State High-Risk Audit Program

The California State Auditor’s Updated Assessment of Issues and Agencies That Pose a High Risk to the State

August 24, 2023

2023-601

The Governor of California

President pro Tempore of the Senate

Speaker of the Assembly

State Capitol

Sacramento, California 95814

Dear Governor and Legislative Leaders:

As required by Government Code section 8546.5, my office presents this report about statewide issues and state agencies that represent a high risk to the State or its residents. Our work to identify and address such high-risk statewide issues and agencies aims to enhance efficiency and effectiveness by focusing the State’s resources on improving the delivery of services related to important programs or functions.

We describe in this report four high-risk statewide issues that include aspects of state management of COVID-19 federal funds, state management of financial reporting and accountability, information security, and water infrastructure. We also conclude that three state agencies meet our criteria to be designated as high-risk: the Employment Development Department, the California Department of Technology, and the Department of Health Care Services. Finally, we have removed from our state high-risk list higher education, the California State Teachers’ Retirement System, other postemployment benefits, the California Department of Public Health, transportation infrastructure, and the California Department of Corrections and Rehabilitation. We have based these decisions on factors including changes in circumstances and the significant progress that the State has made toward mitigating various risk factors.

We will continue to monitor the risks we have identified in this report and the actions the State takes to address them. When the State’s actions result in significant progress toward resolving or mitigating such risks, we will remove the high-risk designation based on our professional judgment.

Respectfully submitted,

GRANT PARKS

California State Auditor

Selected Abbreviations Used in This Report

| ACFR | Annual Comprehensive Financial Report |

| CalPERS | California Public Employees’ Retirement System |

| CalSTRS | California State Teachers’ Retirement System |

| CCC | California Community Colleges |

| CDCR | California Department of Corrections and Rehabilitation |

| CDT | California Department of Technology |

| CSU | California State University |

| DHCS | Department of Health Care Services |

| DOL | Department of Labor |

| EDD | Employment Development Department |

| IT | information technology |

| MHSA | Mental Health Services Act |

| OIG | Office of the Inspector General |

| OPEB | other postemployment benefits |

| PAL | Project Approval Lifecycle |

| UC | University of California |

| UI | Unemployment insurance |

Contents

| High-Risk Issue or Agency | Responsible Agency | Report Section | On List Since |

|---|---|---|---|

| Introduction | |||

| New High-Risk Agency | |||

| Employment Development Department | Employment Development Department | EDD Is High-Risk Because of Inadequate Fraud Prevention and Claimant Service, as Well as a High Rate of Overturned Eligibility Decisions in Its Unemployment Insurance Program | 2023 |

| Retained on High-Risk List | |||

| State Management of COVID‑19 Federal Funds | Various Agencies | The State’s Management of COVID‑19 Federal Funds Continues to Be a High-Risk Issue | 2020 |

| State Financial Reporting and Accountability | Department of FI$Cal and Various Agencies | Late Financial Reporting Continues to Increase Risk to the State | 2020 |

| Information Security | California Department of Technology and Various Agencies | The State’s Information Security Remains a High-Risk Issue | 2013 |

| Information Technology Oversight | California Department of Technology | CDT Has Not Made Sufficient Progress in Its Oversight of State Information Technology Projects | 2007 |

| Water Infrastructure and Availability | Department of Water Resources and the Governor’s Office of Emergency Services | Climate Change and Aging Water Infrastructure Threaten California’s Water Supply and Public Safety | 2018 |

| Department of Health Care Services | Department of Health Care Services | Health Care Services Has Not Adequately Addressed Issues With Medi-Cal Eligibility, But It Has Made Improvements to Its MHSA Oversight | 2007 |

| Removed From High-Risk List | |||

| Higher Education | California State University and University of California | CSU and UC Have Made Efforts to Control Tuition and Fees in the Past Decade | 2013 |

| California State Teacher’s Retirement System | California State Teacher’s Retirement System | CalSTRS Has Implemented Corrective Action to Decrease the Risk Posed by Its Unfunded Liability | 2011 |

| Other Postemployment Benefits | Department of Finance, California Department of Human Resources, and California Public Employees’ Retirement System | The State Is Addressing Its OPEB Liabilities | 2007 |

| California Department of Public Health | California Department of Public Health | Public Health Has Made Sufficient Progress in Implementing Outstanding Recommendations | 2007 |

| Transportation Infrastructure | California Department of Transportation and California Transportation Commission | The State Has Made Sufficient Progress in Improving Its Transportation Infrastructure | 2007 |

| California Department of Corrections and Rehabilitation | California Department of Corrections and Rehabilitation | CDCR Is Making Progress in Improving Its Health Care Delivery | 2007 |

