Introduction

Background

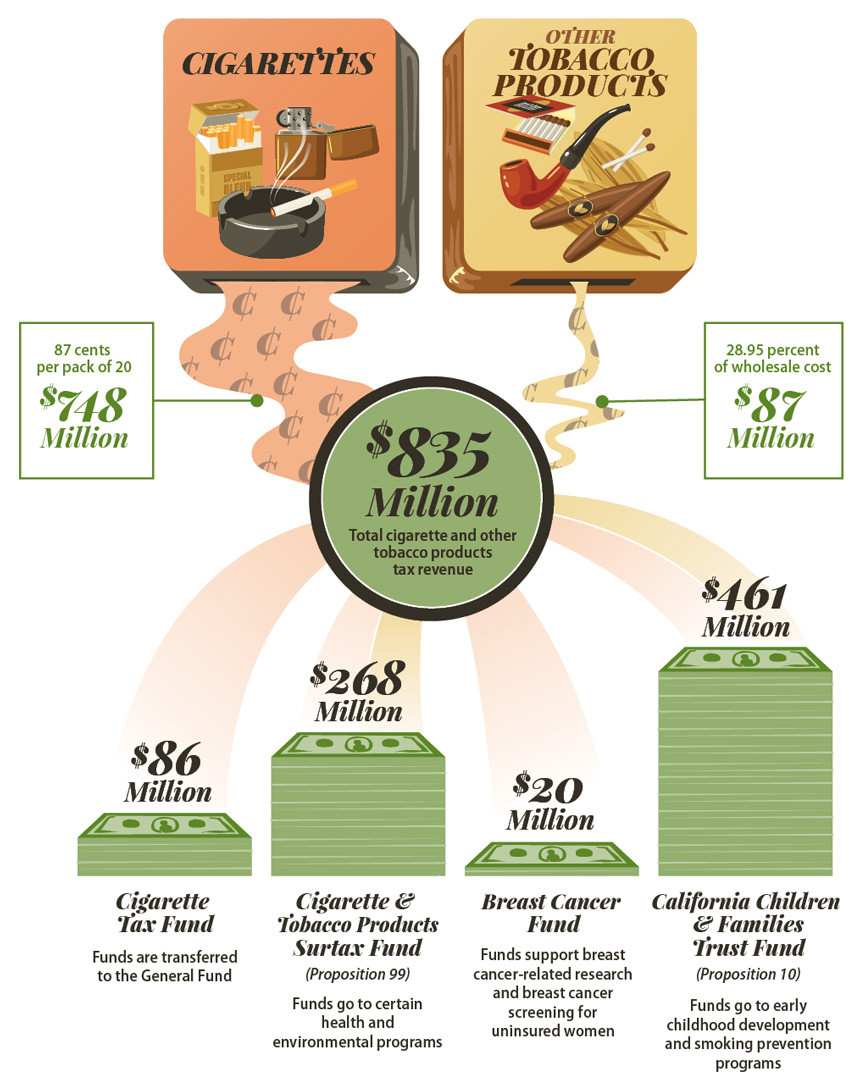

Cigarettes and tobacco products are subject to various federal, state, and local taxes and fees. In addition to charging a sales tax, California imposes on cigarettes and tobacco products certain excise taxes, which are taxes on the use or consumption of particular goods. As of January 1, 2016, California imposes an 87-cent excise tax on each pack of 20 cigarettes and an excise tax of 28.13 percent of the wholesale cost of tobacco products, which include chewing tobacco, smoking tobacco, and other products containing at least 50 percent tobacco.1 Distributors of cigarettes and tobacco products pay these taxes and usually pass these costs on to their consumers. As Figure 1 shows, most of the revenue from these excise taxes, which totaled $835 million in fiscal year 2014–15, is allocated to the State’s General Fund and programs established by two voter‑approved propositions: Proposition 99, passed in 1988 to provide funding for certain environmental programs as well as for tobacco-related health programs; and Proposition 10, passed in 1998 to fund early childhood development and smoking prevention programs.

Figure 1

California’s Revenue From Taxes on Cigarettes and Other Tobacco Products

During Fiscal Year 2014–15

Sources: Publication 93; Cigarette and Tobacco Products Taxes, June 2015, by the State Board of Equalization (board); the Department of Finance’s Manual of State Funds; Revenue and Taxation Code and Health and Safety Code; and documentation provided by the board’s accounting branch.

