Introduction

Background

State Bar of California’s Primary Responsibilities

- Regulating the conduct of attorneys through an attorney discipline system

- Administering the exam for admission to the California State Bar

- Regulating mandatory continuing legal education

- Administering an Attorney Diversion and Assistance Program

- Expanding access to and improving the quality of free or low cost legal services in civil matters for indigent citizens

- Administering a Client Security Fund to mitigate losses caused by the dishonest conduct of attorneys

Source: Business and Professions Code, Division 3, Chapter 4.

The State Bar of California (State Bar) is a public corporation within the judicial branch of the State of California. State law requires that every person admitted and licensed to practice law in California belong to the State Bar, unless the individual holds office as a judge in a court of record. State law establishes public protection as the highest priority of the State Bar and its board of trustees (board) in exercising their licensing, regulatory, and disciplinary functions. The State Bar’s primary responsibilities are listed in the text box.

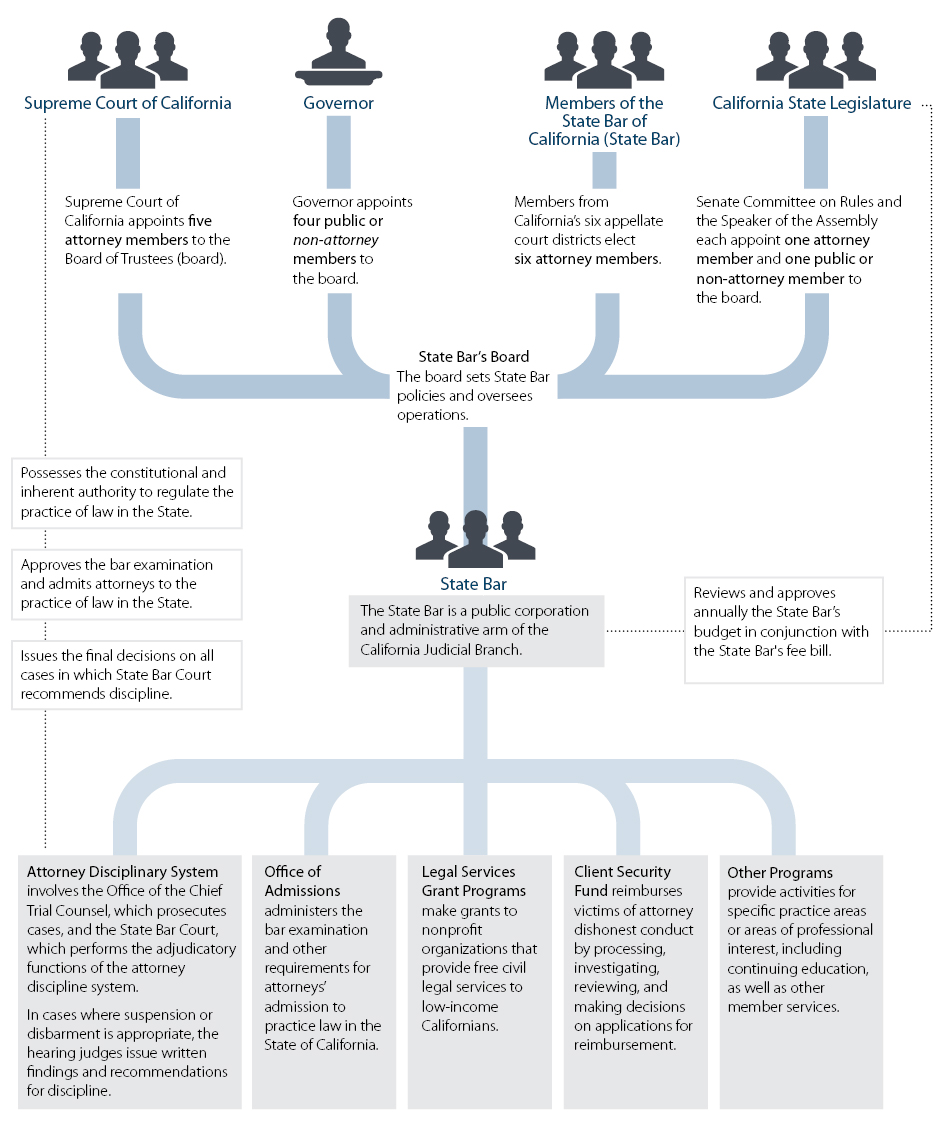

The State Bar’s Governance and Oversight Structure

States may use one of two models to establish their bars: the unified bar model or the voluntary bar model. Characteristics of a unified bar model, which California’s bar follows, include mandatory membership and the payment of an annual fee by each attorney licensed to practice law in the State.1 The bar’s functions under this model include discipline, admissions, and education. A unified bar also provides member services, such as annual meetings and social functions; political lobbying related to the administration of justice; and member discounts on insurance and other goods and services. Like California, Texas and Florida operate under the unified bar structure.