| Responses to the Audit | |||

| California Governor’s Office of Emergency Services (CalOES) | |||

| California State Auditor’s Comment on the Response From CalOES | |||

| California State Transportation Agency (CalSTA) | |||

| California Department of Public Health (Public Health) | |||

| California Department of Technology (CDT) | |||

| California State Auditor’s Comments on the Response From CDT | |||

| Department of Health Care Services (DHCS) | |||

| California Natural Resources Agency | |||

| The California State University Office of the Chancellor | |||

| California Employment Development Department (EDD) | |||

| California State Auditor’s Comments on the Response From EDD | |||

| Financial Information System for California (FI$Cal) | |||

| California State Auditor’s Comment on the Response From FI$Cal | |||

| Department of Finance (Finance) | |||

| California State Auditor’s Comments on the Response From Finance | |||

Introduction:

Background

State law authorizes the California State Auditor (State Auditor) to develop a state high-risk government agency audit program (high‑risk program). Our office implemented this program to improve the operation of state government by identifying, auditing, and recommending improvements to state agencies and statewide issues at high risk for waste, fraud, abuse, or mismanagement or for having major challenges associated with their economy, efficiency, or effectiveness. In accordance with this statutory authority, the State Auditor adopted regulations in 2016 that further define the high-risk program. These regulations provide the criteria we used in determining the list of state high-risk agencies and statewide issues we present in this report.

Criteria for Determining Whether a State Agency or Statewide Issue Merits a High‑Risk Designation

State regulations outline the conditions under which an agency or issue may be added to the State Auditor’s high-risk list. All four of the following conditions must be present for us to assign the high‑risk designation:

- Potential waste, fraud, abuse, or mismanagement or impaired economy, efficiency, or effectiveness that may result in serious detriment to the State or its residents.

- The likelihood of waste, fraud, abuse, or mismanagement or the likelihood of impaired economy, efficiency, or effectiveness causing harm is so great that this likelihood constitutes a substantial risk of detriment to the State or its residents.California Code of Regulations, title 2, section 61015 (a), defines substantial risk and directs the State Auditor to assess “whether the likelihood of the waste, fraud, abuse, or mismanagement or impaired economy, efficiency, or effectiveness being risked by a state agency or a statewide issue is great enough, when compared with the level of serious detriment that may result, for there to be substantial risk of serious detriment to the State or its residents.”

- The state agencies that are affected by or responsible for resolving the waste, fraud, abuse, or mismanagement or the impaired economy, efficiency, or effectiveness are not taking adequate corrective actions to prevent the risk or its effects.

- An audit and the agencies’ implementation of the resulting recommendations may significantly reduce the substantial risk of serious detriment to the State or its residents.

When assessing both state agencies and statewide issues, we consider a number of factors to determine whether there is substantial risk to the State or its residents. We consider whether the risks are already causing detriment, whether those risks are increasing, and whether changes in circumstances are likely to cause detriment. We also consider various factors to determine whether the risks may have serious effects, such as loss of life, injury, or a reduction in residents’ overall health or safety; impairment of the delivery of government services; significant reduction in the overall effectiveness or efficiency of state government programs; and infringement on citizens’ rights. Finally, in evaluating whether agencies have taken adequate measures to correct previously identified deficiencies, or whether the State has taken measures to reduce the risks posed by the issues, we consider factors such as whether the agencies have demonstrated a strong commitment to controlling or eliminating the risk and whether they have made significant progress through action already taken to control or eliminate the risk to the State. In all cases, our professional staff make the final determination of risk level according to their independent and objective judgment.

Removal of High-Risk Designation

We remove the high-risk designation under any of the following circumstances:

- A change in circumstances has resulted in the risk no longer presenting the potential for serious detriment to the State or its residents.

- The agency has taken sufficient corrective action to prevent or mitigate the risk of harm.

- The risk presented by the agency or issue is not likely to be reduced by performing additional audit work.

State regulations require us to use our professional judgment to determine whether to remove a high-risk designation. When we remove the high-risk designation for one of the reasons described above, we continue to monitor the issue or agency and, if the risk reoccurs, we will consider reinstating the high-risk designation according to the factors described earlier.

State High-Risk Reports

Government Code section 8546.5 authorizes the State Auditor to audit and to publish audit reports on any state agency that it identifies as high-risk. In May 2007, we issued Report 2006‑601, which provided an initial list of high-risk state agencies and statewide issues. We have since issued several reports updating the list of those agencies and issues that are high-risk. Further, we include on our website a list of all audits that we are performing, including those of high-risk state agencies and statewide issues.