Note: Of the $835 million of taxes collected on cigarettes and other tobacco products in fiscal year 2014–15, the board used $30 million to pay for the administration, collection, and enforcement of these taxes. Each fund paid a share of this cost mostly in proportion to its share of the total taxes collected. Refer to Table A2 in the Appendix for additional information. The other tobacco product tax rate of 28.95 percent was in effect for fiscal year 2014–15.

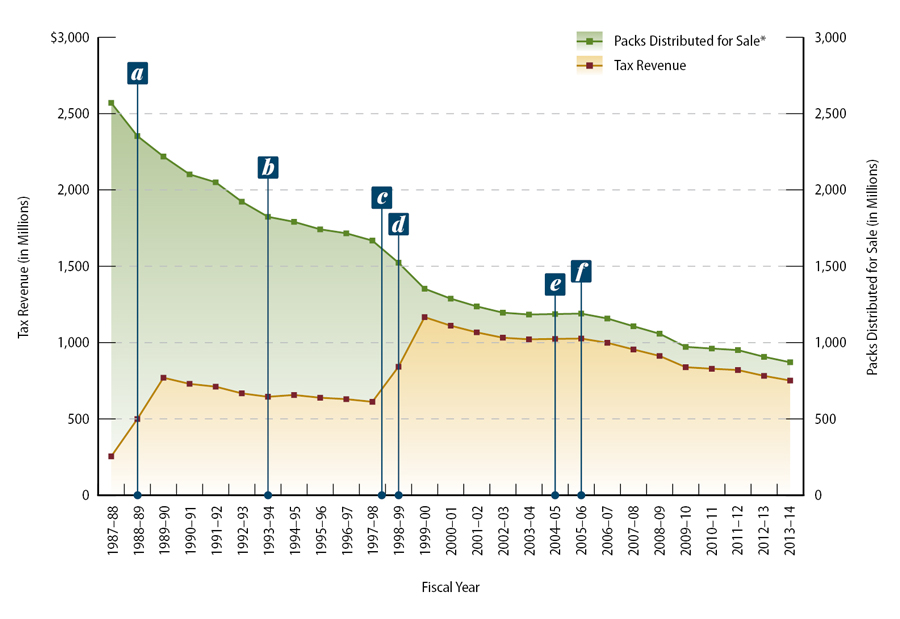

The sales of cigarettes for which distributors have paid the excise tax have steadily declined over time, as Figure 2 shows. This decline is primarily due to fewer people smoking. According to a report by the California State Board of Equalization (board), higher prices are one of the factors causing the downward trend in the number of cigarette packs sold. The report concludes that higher tax rates are usually passed on to consumers as higher prices. As Figure 2 shows, tax revenue spiked after Proposition 99 and Proposition 10 increased the excise tax by 25 cents and 50 cents per pack, respectively. However, revenue has steadily declined since fiscal year 2000–01, following when the excise tax was last increased, and this decrease in revenue parallels the ongoing decline in cigarette packs sold. Evasion of the excise tax is another possible reason for declines in revenue. The cigarette packs sold depicted in Figure 2 do not include untaxed cigarette packs or those for which distributors evaded the excise tax.

Figure 2

While Cigarette Tax Revenue Has Increased, the Number of Cigarette Packs Distributed for Sale Has Declined

Sources: The State Board of Equalization (board) Annual Report, fiscal year 2013–14; California Debt and Investment Advisory Commission’s report titled Issue Brief Tobacco Securitization Bond Issuance in California; and state law.

Note: Cigarette taxes were first imposed on July 1, 1959, at 3 cents per pack, and by October 1, 1967, the cigarette tax had increased to 10 cents per pack until January 1, 1989.

a) On January 1, 1989, the cigarette tax increased by 25 cents per pack (Proposition 99).

b) On January 1, 1994, the cigarette tax increased by 2 cents per pack.

c) In 1998 California entered into the Master Settlement Agreement with tobacco manufacturers to settle lawsuits for damages related to the health effects of smoking.

d) On January 1, 1999, the cigarette tax increased by 50 cents per pack (Proposition 10).

e) On January 1, 2004, the Cigarette and Tobacco Licensing Act went into effect.

f) On January 1, 2005, the requirement to use an encrypted tax stamp for cigarettes became effective.