Under the voluntary bar model, a state supreme court creates boards, commissions, or agencies that are responsible for overseeing the state’s legal disciplinary systems; thus, the state bar performs only member‑service functions. States that operate under the voluntary bar structure include New York and Illinois. Boards govern the bars in both unified and voluntary models. However, the voluntary bars in New York and Illinois also have assemblies—large authoritative bodies—that set the policies that the boards administer.

Typically a 19‑member board that meets formally six to eight times per year governs the State Bar. As Figure 1 shows, 13 of its trustees are lawyers: members of the State Bar elect six of these 13, and the California Supreme Court (Supreme Court) and the Legislature appoint the other seven. Six members are public members who are not attorneys: the governor appoints four, and the Legislature appoints two members. Each of these six public members is subject to confirmation by the Senate and must never have been a member of the State Bar or admitted to practice in any court in the United States. California’s State Bar board members serve three‑year terms and may be reelected. As of March 2016, the longest‑serving trustee had been on the board since 2009, and another had served since 2010.

The State Bar has experienced significant turnover and a restructuring of its executive management since 2014. All of the state bars we reviewed employ executive directors to execute the policies and directives of their boards. In California, the executive director serves at the pleasure of the board. On November 7, 2014, after procuring an independent investigation of wide‑ranging allegations that several of the State Bar’s high‑level employees had raised, the State Bar’s board voted to end the former executive director’s employment. Additionally, five other executives left the State Bar between November 2014 and November 2015. The former executive director subsequently filed a lawsuit. In January 2016, a Los Angeles County Superior Court judge appointed an arbitrator to assist the State Bar and the former executive director in resolving the litigation. The arbitrator dismissed all claims in the lawsuit in April 2016. According to a State Bar press release, should the former executive director amend his complaint, the State Bar will again challenge it.

The State Bar hired a new executive director and a new chief operations officer (operations officer), who assumed their responsibilities in September 2015, and a new general counsel, who began her employment in October 2015. Under the new leadership, the State Bar restructured its executive management team by eliminating the positions of deputy executive director, chief financial officer, and chief communications officer, among others. As of March 2016, the State Bar employed 534 people, and it had offices in San Francisco and Los Angeles.

Figure 1

The State Bar of California’s Governance Structure

Sources: Various Business and Professions Code sections and State Bar organization charts and documents.

The State Bar’s Accounting Processes for Revenue and Expenses In 2015 the State Bar accounted for its various revenue and expenses by recording individual transactions across 22 program funds and its general fund. As shown in Table 1, these funds are designed for specific purposes, such as accounting for mandatory fee revenue and expenses related to administering the bar exam or for voluntary donations to provide grants to nonprofit legal aid organizations. Some of the State Bar’s funds are restricted; therefore, the money within those funds can only be used in accordance with special regulations, restrictions, or limitations. In 2015 the State Bar consolidated eight of its funds into its general fund for financial reporting and budgeting purposes. However, the State Bar still tracks revenue and expenses of these eight funds separately in its accounting system.

| Consolidated Gerneral Fund* | Main operating fund | General Fund–Used to account for membership fees and resources of the State Bar of California (State Bar) not related to other fund activities; these fees include those assessed on law corporations and continuing education providers. Also used to account for voluntary and nonfee operating revenue of the State Bar not related to other fund activities, including revenue from continuing education fees and investment income. The general fund supports various State Bar programs, including Discipline and Adjudication, Administration of the Profession, and Program Development. |

| Capital asset funds | Building Fund–Used to account for revenue from rental income the State Bar generates from leasing space to third parties at its facility in San Francisco. The Building Fund also accounts for capital asset purchases, including construction, equipment, furnishings, land, and buildings not accounted for in the Fixed Assets Fund or in the Los Angeles Facilities Fund. | |

| Fixed Assets Fund–Used to account for capital assets not accounted for in the Building Fund and in the Los Angeles Facilities Fund. This fund does not receive revenue. | ||

| Los Angeles Facilities Fund–Used to account for rental income the State Bar generates from leasing space to third parties at its facility in Los Angeles. This Fund also accounts for all expenses, such as capital asset purchases, loan payments, and building maintenance activities related to the State Bar’s Los Angeles facility. | ||