To update our assessment of high-risk state agencies and statewide issues, we interviewed knowledgeable staff at the responsible state agencies to gain perspective on the extent of the risks the State faces. We also reviewed the efforts that staff at the agencies said were underway and were intended to mitigate the identified risks. In addition, we reviewed reports and other documentation relevant to the issues. Finally, we conferred with agencies and interested parties, such as the Department of Finance, the Legislative Analyst’s office, and the Public Policy Institute of California. Each of the entities we conferred with provided its perspective on high-risk areas facing the State.

New High-Risk Agency:

EDD Is High-Risk Because of Inadequate Fraud Prevention and Claimant Service, as Well as a High Rate of Overturned Eligibility Decisions in Its Unemployment Insurance Program

Background

The Employment Development Department (EDD) provides billions of dollars in partial wage replacement benefits each year to Californians who need and seek such benefits (claimants). One of EDD’s primary responsibilities is its administration of the unemployment insurance (UI) program. Funded by taxes on employers, the UI program provides temporary financial assistance to unemployed workers who meet specific eligibility requirements, including those workers who were affected by the COVID-19 pandemic.

Beginning in March 2020, a surge in pandemic-related unemployment claims increased EDD’s UI workloads and resulted in changes to federal UI benefit programs, both of which created a greater risk of fraud. In Report 2020-628.2, January 2021, we explained that EDD’s fraud prevention approach during the pandemic was marked by significant missteps and inaction that led to billions of dollars in unemployment benefit payments that EDD later determined may have been fraudulent. Further, we also reported that EDD has been unable to accurately quantify its inappropriate UI payments, contributing to the delayed publication of California’s financial statements for the two most recently published fiscal years and to modified audit opinions on those statements. Modified opinions included disclaimers of opinion and qualified opinions. An auditor expresses a disclaimer of opinion when the auditor is unable to obtain sufficient appropriate audit evidence on which to base the opinion, and the auditor concludes that the possible effects on the financial statements of undetected misstatements, if any, could be both material and pervasive. An auditor expresses a qualified opinion when the auditor concludes that the possible effects on the financial statements of misstatements or undetected misstatements, if any, could be material but not pervasive. For the year ending June 30, 2020, we issued a disclaimer of opinion for the Unemployment Programs Fund and qualified opinions for Business-Type Activities and the Federal Fund. For the year ending June 30, 2021, we issued a disclaimer of opinion for the Unemployment Programs Fund and qualified opinions for Governmental Activities, Business‑Type Activities, and the Federal Fund.

Moreover, as we described in Report 2020‑128/628.1, January 2021, EDD did not prepare for an economic downturn despite multiple warnings, a key example of which is EDD’s slow efforts to improve its UI call center and overall claimant experience. Because the department did not address longstanding problems with the efficiency of its UI customer service, including its call center, EDD was unable to answer claimant questions and process claims in a timely and accurate manner during the pandemic.

Assessment

EDD is a high-risk agency because of its mismanagement of the UI program. Specifically, EDD is unable to reliably estimate improper payments under the UI program, thus adversly affecting the State’s financial statements as well as impairing efforts to independently evaluate the efficacy of EDD’s own fraud prevention activities. Further, EDD needs to improve customer service to unemployment insurance claimants, while also taking steps to ensure its eligibility decisions are not frequently overturned on appeal. EDD’s mismanagement of the UI program has resulted in a substantial risk of serious detriment to the State and its residents. A high-risk audit may result in recommendations that could substantially reduce the risks we have identified.

Substantial Fraud Risk Exists in EDD’s UI Program

EDD’s administration of the UI program has resulted in the substantial risk of serious detriment Per California Code of Regulations, title 2, section 61014, in evaluating the risk of serious detriment, the State Auditor considers whether any of eight circumstances—such as an increase in state liabilities that significantly affects the State’s finances or impairment of the delivery of important government services—may result. to the State and its residents. In addition to providing temporary wage replacement to unemployed workers, the UI program helps maintain the stability of the state economy during economic downturns. Despite the program’s critical importance, EDD’s management of the UI program has been characterized by significant internal control weaknesses. For example, the program did not block addresses used to file unusually high numbers of claims, and it removed a safeguard preventing payment to individuals who had unconfirmed identities. These inadequate internal controls did not prevent potential fraud during fiscal years 2019–20 and 2020–21 and allowed the payments of potentially fraudulent claims, estimated at tens of billions of dollars, most of which have yet to be recovered.

