| American Indian | 0% | 0% | 0% | 24% | |

| Asian | 24 | 33 | 38 | ||

| Black | 0 | 0 | 1 | ||

| Chicano/Latino | 2 | 3 | 5 | ||

| Other/Unknown | 69 | 57 | 47 | ||

| White | 5 | 7 | 10 | ||

| All Graduates | |||||

| African American | 2% | 2% | 3% | 4% | |

| American Indian | 1 | 1 | 1 | ||

| Asian | 23 | 24 | 27 | ||

| Black | 0 | 0 | 1 | ||

| Chicano/Latino | 7 | 8 | 9 | ||

| Other/Unknown | 22 | 22 | 19 | ||

| White | 45 | 42 | 40 | ||

Sources: California State Auditor’s analysis of data obtained from the University of California (university), Office of the President’s UC Information Center Enrollment Data Mart.

* Residents include certain students whom the university Board of Regents’ policy exempts from nonresident tuition consistent with Assembly Bill 540 (Chapter 814, Statutes of 2001).

† The university considers underrepresented minorities to be African Americans, Chicanos/Latinos, and American Indians.

Note 1: The other/unknown category contains both those students with unknown ethnicity and international students that the university categorized as qualifying for resident status.

Note 2: The total percentages may not equal 100 percent due to rounding.

Note 3: We did not provide separate breakdowns of Graduate Self-Supported or Medical Resident student ethnicities because the university does not distinguish the residency status of students enrolled in those programs. However, we included students enrolled in both programs in the All Graduates table above.

The university’s effort to increase the enrollment of underrepresented minorities among resident students is commendable, but the university’s overall undergraduate student body does not yet encompass the State’s diversity characteristics. According to statistics from the Department of Finance, underrepresented minorities comprised 45 percent of California’s population in 2014. Despite raising California undergraduate enrollment of underrepresented minorities to 30 percent in academic year 2014–15, the university needs to make additional progress to raise the level of underrepresented minorities enrolled to mirror the 45 percent of the State’s overall population.

However, the university’s emphasis on enrolling increasing numbers of nonresidents has hampered its efforts to enroll more underrepresented minorities because only 11 percent of enrolled nonresident domestic undergraduate students were from underrepresented minorities as shown in Table 9. In fact, as of academic year 2014–15, roughly 86 percent of undergraduate domestic nonresident students identified their ethnicity as Asian or white. The university has more than tripled its population of undergraduate nonresidents since academic year 2005–06, resulting in underrepresented minorities comprising less than 30 percent of the university’s total undergraduate population. According to the university, its goal for resident undergraduates is to reflect the diversity of the State, while it seeks to increase geographic diversity by enrolling nonresidents. Although nonresidents bring geographic diversity to the university’s overall student population, increasing the number of nonresidents has slowed its progress in aligning the university’s percentages of underrepresented minorities with those of the State’s percentages.

Furthermore, in academic year 2005–06, the university denied admission to the campus of their choice to about 23 percent of undergraduate residents who applied, and by academic year 2014–15, that percentage had grown to 38. As shown in Figure 8, the university increasingly denied admission to residents of all ethnicities. Figure 8 also shows the increasing trend in resident applications, which contributed to the increasing rates of denial. Although the university cannot consider race or ethnicity when making admissions decisions, the university continues to deny admission to underrepresented minorities at higher rates than residents who identify their ethnicity as Asian or white. In particular, in academic year 2014–15, the university denied admission to 47 percent of underrepresented minority applicants, and to 32 percent of applicants who identified their ethnicity as Asian or white.

Figure 8

Ethnicities of Resident Undergraduates Who Were Denied Admission to the Campuses of Their Choice

Sources: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Undergraduate Admissions System and other operational data.

Note 1: The university considers underrepresented minorities to be African Americans, Chicanos/Latinos, and American Indians.

Note 2: Some students to whom the university denied admission to the campuses of their choice ultimately enrolled at an alternate referral campus, as shown in Table 7.

