Appendix

THE INVESTIGATIONS PROGRAM

The California Whistleblower Protection Act (Whistleblower Act) authorizes the California State Auditor (state auditor) to investigate allegations of improper governmental activities by state agencies and employees. Contained in the Government Code, beginning with section 8547, the Whistleblower Act defines an improper governmental activity as any action by a state agency or employee during the performance of official duties that violates any state or federal law, is economically wasteful, or involves gross misconduct, incompetence, or inefficiency.

To enable state employees and the public to report suspected improper governmental activities, the state auditor maintains a toll‑free Whistleblower Hotline (hotline) at (800) 952‑5665. The state auditor also accepts reports of improper governmental activities by mail and over the Internet at www.auditor.ca.gov.

The Whistleblower Act provides that the state auditor may independently investigate allegations of improper governmental activities. In addition, the Whistleblower Act specifies that the state auditor may request the assistance of any state entity in conducting an investigation. After a state agency completes its investigation and reports its results to the state auditor, the state auditor’s investigative staff analyzes the agency’s investigative report and supporting evidence and determines whether it agrees with the agency’s conclusions or whether additional work must be done.

Although the state auditor conducts investigations, it does not have enforcement powers. When it substantiates an improper governmental activity, the state auditor confidentially reports the details to the head of the state agency or to the appointing authority responsible for taking corrective action. The Whistleblower Act requires the agency or appointing authority to notify the state auditor of any corrective action taken, including disciplinary action, no later than 60 days after transmittal of the confidential investigative report and monthly thereafter until the corrective action concludes.

The Whistleblower Act authorizes the state auditor to report publicly on substantiated allegations of improper governmental activities as necessary to serve the State’s interests. The state auditor may also report improper governmental activities to other authorities, such as law enforcement agencies, when appropriate.

Improper Governmental Activities Identified by the State Auditor

Since the state auditor activated the hotline in 1993, it has identified improper governmental activities totaling $575.8 million. These improper activities include theft of state property, conflicts of interest, and personal use of state resources. For example, the state auditor reported in March 2014 that the Employment Development Department failed to participate in a key aspect of a federal program that would have allowed it to collect an estimated $516 million owed to the State in unemployment benefit overpayments between February 2011 and September 2014. The investigations have also substantiated improper activities that cannot be quantified in dollars but have had negative social impacts. Examples include violations of fiduciary trust, failure to perform mandated duties, and abuse of authority.

Corrective Actions Taken in Response to Investigations

The chapters of this report have described the specific corrective actions that the relevant agencies implemented on individual cases that the state auditor completed from July 2015 through December 2015. Table A summarizes all of the corrective actions that agencies took in response to investigations between the time that the state auditor opened the hotline in July 1993 until December 2015. In addition to the corrective actions listed, these investigations have resulted in many agencies modifying or reiterating their policies and procedures to prevent future improper activities.

| TYPE OF CORRECTIVE ACTION | TOTALS |

|---|---|

| Convictions | 12 |

| Demotions | 22 |

| Job terminations | 87 |

| Resignations or retirements while under investigation* | 18* |

| Pay reductions | 55 |

| Reprimands | 327 |

| Suspensions without pay | 28 |

Source: California State Auditor.

* The number of resignations or retirements reflects those that occurred during investigations that the California State Auditor has completed since 2007.

The State Auditor’s Investigative Work From July 2015 Through December 2015

The state auditor receives allegations of improper governmental activities in several ways. From July 1, 2015, through December 31, 2015, the state auditor received 668 calls or inquiries. Of these, 117 came through the hotline, 228 through the mail, 318 through the state auditor’s website, and 5 were generated internally. When the state auditor determined that allegations were outside its jurisdiction, it referred the callers and inquirers to the appropriate federal, local, or state agencies, when possible.

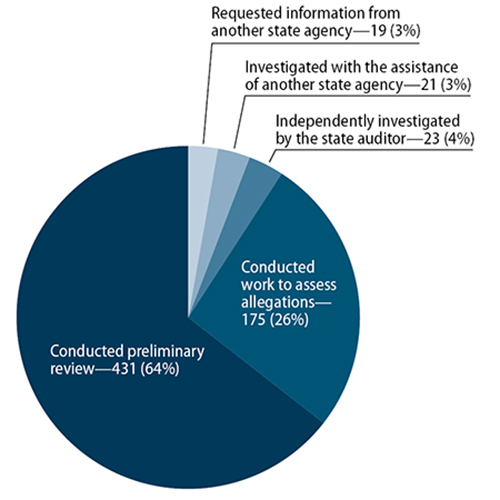

During this six-month period, the state auditor conducted investigative work on 669 cases that it opened either in previous periods or in the current period. As Figure A shows, after conducting a preliminary review of these allegations, the state auditor’s staff determined that 431 of the 669 cases lacked sufficient information for investigation. For another 175 cases, the staff conducted work—such as analyzing available evidence and contacting witnesses—to assess the allegations. In addition, the staff requested that state agencies gather information for 19 cases to assist in assessing the validity of the allegations. The state auditor’s staff investigated 23 cases independently and investigated 21 cases with assistance from other state agencies.

Figure A

Status of 669 Cases

From July 2015 Through December 2015

Source: California State auditor.