* Does not include the distribution of tax-exempt cigarettes, which were 2 percent of all packs distributed in fiscal year 2013–14.

The board administers the excise taxes on cigarettes and tobacco products, performs such administrative functions as processing tax returns for distributors of cigarettes and tobacco products, and supplies cigarette distributors with tax stamps that they must affix to every package of cigarettes. State law requires that each pack of cigarettes have an encrypted tax stamp affixed to it; the stamp indicates that the distributor has paid the cigarette tax. The board’s collection of cigarette and tobacco product excise taxes and other administrative efforts constitute the board’s Cigarette and Tobacco Products Tax Program (tax program). In addition to administering the tax program, the board also enforces tax payment through its retail inspections, criminal investigations, civil audits—specialized audits that provide supporting documentation for the prosecution of criminal cases of tax evasion—and other enforcement activities. Generally, the board’s Investigations and Special Operations Division (investigations division) performs these enforcement activities. The Department of Justice helps the board prosecute tax evasion cases, and the Office of the Attorney General assists the board in enforcing tax payment on cigarette and tobacco products sold via other means, such as on the Internet, by telephone, and through mail orders.

Types of Activities Used to Evade Cigarette and Tobacco Products Taxes in California

Excise tax evasion through the illegal sale of untaxed cigarettes and other tobacco products takes many forms in California, including the following:

- Distributing untaxed tobacco products and cigarettes, including cigarettes bearing counterfeit, reused, or out‑of‑state tax stamps or cigarettes without a stamp.

- Purchasing untaxed products over the Internet or by mail order from out-of-state suppliers.

- Purchasing untaxed cigarettes and tobacco products from Indian tribal retail establishments by individuals who are not tribal members.

- Hijacking trucks transporting tobacco products and stealing unstamped and stamped domestic cigarettes.

- Establishing companies under false pretenses to acquire and distribute untaxed cigarettes and tobacco products. These companies typically vanish upon detection or selection for audit.

Source: Fiscal year 2013–14 Investigations Division Annual Report, State Board of Equalization.

Evasion of Tax Payments on Cigarettes and Tobacco Products

The board estimates that in fiscal year 2012–13, the State did not collect $214 million in tax revenue because sellers and consumers failed to pay required excise taxes on cigarettes and tobacco products. Retailers that purchased and sold cigarettes that lacked encrypted stamps or that purchased and sold other untaxed tobacco products are responsible for $198 million of the estimated $214 million in unpaid taxes. According to the board, consumers evaded an estimated $16 million in excise taxes by buying cigarettes and tobacco products in another state and transporting them back into California as well as by purchasing cigarette and tobacco products from another state or country on the Internet or by mail. According to the U.S. Government Accountability Office, illicit trade in cigarettes and tobacco occurs because it offers high rewards and low risks compared to crimes with high penalties, such as smuggling drugs. The investigations division reports that retailers who evade the excise tax can gain in two ways: They can increase their profit margins by selling untaxed cigarettes and tobacco products at the regular, taxed price, or they can pass the savings from their untaxed products along to their consumers in order to undercut the retailers’ competition and increase their market share. In either case, the State does not receive excise tax revenue from those products. The text box lists several types of evasion of the taxes on cigarettes and tobacco products that take place in California.

California’s Participation With Tobacco Companies in the Master Settlement Agreement for Damages Related to Smoking

In 1998 California and 45 other states entered into an agreement with the four largest tobacco manufacturers to settle a number of lawsuits against the manufacturers for damages related to the negative health effects of smoking. This agreement, known as the Master Settlement Agreement (MSA), imposes multiple obligations on participating tobacco manufacturers, including a requirement to make annual payments to each settling state in perpetuity. Annual MSA payments to California over the last five years have averaged a little more than $800 million per year, and the State has received a total of nearly $13.4 billion from 1999 through April 2015. One-half of this amount goes to local governments, while the other half goes to the State. In the past, to balance the budget, the State borrowed against its share of this payment stream by selling bonds. The State has pledged 100 percent of its share of settlement revenue to repay bondholders. As of 2014 the State still owed $18.4 billion on these bonds.