Moreover, many of the underrepresented minorities to whom the university denied admission to the campus of their choice might have been qualified to attend the campus to which they applied. Specifically, as noted earlier in this chapter, the university’s campuses denied admission to nearly 4,300 residents from academic years 2005–06 through 2014–15 whose academic scores met or exceeded the median scores of admitted nonresidents on every academic indicator we evaluated. More than 450 of those were resident underrepresented minorities. This number suggests that the university denied admission to more than 450 underrepresented minorities—364 of those in the last three academic years—who were at least as academically qualified as certain admitted nonresidents.

The University Has Not Sufficiently Justified Resident Tuition Increases

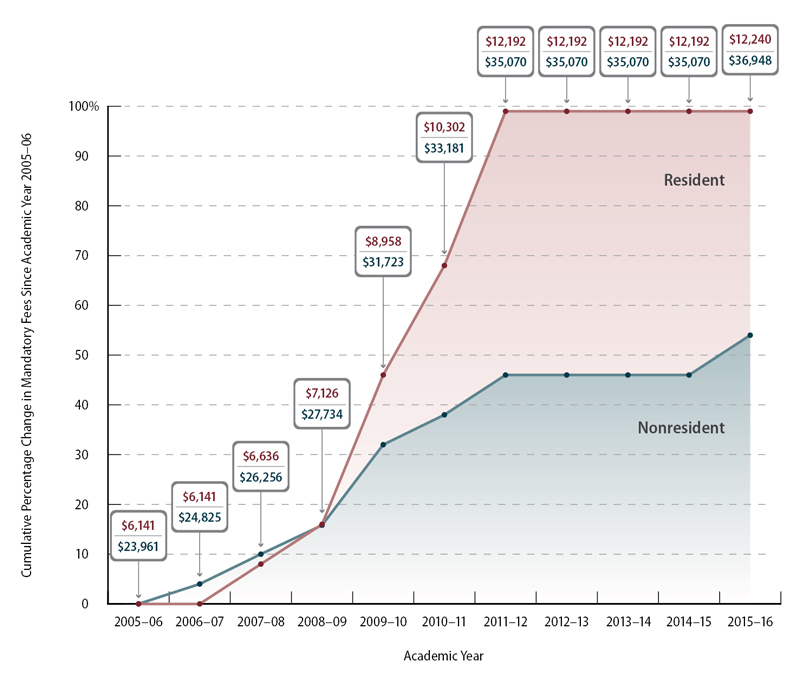

Over the past 10 years, the university has repeatedly increased the cost of tuition without sufficient justification and to the detriment of California families. Since academic year 2005–06, the university has increased mandatory fees—base tuition and the student services fee—for residents six times and at varying rates resulting in an overall increase of 99 percent, from $6,141 in academic year 2005–06 to $12,240 in academic year 2015–16, as shown in Figure 9. Over the same time frame, median household income in California decreased by nearly 4 percent, from more than $62,700 in 2005 to $60,500 in 2014. This income decrease, coupled with the unpredictable timing and amount of tuition increases, has likely made it difficult for families to effectively budget for this important investment.

We expected the university to have based any tuition increases on its actual cost of instruction; however, according to the university’s associate vice president of budget analysis and planning (budget associate vice president), the university does not base tuition on the cost of instruction. Instead, it uses a model to estimate its future budget needs and expected revenue, then increases tuition to fill any estimated revenue gap. She explained that the university looks at how proposed tuition levels will compare with other public institutions to determine whether an increase is justified.

In fact, even though it is required, the university has not conducted a usable study to determine the costs of educating its students, thereby limiting its ability to appropriately justify tuition increases. The Legislature required the university to submit a report every two years beginning in 2014 on the total costs of education at the university, disaggregated by academic discipline. In the report issued in 2015, the university took issue with the methodology the Legislature requested and instead provided a range of costs, one based on what it called the Legislature’s “narrow definition” and a broader definition it considered more complete. However, the university cautioned that decision makers should not use the report as a solid rationale for making policy decisions or allocating resources because the assumptions, estimates, and proxies for data it had used to calculate the costs it reported could result in unreliable estimates.

Figure 9

The University of California Has Significantly Increased Undergraduate Mandatory Fees

Source: The University of California 2015–16 Budget for Current Operations.