| Reserve funds | Benefits Reserve Fund–Used to account for resources set aside by the State Bar to fund the future costs of postemployment benefits other than pensions. Resources in this fund are provided by other State Bar funds in proportion to their salary expenses. | |

| Public Protection Fund–Used to account for reserve funding set aside to ensure the continuity of the State Bar’s disciplinary system and its other essential public protection programs. | ||

| Other program and administrative funds | Legal and Education Development Fund–Used to account for revenue from royalties, marketing contributions, investment income, and programs it offers to members, such as life insurance and discounts on products. The Legal and Education Development Fund supports competency‑based education programs for attorneys that are aimed at reducing the severity and frequency of professional liability claims. | |

| Technology Improvement Fund–Used to account for expenses related to technology projects. This fund receives resources from the State Bar’s other funds—such as the Information Technology Assessment Fund, the Admissions Fund, and the general fund—to finance its technology projects. | ||

| Support and Administration Fund–Used to account for the State Bar’s indirect costs that are not accounted for by the program areas in the State Bar’s other funds. The Support and Administration Fund does not receive revenue. | ||

| Restricted funds | Admissions Fund–Used to account for mandatory fee revenue and expenses related to administering the bar examination and other requirements for admission to the practice of law in the State of California. This fund is also used to account for voluntary and nonfee operating revenue of the State Bar not related to other fund activities, including penalties and various continuing legal education fees. | |

| Client Security Fund–Used to account for mandatory membership fees and expenses of the Client Security Fund program. The State Bar is required by law to administer the Client Security Fund program to reimburse individuals who incur losses resulting from dishonest conduct by attorneys. | ||

| Elimination of Bias and Bar Relations Fund–Used to account for annual voluntary membership fees and expenses that support activities with voluntary bar associations and programs that address concerns of access and bias in the legal profession. The State Bar includes a voluntary fee in its annual membership fee bill; however, members who do not wish to fund these activities have the option to reduce their annual fee payment by $5. This fund is also used to account for various voluntary fees related to the State Bar’s sponsored events and programs, as well as grant revenue. | ||

| Equal Access Fund–Used to account for funding from the Judicial Council of California that the State Bar uses to provide grants to approximately 100 nonprofit legal aid organizations to provide free legal services to indigent Californians. | ||

| Information Technology Special Assessment Fund–Used to account for a $10 mandatory fee the State Bar collected from its members from 2011 through 2013 for the purpose of upgrading the State Bar’s information technology systems, including the purchase and maintenance of computer hardware and software. | ||

| Justice Gap Fund–Used to account for voluntary donations the State Bar uses to provide grants to nonprofit legal aid organizations offering free legal services to low‑income Californians. The State Bar includes an option on its annual membership fee bill for members to make donations to this program. | ||

| Lawyer’s Assistance Fund–Used to account for mandatory member fees the State Bar uses to fund education, remedial, and rehabilitative programs for those members who need assistance as a result of disabilities related to substance abuse or mental illness. | ||

| Legal Services Trust Fund–Used to account for revenue primarily from interest earned on certain client trust accounts held by California attorneys to fund free legal services for indigent people. State law requires attorneys who hold client funds in trust to remit interest earned on those accounts to the State Bar. After the State Bar deducts its administrative costs, it distributes the remaining funds as grants to nonprofit legal aid organizations. In addition, this fund receives voluntary membership fees that the State Bar also uses to fund these grants. The State Bar includes a voluntary fee for this fund in its annual membership fee bill; however, members who do not wish to fund these activities have the option to reduce their annual fee payment by $40. This fund is also used to account for tax refund revenue intercepted from resigned or disbarred members who have outstanding debts with the State Bar. | ||

| Legal Specialization Fund–Used to account for voluntary application fees, certification fees, recertification fees, and annual membership fees and expenses of the State Bar’s Legal Specialization Program. | ||

| Legislative Activities Fund–Used to account for voluntary member fees the State Bar uses for lobbying and other related activities deemed outside of the parameters established in Keller vs. the State Bar. The State Bar includes a voluntary fee for this fund in its annual membership fee bill; however, members who do not wish to fund these activities have the option to reduce their annual fee payment by $5. | ||

| Sections Fund–Used to account for voluntary membership fees and expenses restricted by law related to the activities of 16 sections, which consist of specific practice areas or areas of professional interest. The Sections Fund also receives revenue from seminars and workshops, advertising, sales of various pamphlets and publications, and grants. | ||

| Other funds | Annual Meeting Fund–Used to account for voluntary registration fees and expenses of the State Bar’s annual meeting. The Annual Meeting Fund allocates its revenue and expenses among itself, the Sections Fund, and the Conference of Delegates of California Bar Associations, which operates as an independent entity. This fund is also used to account for advertising revenue and other miscellaneous revenue generated from hosting the annual meeting. | |

| Grants Fund–Used to account for corporate sponsorships and grant revenue the State Bar uses to support various program expenses and special projects. | ||

| State Bar Access and Education Foundation Fund–Used to account for the activities of the State Bar’s nonprofit organization, the State Bar Access and Education Foundation. |

Sources: The State Bar’s 2014 financial report and accounting documents, policies of the State Bar’s board of trustees, and the California Business and Professions Code.