Although many tobacco manufacturers have agreed to participate in the MSA, some have not. Because they are not subject to the payments and other requirements, manufacturers that are not party to the MSA (nonparticipating manufacturers) could obtain a competitive advantage over the participating manufacturers. Therefore, the MSA provides that, in order to receive full payment, settling states must enact laws requiring the nonparticipating manufacturers to make payments to the states based on those manufacturers’ cigarette sales. Moreover, the settling states are obligated to diligently enforce these payment requirements by tracking all cigarettes sold within the states. If a state does not diligently enforce payments by nonparticipating manufacturers, participating manufacturers can seek to lower their payments through arbitration.

Cigarette and Tobacco Products Tax Enforcement

To ensure compliance with the MSA and decrease tax evasion, between January 2004 and June 2006 the board implemented two statutes—the Cigarette and Tobacco Products Licensing Act of 2003 (licensing act), which became effective on January 1, 2004, and another bill related to the cigarette tax stamp, which became effective on January 1, 2005. The licensing act expanded to retailers, manufacturers, and importers an existing statutory requirement for each wholesaler and distributor to obtain a license to sell cigarettes and tobacco products. The licensing act also created additional enforcement powers for the board, established additional penalties—including fines, imprisonment, and seizure of untaxed products—for distributors that engage in tax evasion activities, and appropriated $11 million from the Cigarette and Tobacco Products Compliance Fund to the board for the purpose of implementing the act. The board created the Cigarette and Tobacco Products Licensing Program (licensing program), which implements, enforces, and administers the licensing act through such activities as processing license applications and each year performing approximately 10,000 inspections of licensees, which are primarily retailers.

The second piece of tax enforcement-related legislation required the board to replace the existing cigarette tax stamp by January 1, 2005. The new stamp had to be readable by a scanning device and bear encrypted information, such as the name and address of the distributor affixing the stamp. According to the investigations division chief, switching from a traditional paper stamp to a high‑technology stamp with a hidden encrypted serial number has made authenticating cigarette tax stamps easier and more effective. According to the acting chief of the Special Taxes Policy and Compliance Division (special taxes division), the board does not use a tax stamp for tobacco products, such as chewing tobacco, because the law instead requires distributors to pay taxes on tobacco products by filing a tax return along with a remittance. During their inspections, investigations division inspectors verify tax payments for tobacco products when the inspectors reconcile purchase invoices to the retailers’ inventories.

The board’s economist estimates that evasion of taxes on cigarette and tobacco products would be much higher each year without these enforcement improvements. For fiscal year 2012–13, the most recent estimate available, the economist believes that evasion of the excise taxes would have been $91.3 million more than the $214 million in evaded taxes that the economist quoted for that year. The economist also estimates that evasion of an additional $44.4 million in state and local sales and in use taxes would have occurred were it not for the compliance improvements.

The retail license requirement, the encrypted cigarette tax stamp, and the inspections of retailers work together to ensure compliance with the excise tax requirements. Each of these three elements of cigarette and tobacco product tax enforcement is distinct yet interdependent. The requirement that retailers obtain licenses allows the board to identify retailers who sell cigarettes and tobacco products that investigations division inspectors must inspect for tax compliance. In addition, penalties for selling cigarettes without a retail license provide both an incentive for retailers to comply with the licensing requirement and a means for the board to enforce the requirement. According to the investigations division chief, the encrypted information within the tax stamp enables inspectors using scanners in retail stores to validate legitimate stamps immediately and to identify counterfeit ones even when those stamps appear visually identical to the real California tax stamp. Finally, inspections of retailers help prevent retailers from simply selling cigarettes illegally with no stamps or with counterfeit stamps. Similarly, such inspections also discourage retailers from selling tobacco products without paying the excise and other taxes.

License and Administrative Fees on Cigarettes and Other Tobacco Products That the Board Collects and Uses to Help Pay for Its Licensing Program

Retailer—$100 one-time license fee to sell cigarettes and other tobacco products.

Distributor and wholesaler—$1,000 annual license fee to distribute or sell cigarettes and other tobacco products.