Resident mandatory fees include base tuition and student services fee.

Nonresident mandatory fees include base tuition, student services fee, and nonresident supplemental tuition.

The university’s cost study is problematic because the source of the data it uses is not apparent, and it does not tie the costs and funding it reported to readily available and public financial data, such as its audited annual financial report. By contrast, the National Association of College and University Business Officers (national association) developed a cost model for universities to clearly outline the annual costs of education based on either the indirect cost rate study they prepare for the federal government or their audited financial statements, both of which are verified and readily available sources of financial information. The university chose not to use the national association model because it disagreed with some of its assumptions. Despite the university’s reluctance to produce a cost study because it disagrees with the prescribed methodology or because it believes the underlying cost accounting data for a detailed cost study are difficult and expensive to obtain, the university should develop a reasonable, well-supported methodology and use it as the basis for funding requests and tuition increases.

In addition to the methodology the national association created, other public university systems have developed thorough cost studies which decision makers can assess when considering tuition increases or funding requests, suggesting that such an approach is both feasible and beneficial. For instance, Texas uses actual expenditures to calculate the relative educational costs per student academic level and discipline. Every two years, the Texas state legislature uses this cost study to make funding decisions. According to the university, the cost study approach used by other states—primarily Texas—is overly complex. However, our review found that the process Texas employs is relatively straightforward because it uses operating cost elements that campuses report in their annual financial statements and enrollment data. Furthermore, the University of Texas at Austin, one of the schools within the University of Texas system, uses the results of its state’s cost study as one of the main factors—along with tuition rates that other universities charge, its projected cost increases, and its priorities—to determine the tuition it charges students.

By performing a cost study, the university could find, for example, that the amount it actually costs to educate students could justify its need to increase—or decrease—the amount it charges for tuition. An accurate calculation of costs also could serve as a foundation that the Legislature and the university could use to determine reasonable levels of financial support from both the State and from students.

Legislative Intervention Could Help to Ensure That the University Meets Its Commitment to Residents

The university’s decision to increase nonresident enrollment at the expense of residents will have a long‑lasting impact unless the Legislature and the university take steps to restore the university’s historic commitment to residents. These steps must not only ensure that the university prioritizes residents’ interests in the future but also repairs the damage that its past decisions have caused. In November 2015—during the course of our audit—the university committed to enrolling an additional 10,000 more residents over the next three fiscal years. However, the enrollment of 10,000 additional residents will not fully rectify the ramifications of its decision to admit nonresidents while referring or denying admission to more qualified resident applicants.

Based on the university’s assertion that it increased nonresident enrollment because of decreases in state funding and rising costs, we would have expected it to decrease—or at least hold constant—its nonresident enrollment when state funding began to increase. Instead, as previously shown in Figure 3, state funding has been increasing steadily since fiscal year 2012–13. However, the university has acknowledged that it intends to continue to admit increasing numbers of nonresidents, and in its 2016–17 operating budget, the university indicated that nonresident revenue continues to be a key part of its financial plan. Thus, until the university’s financial incentive to enroll nonresidents is mitigated, it will likely continue to admit increasing numbers of nonresidents.

The university’s 2010 Commission on the Future report acknowledged the potential benefits and challenges of increasing nonresident enrollment. This report asserted that the university had low proportions of nonresident undergraduates compared to other public and private research universities and recommended that it increase nonresident enrollment to 10 percent. Such an increase, the report stated, would generate additional revenue to sustain current instructional capacity and educational offerings for all undergraduates. Further, the report stated that increasing the number and proportion of nonresidents would enhance undergraduates’ educational experience, broaden geographical diversity, and prepare students for a global society.

However, the report cautioned that campuses must establish targets for nonresident enrollment that do not displace funded enrollment of California residents and that the admission of nonresident undergraduates should not displace funded California residents who are eligible for admission. The report indicated that the university should cap this increase in nonresident enrollment at 10 percent, and it should also consider creating a systemwide referral pool for nonresidents and determining the areas to which each campus should dedicate the revenue from increased nonresident enrollment. However, the university has not taken these actions. Instead, total nonresident undergraduate enrollment stands at 13.4 percent for academic year 2014–15; the university does not put nonresidents in the referral pool; and the Office of the President has not given campuses specific direction on how to dedicate the increased revenue from nonresident enrollment.