* The funds in the consolidated general fund are reported as one fund in the State Bar’s financial statements beginning in fiscal year 2015; however, the State Bar continues to report restricted funds and other funds separately.

The State Bar’s budget serves as its primary fiscal control and contains its anticipated income and expenses. The State Bar uses its budget to present its plans for its programs, the cost of those plans, and the estimated income sources it intends to use to finance the costs. The State Bar’s Office of Finance prepares and submits the annual budget to the board for approval. State law requires the board to complete and implement five‑year strategic plans, which provide the framework for its annual budget process. In its most recent update of its strategic plan in 2014, the State Bar included such initiatives as modernizing its information technology, improving its physical facilities, and streamlining its programs and processes.

The State Bar’s fiscal year ends on December 31, and its expense cycle begins when the board uses the annual budget process to approve expense amounts for its programs. State Bar policy requires various levels of management approval to authorize all expenses based on board‑approved budget or agenda items. For example, certain employees may approve amounts up to $1,000, managers may approve amounts up to $5,000, and senior executive staff members may approve amounts up to $50,000. Only the State Bar’s executive director or operations officer may approve amounts more than $50,000. State Bar policy further emphasizes that each department’s procurement of goods and services must be based on its approved budget regardless of the amount of the purchase.

The State Bar also has formal processes in place to ensure that its staff record revenue and expenses in the appropriate funds and accounts. For example, its policies and procedures for cash receipts describe the steps necessary to prepare, review, and approve transactions and to record them in its accounting system.

The State Bar’s Revenue Sources

The State Bar maintains, operates, and supports its discipline system and general operations primarily through mandatory fees that it charges its members. Nearly 49 percent of the revenue the State Bar received from 2013 through 2015 was restricted either by statute or by its board. As shown in Table 2, the State Bar’s largest types of revenue were mandatory member fees, admissions fees, and revenue from the Judicial Council of California (Judicial Council) used for grants. In 2015 mandatory member and admissions fees totaled $91.7 million, or 61 percent of the State Bar’s overall revenue. Judicial Council revenue totaled about $14.2 million, or 9 percent of its overall revenue.

| 2013 | 2014 | 2015 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Revenue Type | Restricted | Unrestricted | Total | Restricted | Unrestricted | Total | Restricted | Unrestricted | Total | |

| Category 1: Mandatory fees and other charges | ||||||||||

| Mandatory member fees | $11,357 | $59,236 | $70,593 | $7,597 | $64,811 | $72,408 | $7,709 | $65,784 | $73,493 | |

| Admissions fees | 17,939 | 17,939 | 17,487 | 17,487 | 18,253 | 18,253 | ||||

| Legal specialization fees | 2,388 | 2,388 | 2,019 | 2,019 | 2,538 | 2,538 | ||||

| Law corporation fees | 1,338 | 1,338 | 1,355 | 1,355 | 1,410 | 1,410 | ||||

| Continuing education fees | 293 | 136 | 429 | 311 | 137 | 448 | 280 | 156 | 436 | |

| Law school fees | 139 | 139 | 126 | 126 | 125 | 125 | ||||

| Other mandatory charges | 173 | 723 | 896 | 194 | 848 | 1,042 | 227 | 869 | 1,096 | |

| Category 1 total | 32,289 | 61,433 | 93,722 | 27,734 | 67,151 | 94,885 | 29,132 | 68,219 | 97,351 | |

| Category 2: Voluntary fees and charges, and donations | ||||||||||

| Donations | 5,893 | 5,893 | 7,395 | 7,395 | 8,912 | 8,912 | ||||

| Sections fees | 4,951 | 4,951 | 5,428 | 5,428 | 5,891 | 5,891 | ||||

| Continuing education fees | 1,025 | 226 | 1,251 | 1,029 | 170 | 1,199 | 810 | 278 | 1,088 | |

| Other voluntary fees and charges | 3,216 | 628 | 3,844 | 3,388 | 795 | 4,183 | 3,653 | 682 | 4,335 | |