Manufacturer and importer of chewing tobacco or snuff—one-time license fee of $10,000.

Manufacturer and importer of tobacco products, including cigarettes but excluding chewing tobacco or snuff—one-time license fee of $2,000.

Cigarette manufacturer or importer—one-time administrative fee based on its respective market share of cigarettes manufactured or imported and sold in California during the next calendar year.

Source: California Business and Professions Code.

Sources of Funding for the Board’s Tax and Licensing Programs

License fees and penalties as well as cigarette and tobacco products taxes are the primary sources of funding for the licensing program. As the text box shows, the act that helps fund the licensing program imposes various fees on the companies involved in the sale of cigarettes and tobacco products in California.

These fees brought in about $1.8 million in fiscal year 2014–15. However, the licensing program’s costs for the same period were more than $9.8 million, leaving a shortfall of roughly $8.0 million between the licensing program’s revenue and its costs. The board’s licensing program costs first exceeded available funding in fiscal year 2006–07, and shortages have occurred in every subsequent year. To cover this ongoing funding shortfall, the board imposes a charge against each fund that receives cigarette and tobacco tax revenue. Specifically, each fund covers a portion of the shortfall that is roughly equivalent to the proportion of all revenue from cigarette and tobacco products taxes that the fund receives.

Unlike the licensing program, which covers some of its costs with license fees and penalties, the tax program is funded entirely by cigarette and tobacco products taxes. Its costs in fiscal year 2014–15 were $22.4 million. Similar to the licensing program, the tax program has its costs spread across each of the four funds receiving cigarette and tobacco products taxes, with each fund paying a share of costs that is roughly in proportion to its share of total excise tax revenue. More than one‑third of the tax program’s costs are for the encrypted cigarette tax stamp, which is one facet of the board’s tobacco tax enforcement efforts. The Appendix shows additional detail on both programs’ expenditures and funding sources over the past five fiscal years.

Overview of the Board’s Methods for Allocating Costs

The board does not have dedicated staff for either the tax or the licensing program. Instead, the special taxes division manages program area work, such as processing license registrations, processing tax returns and billings, handling appeals and refunds, and providing tax advice. Both the staff of the special taxes division, which conducts tax audits, and the staff of the investigations division, which performs enforcement and compliance activities, work on the tax and licensing programs. Additionally, staff of these two divisions conduct activities related to the 27 other tax and fee programs that the board administers.

The board allocates in several ways the direct and indirect program costs for all programs, including the tax and licensing programs. For direct personnel service costs, the board allocates these costs based on the percentage of hours that staff in each division work directly on a particular program; the board uses the average pay for each different personnel classification. The board also allocates direct operating expense and costs using the percentage of hours that staff from each division directly charge to each program. Additionally, the board allocates costs of several indirect support units—including those related to technology, legal, and cashier services—based on actual use. For example, the cashier unit costs are allocated to programs based on the number of transactions the unit processes for each program. Further, after calculating each program’s share of direct and indirect unit costs, the board allocates what it refers to as distributed administration, which includes costs for accounting, human resources, and any other units that support the board as a whole. Each program is allocated a portion of distributed administration based on a program’s overall share of direct and indirect costs. Finally, the board distributes its share of the costs of the centralized administrative services provided to all state agencies and departments, known as pro rata costs, to its programs in proportion to the programs’ funding levels.

Scope and Methodology

The Joint Legislative Audit Committee (audit committee) directed the California State Auditor’s Office to perform an audit of the costs to administer the board’s tax and licensing programs. Table 1 includes the audit objectives that the audit committee approved and the methods we used to address them.

| Audit Objective | Method | |

|---|---|---|

| 1. | Review and evaluate the laws, rules, and regulations significant to the audit objectives. | We reviewed relevant laws, regulations, and other background materials applicable to California’s cigarette and tobacco products taxes. |

| 2. | Review the policies of the State Board of Equalization (board) as well as its procedures and practices for identifying tax program versus licensing program costs to ensure the following: | We reviewed relevant administrative policies, procedures, and practices, and interviewed budget and accounting staff. We evaluated the board’s cost allocation plan by selecting expenditures and time charges, and determining whether they adhered to the plan and to other board policies and practices for allocating costs. |