We believe that the Legislature should consider amending state law to limit nonresident undergraduate enrollment at the university, which would ensure that the university does not displace residents. For example, between academic years 2005–06 and 2007–08, before the drop in state funding, nonresidents comprised about 5 percent of the university’s new undergraduate enrollment.5 By academic year 2014–15, that percentage had climbed to more than 17 percent, which translated to 7,200 new nonresident undergraduates above a 5 percent limit on new nonresident enrollment. Decreasing new nonresident enrollment by 7,200 would make the same number of spots available for residents to maintain the 5 percent limit of new nonresident undergraduates to new resident undergraduates.

Requiring the university to enroll significantly more resident undergraduates would require an additional financial commitment from both the university and the State. As we show in Table 10, different enrollment limits on new nonresident enrollment with a corresponding increase in resident enrollment would require additional revenue, which either the university or the State—or both—would need to provide. For example, if the university’s total expenditures remained constant and it increased enrollment by 7,200 residents to correspond to the 5 percent limit on new nonresident undergraduate enrollment, the university would require additional revenue of $72 million, or $10,000 per student—the amount that the university asserts it would need to fund resident enrollment growth.

If the Legislature were also to commit additional funds to the university for meeting an agreed-upon enrollment percentage, it could do so using a phased-in approach. For example, the Legislature could require the university to achieve a 5 percent limit on overall nonresident undergraduate enrollment within four years and it could provide the university with incremental increases in appropriations each year until the university reached that target. For example, year one would require a $72 million additional investment over the fiscal year 2014–15 baseline appropriation. Similarly, following the recommendation in the university’s Commission on the Future report, if the cap on nonresident enrollment was set at 10 percent, year one would require $42 million in funding. As we discuss later in this report, we believe the university could also generate additional savings internally, which could help it compensate for the lost nonresident revenue.

Finally, even though the university asserts that enrolling more nonresidents has not precluded it from meeting its Master Plan commitment to select from the highest achieving students in the State—the top 12.5 percent of all California high school graduates—the university’s admission decisions call into question whether it has actually met this commitment. As we discussed earlier in this chapter, few residents accept the university’s referrals to the Merced campus; nonetheless, the university identifies its referral process as playing a major role in fulfilling the goals of the Master Plan. According to the university, it estimated admitting the top 14.9 percent of the eligible California high school graduating class in academic year 2014–15, which includes residents in the referral pool. If we exclude the residents the university placed in the referral pool and who did not ultimately enroll at the referral campus, the university would have admitted 12.4 percent of the eligible California high school graduating class—less than the 12.5 percent Master Plan commitment. Because placements in the referral pool result in significantly fewer enrollments of residents than do admissions to a campus to which a resident applied, we question whether the university should include referral admissions when computing its admission of the top 12.5 percent of California high school graduates. To remedy this problem, the Legislature should consider requiring that the university exclude placements in the referral pool when determining whether it meets the Master Plan tenet to admit the top 12.5 percent of high school graduates until more residents actually enroll at the referral campus.

| New Undergraduate Nonresident Enrollment |

Overall Undergraduate Nonresident Enrollment | |||||

|---|---|---|---|---|---|---|

| Desired percentage of New Annual Undergraduate Nonresident Enrollment | Desired Number of New Annual Nonresident Enrollments (using academic year 2014–15 new enrollment) | Change from Actual Academic Year 2014–15 Nonresident New Enrollment to Desired | Additional Funding needed to enroll corresponding number of residents at $10,000 per student (in millions) | Total Nonresident Enrollment Percentage | Total Enrolled Undergraduate Nonresidents at that Percentage (using academic year 2014–15 enrollment) | |

| 5% | 2,940 | (7,158) | $72 | 5% | 9,754 | |

| 10 | 5,880 | (4,218) | 42 | 10 | 19,508 | |

| 15 | 8,820 | (1,278) | 13 | 26,200* | ||

| 10,098† | – | – | 15 | 29,262 | ||

| 20 | 11,760 | 1,662 | – | 20 | 39,016 | |

Sources: California State Auditor analysis of fiscal year 2014–15 admission and enrollment data obtained from the University of California (university) Office of the President’s University Undergraduate Admissions System and other operational data, University UC Information Center Enrollment Data Mart, the university’s Information Center, and the university’s 2015–16 Budget for Current Operations.