| Category 2 total | 15,085 | 854 | 15,939 | 17,240 | 965 | 18,205 | 19,266 | 960 | 20,226 | |

| Category 3: Nonfee operating revenue | ||||||||||

| Judicial Council of California revenue | 16,145 | 23 | 16,168 | 14,512 | 5 | 14,517 | 14,200 | 25 | 14,225 | |

| Settlement grants | 6,085 | 6,085 | ||||||||

| Mandatory collection of interest on lawyer trust accounts | 4,989 | 4,989 | 5,226 | 5,226 | 5,532 | 5,532 | ||||

| Penalties, late fees, and miscellaneous charges | 509 | 2,562 | 3,071 | 460 | 2,374 | 2,834 | 476 | 2,530 | 3,006 | |

| Insurance program revenue | 1,867 | 1,867 | 1,650 | 1,650 | 2,143 | 2,143 | ||||

| Advertising income | 17 | 126 | 143 | 35 | 140 | 175 | 57 | 159 | 216 | |

| Royalties and sales of member information | 136 | 136 | 115 | 115 | 188 | 188 | ||||

| Collections from tax intercepts | 178 | 178 | 99 | 99 | ||||||

| Sales of publications | 77 | 38 | 115 | 65 | 45 | 110 | 57 | 24 | 81 | |

| Other revenue | 4 | 4 | 4 | 4 | 4 | 4 | ||||

| Category 3 total | 21,737 | 4,756 | 26,493 | 20,476 | 4,333 | 24,809 | 26,506 | 5,073 | 31,579 | |

| Category 4: Other nonoperating revenue | ||||||||||

| Rental income | 1,034 | 1,034 | 1,879 | 1,879 | 1,814 | 1,814 | ||||

| Investment income | 134 | 128 | 262 | 102 | 127 | 229 | 109 | 76 | 185 | |

| Category 4 total | 134 | 1,162 | 1,296 | 102 | 2,006 | 2,108 | 109 | 1,890 | 1,999 | |

| Grand total | $69,245 | $68,205 | $137,450 | $65,552 | $74,455 | $140,007 | $75,013 | $76,142 | $151,155 | |

Source: California State Auditor’s analysis of the State Bar of California’s JD Edwards EnterpriseOne data.

Member Fees, Admissions Fees, and Donations

In recent years, the State Bar’s mandatory member fees revenue ranged from $70.6 million in 2013 to $73.5 million in 2015 because of a 4.3 percent increase in membership. Historically, annual legislation has authorized the State Bar to impose a membership fee; however, in 1997 the governor vetoed the annual fee bill because he had concerns that the State Bar had become overly political, unresponsive to its members, and inefficient. As a result, the State Bar was unable to impose annual membership fees for 1998 and 1999. The Supreme Court adopted an emergency interim measure in 1998 and imposed a mandatory fee on all active members for a special attorney discipline fund.

In past years, state law also authorized the State Bar to charge members additional mandatory fees for specific purposes. For example, from 2008 through 2013, state law authorized the State Bar to collect an additional $10 from each active member to pay for upgrades to its information technology (IT) systems. State law also authorized the State Bar to collect an additional $10 from each member from 2009 through 2013 to pay for the cost of financing, constructing, purchasing, or leasing facilities to house State Bar staff in Southern California. Additionally, admission fees support the State Bar’s admission program. State law requires applicants to pay these fees if they wish to take the bar exam and register to practice law in the State. The State Bar received between $17.5 and $18.3 million annually in admissions fees from 2013 to 2015.

On the other hand, some of the membership fees the State Bar collects are voluntary. For example, members may choose not to pay the State Bar’s $5 fee for lobbying and related activities. As shown in Table 3, State Bar members each could pay a maximum of $50 in voluntary membership fees for 2015 and 2016. State law restricted to specific purposes the State Bar’s use of $45 of each $50 voluntary fee payment, while the board restricted the other $5. For example, members can pay a voluntary $40 fee to the Legal Services Trust Fund, which specifically supports nonprofit organizations that provide free legal services to people of limited means. The State Bar collected more than $20.2 million in total voluntary fees, donations, and charges in 2015. Of this amount, the State Bar received nearly $5.9 million in voluntary sections fees—revenue dedicated to voluntary organizations of attorneys and associates who share an area of interest. The Sections help their members maintain knowledge in various fields of law, expand their professional contacts, and serve the profession, the public, and the legal system. The State Bar received the remaining $14.3 million of the $20.2 million in donations and other voluntary fees and charges to provide legal aid to low‑income Californians, to address concerns of bias in the legal profession, to offer support services for local bar associations, and to oversee providers of continuing education.