| a. Compliance with all relevant laws, rules, and regulations. | ||

| b. The reasonableness of costs and staffing allocated to each program. | ||

| 3. | For the past five fiscal years, determine the sources and amounts of funding used by the licensing program and whether this funding is consistent with applicable laws. | We obtained documentation from the board to determine the sources and amounts of funding used by the licensing program. We also reviewed applicable laws and determined that the funding was consistent with applicable laws. |

| 4. | Review and evaluate the board’s approach for determining how to effectively and efficiently manage the tax and licensing programs while maximizing the revenue generated by tobacco excise taxes and the Master Settlement Agreement. To the extent possible, recommend other methods to further reduce administrative costs. | We interviewed board staff that manage the licensing and tax programs. We evaluated outcomes of the licensing program, such as seizures of cigarettes and other tobacco products during inspections, and we evaluated the frequency of inspections of cigarette and tobacco products retailers. |

| 5. | Determine whether the current level of funding is reasonable to maintain the tax and licensing programs’ effectiveness and whether funding and resources are being used for other purposes. To the extent possible, determine what a selection of other states is doing to enforce those states’ cigarette and tobacco programs. | We evaluated the effectiveness of the tax and licensing programs in the course of addressing objectives 1 through 4. Further, when we determined the sources and amounts of funding used by the licensing program, we also determined that those funds were not being used for other purposes. We interviewed chief investigators and tax administrators involved in cigarette and tobacco products tax enforcement in four other states to determine the enforcement methods that they use and compared these methods to those of California. We selected four states that share one or more of the following characteristics with California: a large population, an international border, or a location in the West. |

| 6. | Review and assess any other issues that are significant to the audit. | We did not find any other issues relevant and significant to this audit. |

Sources: The California State Auditor’s analysis of Joint Legislative Audit Committee audit request 2015-119 and information and documentation identified in the table column titled Method.

Assessment of Data Reliability

In performing this audit, we relied on data from the information systems listed in Table 2. The U.S. Government Accountability Office, whose standards we are statutorily required to follow, requires us to assess the sufficiency and appropriateness of computer-processed information that we use to support our findings, conclusions, or recommendations. Table 2 describes the analyses we conducted using data from these information systems, our methodology for testing them, and the result of our assessment which is, the data is not sufficiently reliable for our audit purposes. Although this determination may affect the precision of the numbers we present, there is sufficient evidence in total to support our audit findings, conclusions, and recommendations.

| Information System | Purpose | Method and Result | Conclusion |

|---|---|---|---|

| State Board of Equalization (board) Revenue and cost allocations databases and spreadsheets for fiscal years 2010–11 through 2014–15 |

|

We obtained data related to the board’s tax and licensing programs’ expenditures and funding sources from a series of Microsoft Access databases (Access) and Excel spreadsheets (Excel). The board uses computer code written in Access and Excel to allocate its tax and licensing programs’ costs and revenues. Due to the complexity of the calculations related to these allocations, we determined that it was cost prohibitive to perform a review of these allocations. However, to gain some assurance of the accuracy of the tax and licensing program expenditures, we tested a selection of fiscal year 2014–15 expenditures and hours worked. We also analyzed the board’s cost allocation plan. We found that the operating expenditures were reasonably allocated. As discussed in the Audit Results, we determined that some of the hours worked—which the board uses as a basis for allocating costs—were not accurate. Further, to assess the completeness of fiscal year 2014–15 financial records, we reviewed the tax and licensing programs’ combined total expenditures and revenues from each cigarette and tobacco tax fund. The funds we reviewed included the Cigarette Tax Fund, the Breast Cancer Fund, the Cigarette and Tobacco Products Surtax Fund, and the California Children and Families Trust Fund. For each of these funds, we compared fiscal year 2014–15 financial statement records with documentation from the State Controller’s Office (controller). We found that the amounts reported by the board reconciled to the controller’s records. |

Not sufficiently reliable for these audit purposes. Although this determination may affect the precision of the numbers we present, there is sufficient evidence in total to support our audit findings, conclusions, and recommendations. |

Sources: California State Auditor’s analysis of various documents, interviews, and data obtained from the board.

Footnotes

1 This tax rate was effective on July 1, 2015, and is for fiscal year 2015–16. Go back to text