Note: New undergraduate enrollment includes incoming freshman and transfer students.

* This is the actual nonresident enrollment total for academic year 2014–15 as of the third week of the fall term.

† This is the actual new nonresident enrollment total for academic year 2014–15.

Recommendations

To meet its commitment to California residents, the university should do the following:

- Replace its “compare favorably” policy with a new admission standard for nonresident applicants that reflects the intent of the Master Plan. The admission standard should require campuses to admit only nonresidents with admissions credentials that place them in the upper half of the residents it admits.

- Amend its referral process by taking steps to increase the likelihood that referred residents ultimately enroll.

To ensure that campuses’ interpretations of admission standards do not adversely impact residents, the university should implement a thorough process to annually evaluate the qualifications of students who apply and students who are admitted. These evaluations should highlight instances when campuses admit nonresidents who are less qualified than residents and should include corrective action steps. Moreover, this evaluation should include resident and nonresident undergraduate enrollment in majors at each campus. The university should make the results of this evaluation—including details of the academic qualifications of students who applied and who were admitted—publicly available.

To ensure that it has accurate information upon which to make funding decisions, the Legislature should consider amending the state law that requires the university to prepare a biennial cost study. The amendment should include requirements for the university to differentiate costs by student academic level and discipline and to base the amounts it reports on publicly available financial information. In the absence of legislative action, the university should conduct a cost study every three to five years and ensure that it is based upon publicly-available financial information. The university should use the results of the cost studies as a basis for the tuition it charges and for the proposed funding needs that it presents to the Legislature.

To ensure that the university does not base future admission decisions on the revenue that students generate, the Legislature should consider amending state law to limit the percentage of nonresidents that the university can enroll. For example, the Legislature could require that the university limit nonresident enrollment to 5 percent of total undergraduate enrollment. To accomplish this, the Legislature should consider requiring that the university’s annual appropriations be based on enrolling agreed‑upon percentages of residents and nonresidents.

To ensure that the university meets its commitment to residents and to bring transparency and accountability to admission outcomes, the Legislature should consider excluding the students who the university places in the referral pool and who do not ultimately enroll at the referral campus when calculating the university’s Master Plan admission rate until the percentage of students who enroll through the referral process more closely aligns with that of the other campuses.

Chapter 2

The University of California Did Not Sufficiently Reduce Its Costs Before Increasing Tuition and Nonresident Enrollment

Chapter Summary

Before it increased its tuition and nonresident enrollment to address its funding shortfalls, the University of California (university) could have done more to improve its operational efficiencies and reduce costs. For example, when the Legislature required the university to enroll an additional 5,000 residents in academic year 2016–17 as a stipulation of receiving $25 million in state funds, an action the university estimates will cost approximately $50 million, or $10,000 per student, the university indicated it would use other funding sources to cover the remaining $25 million. The university indicated that it would make these funds available primarily by eliminating financial aid for nonresidents. Since the university can shift its expenditures for the purpose of enrolling additional residents, we believe that it has significant opportunities to replicate this effort.

For example, despite the State’s fiscal crisis, the university increased its spending on employee salaries in eight of the last nine fiscal years. Furthermore, the university pays its top executives salaries that are significantly higher than those the State pays its employees in high-level positions in the executive branch. In fiscal year 2009–10, the university implemented a one-year salary reduction and furlough plan (furlough plan) for faculty and staff, saving an estimated $236 million. If the university had continued this furlough plan at a reduced level, it could have saved an additional $100 million dollars per fiscal year. The university also could improve its executive compensation practices by conducting regular compensation and benefits studies, by addressing recommendations its internal auditor made in 2013 regarding salary-setting practices, and by producing its annual executive compensation report in a timely manner.