| 2013 | 2014 | 2015 | 2016 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Fee allocation by fund | Active Member Fee | Inactive Member Fee | Active Member Fee | Inactive Member Fee | Active Member Fee | Inactive Member Fee | Active Member Fee | Inactive Member Fee | |

| Funds receiving mandatory fees | |||||||||

| General Fund | $285 | $ 45 | $305 | $65 | $305 | $ 65 | $305 | $65 | |

| Client Security Fund | 40 | 10 | 40 | 10 | 40 | 10 | 40 | 10 | |

| General Fund—discipline activity | 25 | 25 | 25 | 25 | 25 | 25 | 25 | 25 | |

| Lawyers Assistance Fund | 10 | 5 | 10 | 5 | 10 | 5 | 10 | 5 | |

| Building Special Assessment Fund | 10 | 10 | – | – | – | – | – | – | |

| Information Technology Special Assessment Fund | 10 | – | – | – | – | – | – | – | |

| Funds receiving voluntary fees | |||||||||

| Legal Services Trust Fund | 20 | 20 | 30 | 30 | 40 | 40 | 40 | 40 | |

| Legislative Activities Fund | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| Elimination of Bias and Bar Relations Fund | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

Sources: California State Auditor’s review of California Business and Professions Code and of State Bar of California documents.

Revenue for Grants

The Judicial Council contracts with the State Bar to administer grants through its Equal Access Fund. In 2015 the Equal Access Fund received more than $14.4 million in revenue for the State Bar to award to qualified legal services projects and support centers that provide legal services to indigent people. The State Bar also receives interest on lawyer trust accounts for the same purpose. Further, the State Bar received $6 million from a national mortgage settlement in 2015 to provide grants for organizations helping California families dealing with foreclosures and community redevelopment legal assistance. The State Bar’s Legal Services Trust Fund Commission awards these grants.

Other Revenue

From 2013 to 2015, the State Bar collected between $6.6 and $7.7 million annually from other sources, including insurance program revenue, rental income, and penalties and late fees. Insurance program revenue accounted for $2.1 million in 2015. Although revenue from these sources is not legally restricted, the board may set it aside during its annual budget process for specific purposes or programs. For example, the board designated insurance program revenue to provide financial support for legal service programs in 2015. The State Bar also deposited its 2015 rental income of $1.8 million—proceeds from leasing to other organizations the unused space in its San Francisco and Los Angeles facilities—into its general fund to support facility‑related expenses, such as construction, equipment, and furnishings.2