Moreover, the university has not maximized the benefits that it could have achieved from an initiative it developed in 2010 called Working Smarter. The Working Smarter initiative’s goal was to redirect the savings generated and the new revenue sources developed to the university’s core academic and research missions. Although the university asserts that it generated $664 million in combined savings and new revenue over the past five years, it could not substantiate this amount or demonstrate that the entire amount was redirected to its academic and research missions. Further, the university does not centrally direct the savings or new revenue the campuses generate or require that campuses participate in the initiative. The university estimates that if it had achieved a campus participation rate of 80 percent for one program alone, it would have generated $9 million of additional savings.

Finally, the university’s nonresident undergraduate recruiting expenditures have increased—from $900,000 in fiscal year 2010–11 to $4.5 million in 2014–15. If the university had done more to limit its nonresident recruiting expenditures, this would have resulted in additional savings from fiscal years 2010–11 through 2014–15.

During the State’s Fiscal Crisis, the University Significantly Increased Its Spending on Employee Costs

As we discuss in the Introduction, the State’s 2008 fiscal crisis resulted in a series of significant cuts to the university’s state appropriations. We expected that the university would have reviewed the efficiency of its internal operations and expenditures in response to these cuts to ensure its ability to continue to provide residents with a high‑quality, low-cost education. Instead, the university increased its staff who belong to one or more of the personnel programs described in Table 11, and it increased spending on salaries in eight of the last nine fiscal years. Additionally, during the past 10 fiscal years, the university increased mandatory fees for residents—base tuition and the student services fee—six times, and increased total nonresident enrollment by 118 percent.

From fiscal year 2005–06 to 2014–15, the gross earnings of the university’s employees systemwide increased 64 percent, from nearly $8 billion a year to nearly $13 billion a year. During that time, the number of university employees and gross earnings increased within each personnel program except the senior management group, as depicted in Table 11. Although the senior management group experienced a reduction of 133 employees, or 40 percent, its gross earnings only decreased by 4 percent during the 10 years, indicating that the average gross earnings of employees in this group also increased. Further, the reduction in the number of employees occurred not because the university reduced the number of senior managers, rather because it reclassified and transferred approximately 100 deans from the senior management group program into the academic personnel program. The managers and senior professionals personnel program experienced the largest increase in employees at 51 percent, or an increase of 4,408 employees, accompanied by a more than $765 million increase in gross earnings, or 104 percent.

Sources: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Corporate Data Warehouse and Decision Support System. The summaries contain payroll transactions, reported as of September 30, 2015.

Note: This table includes all of the university’s staff at each campus, the Office of the President, and medical centers. Dollars are rounded to the nearest hundred thousand.

* Employee counts are based on employees rather than positions, which includes both full- and part-time employees. Also, an employee may be counted more than once if the employee moved from one personnel program to another during the year or held more than one position concurrently.

† The reduction in the number of senior management group employees occurred because the university reclassified and transferred approximately 100 deans from the senior management group into the academic personnel program.

‡ Total exceeds 100 percent due to rounding.

The only fiscal year in which the university decreased its spending on employee salaries was in fiscal year 2009–10, when it implemented a furlough plan for faculty and staff from September 2009 to August 2010. The university estimated that this plan, in which it furloughed employees for 10 to 26 days during those 11 months, saved $236 million from all funding sources. However, in the following year, it negated this one-time cost savings from the furlough plan when it increased its spending on employee salaries by $526 million. Had it continued its furlough plan, the university could have achieved additional savings to offset its loss of state funding. For example, had it continued the furlough program at even less than half the fiscal year 2009–10 savings rate, it could have saved an additional $100 million per fiscal year. Instead, the university’s expenditures for employee salaries continued to increase in each of the fiscal years after the furlough plan ended, for a total of $3.1 billion. In a 2015 analysis of its employee costs, the university attributed 60 percent of its growth in employees from 2007 to 2014 to health science employees, who are paid from other funds besides the State’s General Fund and tuition and fees. It attributed the remaining 40 percent in employee growth to the campuses and the Office of the President, split about evenly between university staff and student workers. However, the university’s analysis does not address the increased cost associated with its employment growth. Although the university indicated that it reduced the number of employees it paid from state funds, the university also increased the number of employees it paid from other funds such as tuition and fees, indicating that the fund sources with which it uses to pay its employees changed.

The University Provides Salaries and Benefits That Significantly Exceed the Compensation of Other High-Level State Positions

In addition to increasing its total number of staff and their gross earnings during the State’s fiscal crisis, the university also paid salaries to its executives that significantly exceeded the amounts earned by employees in high-level state executive branch positions. As shown in Table 12, the salaries of the university’s top executives—including the president, four officers of the Regents of the University of California (regents), and the 10 campus chancellors—significantly exceeded those of employees in high‑level executive branch positions. The university paid all but one of its executives in these positions a base salary of at least $400,000 in fiscal year 2014–15, which was more than double the amount the executive branch paid the governor and the directors of several large state departments. Additionally, all university positions exceeded the salary level of the executive branch’s highest career executive assignment (CEA). CEAs at this level include directors of small departments, chief deputy directors of large departments, or positions with specialized skills within the executive branch. Effective June 2015, state law requires the university to revise its existing process for establishing the salary ranges for its top executives, specifically those in the senior management group, so that its process includes, at a minimum, comparable positions in state government.

| Entity | Position | Fiscal Year 2014–15 Base Salary Earned* |

|---|---|---|

| University of California | Chief Investment Officer and Vice President of Investments† | $615,000 |

| University of California | Chancellor, San Francisco | 579,825 |

| University of California | President | 570,000 |

| University of California | General Counsel and Vice President for Legal Affairs† | 428,480 |

| University of California | Senior Vice President - Chief Compliance and Audit Officer† | 417,150 |

| California State Teachers’ Retirement System | Chief Investment Officer | 415,377 |

| California Public Employees’ Retirement System | Chief Investment Officer | 406,785 |

| University of California | Chancellors, average of remaining nine campuses‡ | 404,313 |

| California Department of Corrections and Rehabilitation | Agency Secretary | 233,611 |

| California Department of Public Health | Director | 225,078 |

| University of California | Secretary and Chief of Staff to the Regents† | 225,000 |

| California State Teachers’ Retirement System | General Counsel | 224,196 |

| California Department of Finance | Director | 178,111 |

| Top allowable executive branch career executive assignment (CEA) salary for positions requiring licensure as a physician, attorney, or engineer | ||

| State of California | Governor | 169,559 |

| California Department of Water Resources | Director | 168,890 |

| California Department of Education | Superintendent of Public Instruction | 152,998 |

| California Department of General Services | Director | 150,277 |

| California Department of Consumer Affairs | Director | 136,496 |

| Top allowable CEA Level C salary | ||

| California State Controller’s Office | Controller | 134,325 |

Sources: California State Auditor’s analysis of data obtained from the University of California (university) Office of the President’s Corporate Data Warehouse and Decision Support System. The data contain payroll transactions reported as of September 30, 2015. State employee data are from the California State Controller’s Office website.

Note: All university positions listed in the table had additional cash earnings during fiscal year 2014–15, which were excluded from the table. The base salary for the chancellor of the San Francisco campus excludes amounts paid by endowment funding.

* State employee salaries were for 2014, with the exception of the Director of the California Department of General Services and the General Counsel of the California State Teachers’ Retirement System, whose salaries are from 2013.

† The university refers to these four positions as its principal officers of the Regents of the University of California.

‡ Excluding the San Francisco campus, the salaries of the chancellors of the other nine campuses ranged from $369,000 to $501,000. The chancellor for the Irvine campus served in his position for part of the fiscal year.