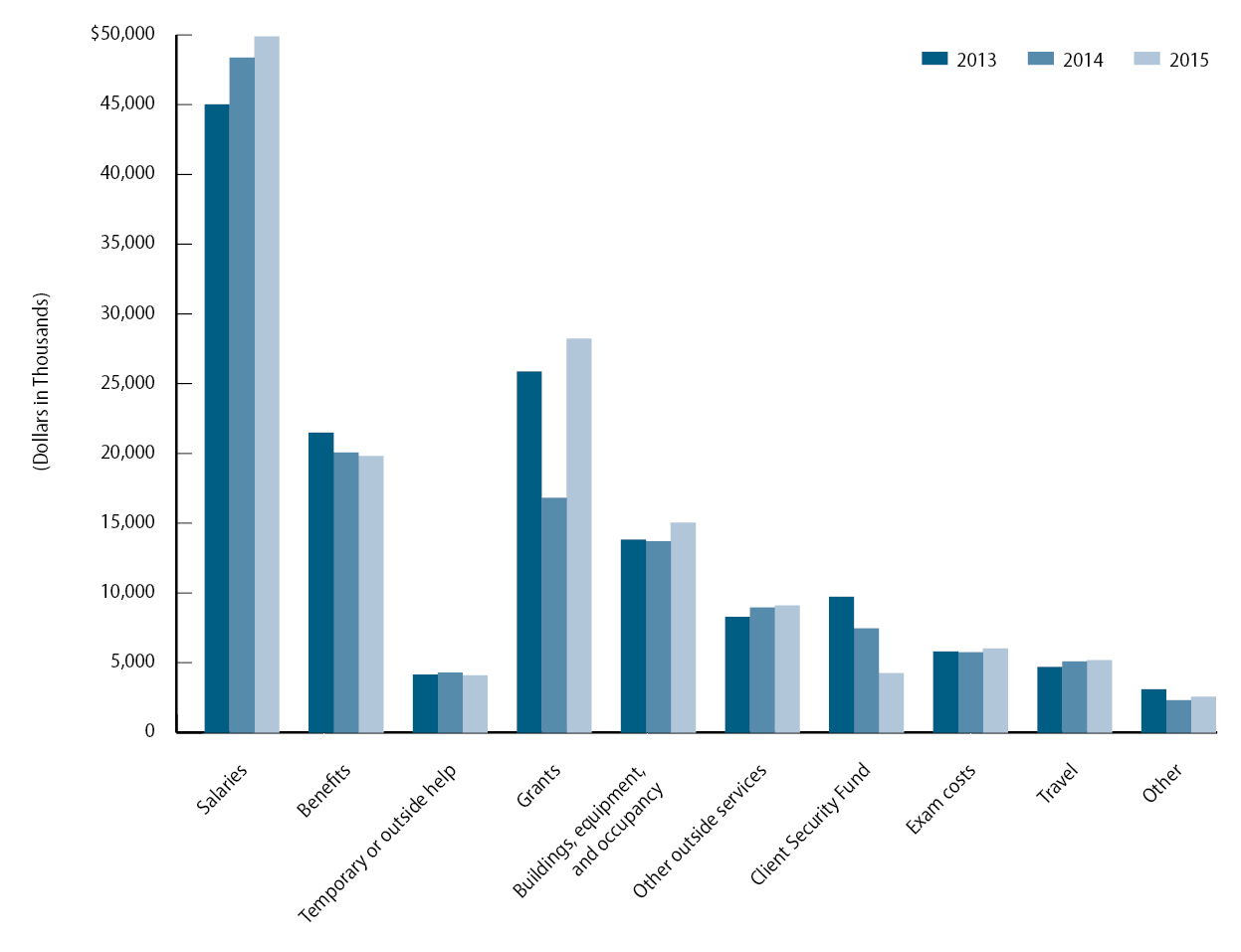

The State Bar’s Expenses

The State Bar’s largest expenses included salaries, benefits, and grants. As shown in Figure 2, salaries accounted for the State Bar’s largest expense and increased by nearly $4.9 million between 2013 and 2015. Grants, like those previously mentioned for legal services for indigent people, accounted for the State Bar’s next largest expense. The State Bar reported a decrease in its grant expenses in 2014 because it adjusted its grants cycle to coincide with the calendar year. As a result, it reported only six months of grant activities in its 2014 financial statements. Finally, as Figure 2 shows, the Client Security Fund’s expenses decreased each year from 2013 through 2015. We discuss this decrease in the Audit Results.

Figure 2

The State Bar of California’s Expenses

From 2013 Through 2015

Source: California State Auditor’s analysis of the State Bar of California’s JD Edwards EnterpriseOne data.

Prior Audit by the California State Auditor

Our June 2015 audit titled State Bar of California: It Has Not Consistently Protected the Public Through Its Attorney Discipline Process and Lacks Accountability, Report 2015‑030, included eight recommendations to the State Bar related to the efficiency and effectiveness of its discipline system and seven recommendations related to improving its financial practices. Specifically, we found that the State Bar’s efforts to align with its mission the staffing for its discipline system had fallen short. In 2011 it employed contractors, shifted staffing resources, and authorized a significant amount of overtime to reduce its backlog of attorney discipline cases, but it discontinued these operational changes shortly thereafter. Its backlog subsequently increased by 25 percent between 2011 and 2014.

State Bar of California’s Workforce Plan

The State Bar of California (State Bar) contracted in 2016 with the National Center for State Courts to review the State Bar’s staffing levels and make recommendations for improving the efficiency and effectiveness of its programs and business processes. The contract requires the following:

- Identify the desired performance level.

- Identify current staffing, including temporary or contract staffing.

- Make recommendations for business process reengineering that could increase the efficiency of each department reviewed.

- Develop a workforce plan that identifies performance‑level metrics and objectives, recommended business processes, and recommended staffing levels, including staff type.

- Develop an implementation timeline and approach.

- Prepare a written report of its recommendations, including the methods, techniques, and data it used to develop its proposed performance metrics, workload planning, and business process reengineering.

Source: The State Bar’s contract with National Center for State Courts, February 2016.

To better align its staffing with its mission, we recommended that the State Bar engage in workforce planning for its discipline system. In October 2015, the governor signed Senate Bill 387 (SB 387), which—among other things—requires the State Bar to submit a workforce plan to the Legislature by May 15, 2016, and to implement this plan by December 31, 2016. In response, the State Bar contracted with the National Center for State Courts, a nonprofit organization, to complete the workforce plan by April 29, 2016. The text box shows the tasks named in the contract. State law requires the State Bar to set a goal for its disciplinary system to complete complaint processing within six months from the receipt of complaints and to ensure that it provides appropriate resources to its disciplinary functions. The State Bar expects the workforce plan will result in a reallocation of resources to the discipline system.