We reviewed the university’s progress toward this state requirement and found that as of February 2016 it matched 32 of its 92 total senior management group positions to positions existing within state government, the California State University, and local governments. The university indicates it was unable to identify comparable positions for the remaining 60 positions because it either found no comparable positions at these entities or needed more time to assess the comparability of the positions. Of the 32 comparable positions it found, the university only matched 23 to positions in state government. The university intends to present this analysis to the regents in March 2016 for approval. If approved, 60 of the university’s salary ranges for its senior management positions will not include comparable positions from the State, local governments, or California State University. As such, the university’s analysis is limited and more work is needed to identify additional positions at these entities for inclusion in its salary ranges.

In addition to salaries that exceed those of employees in high-level executive branch positions, the university provides certain generous benefits to its president and chancellors. Specifically, the university makes contributions to the retirement savings plans of senior management group employees with full-time, nontenured academic appointments at the rate of 3 to 5 percent of their monthly base salaries. For instance, the president of the university earned a base salary of $570,000 in fiscal year 2014–15. Because she receives the retirement plan benefit at 5 percent, the university contributed $28,500 that year to her elected retirement savings plan. This retirement benefit is in addition to the university’s regular pension plan, to which it contributes 14 percent and employees contribute 8 percent of their gross pay.

Additionally, while the salaries of the university’s top executives ranked below those at similar research institutions, the comparative data did not include all elements of compensation for the participating university executives. Specifically, using The Chronicle of Higher Education’s annual survey of chief executive compensation at public and private universities (Chronicle survey), we found that the salaries of the university’s president and chancellors in fiscal year 2013–14 ranked in the bottom half when compared to similar positions at peer research institutions.6 These peer institutions are members of the Association of American Universities, an organization composed of 62 leading public and private research universities located throughout the United States and Canada. According to the Chronicle survey and our additional analysis of the university’s payroll data, the salaries of the university’s chancellors fell among the lower third of its public and private peer institutions in fiscal year 2013–14, while the president of the university ranked above the middle, placing 10th out of 28 public universities that participated in the survey. The university reported that all but one of its chancellors’ annualized base salaries for 2014 had increased by $12,000 to $93,000, while the president’s base salary remained unchanged.7

Examples of Benefits the University Commonly Offers Its President and Chancellors

- Monthly contribution ranging from 3 to 5 percent of the employee’s base salary to one of three types of retirement savings plans, only if the employee does not have an underlying faculty appointment.

- Accrual of sabbatical leave credit if the employee has an underlying faculty appointment.

- Executive life insurance up to two times the employee’s annual base salary to a maximum of $800,000.

- University-provided housing.

- Monthly cash automobile allowance for university business use of a privately-owned vehicle.

- Eligibility for a low-interest home loan upon leaving the position if the employee assumes a tenured position at a university campus.

- Relocation of personal belongings to a California location of the employee’s choice when the employee leaves the position if the employee continues employment at the university.

Sources: California State Auditor’s analysis of compensation packages and University of California compensation policy.

Although the salaries of the university president and chancellors generally lagged behind those paid by comparable public universities, the Chronicle survey did not report the total value of the public universities’ compensation packages. Specifically, it excluded benefits and other noncash elements of compensation for executives of public universities, which may or may not be similar to what the university provides. Examples of other benefits are shown in the text box.

The University Needs to Take Additional Steps to Justify Its Salaries and Benefits

The university could do more to justify the salaries and benefits it provides to its employees. Specifically, it has not conducted regular compensation and benefit studies that would enable it to assess the reasonableness of its executive compensation. Further, it has failed to address its own internal recommendations related to improving its executive compensation practices. Finally, it has not produced timely reports that would increase transparency regarding the salaries and benefits it offers to its top executives and senior managers.

The university has not been proactive in assessing the total value of benefits it provides to its top executives and managers. In 2009, a university consultant performed an analysis to value the competitiveness of certain elements of the university’s executive compensation packages by comparing its base salaries, health and welfare benefits (health benefits), and retirement with those offered by 26 public and private universities, 12 national academic medical centers, and 10 California medical providers. The consultant found the base salaries of employees in its senior management program and its managers and senior professionals program lagged behind the market by 22 and 16 percent, respectively. However, when the consultant added the total value of the university’s health benefits and retirement, the compensation disparity was reduced to approximately 14 percent below market for the senior management group and 4 percent below market for managers and senior professionals.