We also recommended that the State Bar conduct an analysis of its operating costs and develop a biennial spending plan that includes an analysis of its plans to spend excessive fund balances. SB 387 also requires that the State Bar conduct a thorough analysis of its operating costs and develop a spending plan to determine a reasonable amount for the annual membership fee by May 15, 2016. The State Bar’s operations officer said that the State Bar anticipates finalizing its analysis of its priorities and necessary operating costs by the statutory deadline.

Additionally, SB 387 requires that the State Bar conduct a public sector compensation and benefits study (compensation study) to reassess the numbers and classifications of staff required to conduct its disciplinary activities. We discuss the compensation study in the Audit Results.

Our June 2015 audit also found that in 2012 the State Bar transferred $12 million among its various funds to facilitate the purchase of a building in Los Angeles, despite the fact that its board had restricted some of this money for other purposes. We recommended that the State Bar implement policies and procedures to restrict its ability to transfer money between funds that its board or state law designated for specific purposes. We also recommended that the State Bar implement a policy requiring it to develop and present to its board accurate cost‑benefit analyses for purchases exceeding a certain dollar level. We advised that these cost‑benefit analyses should compare relevant cost estimates and be clear about the sources of funding the State Bar intends to use to pay for the purchases. In response to our recommendation, the State Bar developed related policies in July 2015.

Scope and Methodology

The Business and Professions Code requires the State Bar to contract with the California State Auditor to conduct an in‑depth financial audit of the State Bar, including an audit of its financial statements, internal controls, and relevant management practices. The law requires the audit to examine the revenue, expenses, and reserves of the State Bar, including all fund transfers. We list the objectives we developed and the methods we used to address them in Table 4.

| Audit Objective | Method | |

|---|---|---|

| 1 | Identify rules and regulations significant to the audit objectives. |

|

| 2 | Assess the State Bar’s financial condition for a selection of its funds as well as its plans to establish reasonable reserves. |

|

| 3 | Determine and evaluate how the State Bar records its revenues to ensure proper use and reporting. |

|

| 4 | Determine whether the State Bar’s interfund transfers are appropriate and consistent with legal restrictions on funds and consistent with generally accepted accounting principles. |

|

| 5 | Determine whether the State Bar’s expenses are appropriate, reasonable, and correctly assigned to programs and funds. |

|

| 6 | Determine the effectiveness of the State Bar’s efforts to recover disciplinary costs and Client Security Fund payments to victims by evaluating the effectiveness of the State Bar’s corrective actions related to recommendations the State Auditor made in previous audits. |

|

| 7 | Determine whether the State Bar’s current compensation levels for its executive management are commensurate with the duties and responsibilities of comparable entities. |

|

| 8 | Determine whether the State Bar’s current governance structure and board composition promote sound operational and financial practices. Identify the board’s oversight of the State Bar’s financial and administrative operations. |

|

| 9 | Determine the appropriateness of the formation and use of the State Bar’s Access and Education Fund and the extent of the Board of Trustees’ oversight. |

|

Sources: California State Auditor’s analysis of state law, planning documents, and information and documentation identified in the table column titled Method.

Assessment of Data Reliability

In performing this audit, we obtained electronic data files extracted from the information system listed in Table 5. The U.S. Government Accountability Office, whose standards we are statutorily required to follow, requires us to assess the sufficiency and appropriateness of computer‑processed information that we use to support our findings, conclusions, or recommendations. Table 5 describes the analyses we conducted using the data from this information system, our methods for testing it, and the result of our assessment.

| Information System | Purpose | Methods and Results | Conclusion |

|---|---|---|---|

| State Bar of California (State Bar) JD Edwards EnterpriseOne (JDE) data Accounting data as of January 26, 2016 |

To make selections of expense, revenue, and transfer transactions from January 1, 2013, through December 31, 2015. To categorize and total expense and revenue transactions from January 1, 2013, through December 31, 2015. |

|

Sufficiently reliable for these audit purposes. |

Sources: California State Auditor’s analysis of various documents, interviews, and data obtained from the State Bar.

Footnotes

1 States that require their practicing attorneys to be members of those states’ bars refer to their bars as unified, integrated, or mandatory. In this report, we refer to this type of bar as unified. Go back to text

2 During 2013 and 2014, the State Bar deposited its rental income into its Building Fund and its Los Angeles Facilities Fund. As previously discussed, the State Bar consolidated these funds into its general fund beginning in 2015. Go back to text