Contributing to this serious detriment, EDD’s inadequate identification of potentially fraudulent UI benefit payments was also a significant factor leading to modified audit opinions and the delayed publication of California’s Annual Comprehensive Financial Report (ACFR) for fiscal years 2019–20 and 2020–21, which the State Controller published in February 2022 and March 2023, respectively. Further, our contractor responsible for conducting the federal compliance component of the Single Audit found areas of material weakness and noncompliance in EDD’s administration of the UI program during the pandemic, which led the contractor to issue an adverse opinion in the State’s fiscal year 2020–21 Federal Compliance Audit, published in April 2023, indicating that the State did not comply in all material respects with specific program requirements that could have a direct and material effect on the program. The delayed publication of the ACFRs and related audit opinions substantially delayed the public’s ability to gain an understanding of California’s financial position. The impacts on the State’s financial reporting could also be a contributing factor toward any potential decision to lower the State’s credit rating. We discuss our additional concerns about late financial reporting that may adversely affect the State’s credit rating.

EDD has not taken adequate corrective action to prevent the substantial risk of serious detriment to the State and its residents. Corrective action is adequate when it prevents a risk—such as the risk of fraud—from presenting a substantial risk of serious detriment. Because the potentially fraudulent payments have already occurred, have not been fully identified, and have largely not been recovered, EDD’s corrective action is not adequate. Nevertheless, EDD deserves credit for taking some steps to strengthen its internal controls, such as partnering with vendors and data scientists to identify potentially fraudulent claims and to refer those cases to law enforcement agencies for further investigation and potential criminal prosecution, but significant work remains. For example, EDD cannot effectively measure its progress at addressing potentially fraudulent payments because it is unable to accurately determine how many improper payments it has made. We noted this issue in Report 2021-001.1, March 2023, the report that reviewed internal controls and compliance. In fact, we found that EDD’s estimate of potentially fraudulent payments omitted certain payments to claimants who made false statements to obtain benefits and also incorrectly included valid claims for benefits. EDD has established a process to pursue recovery of ineligible payments, but until it identifies all inappropriate transactions, it cannot effectively manage that process or allocate appropriate resources to pursuing recovery. Thus EDD’s current corrective action remains insufficient and is a contributing element to our designation of the agency as high‑risk.

EDD Has Not Provided California Residents With Sufficient Customer Service, Resulting in Significant Challenges to Obtaining UI Benefits

Like the fraud risk noted above, EDD’s handling of other components of the UI program also presents a substantial risk of significant detriment to Californians. EDD has faced longstanding efficiency problems in providing customer service to UI claimants. During the pandemic, millions of Californians were required to wait long periods to receive UI benefits or get answers to questions about their UI claims, and EDD continues to struggle to pay claimants in a timely manner. EDD’s customer service for the UI program has resulted in the impaired delivery of an important government service.

EDD has taken action to begin addressing customer service deficiencies in its UI program; however, those actions are not yet adequate. For example, as of April 2023, EDD had implemented many of our January 2021 recommendations and has since improved performance, but claimants still experience difficulties contacting EDD and being paid on time. Between January and May 2023 individuals called EDD on average between three and eight times a week trying to get help on their claims. In another example, according to statistics published by the U.S. Department of Labor (DOL), although EDD’s timeliness of first payment on a UI claim has improved since the worst of the COVID-19 pandemic, it does not yet meet DOL’s acceptable level of performance. Specifically, in the first six months of 2023, EDD paid between a high of 86 percent of claims and a low of 81 percent of claims within the time frame established by DOL, and it has not yet met DOL’s 87 percent acceptable level of performance. Consequently, these improvements are not sufficient to prevent the impaired efficiency and effectiveness of EDD’s UI program from presenting a substantial risk to California residents.

Many of EDD’s UI Eligibility Decisions Are Not Upheld on Appeal

Apart from the potentially fraudulent UI payments that EDD made during the pandemic, which it has estimated to be in the tens of billions of dollars and which continue to affect the State’s financial reporting, EDD’s eligibility decisions are frequently overturned during appeal and have resulted in the substantial risk of serious detriment to California residents. Specifically, EDD’s improper decisions regarding UI benefits have required some UI claimants to face even longer delays than are typical. From 2017 through 2022, about half of the issues in UI claims that claimants appealed were ultimately overturned in favor of the claimant. This rate of overturned decisions is consistent with the high rate of overturned decisions we noted in Report 2014-101, August 2014. Although EDD wants to reduce the percentage of overturned appeals, it asserts that one of the reasons for the high rate of overturned decisions is that claimants can provide new information during their appeal that was not furnished to EDD during the claim filing process, leading many appeals to be decided in the claimants’ favor. Nevertheless, as of March 2023, California had the third highest reversal rate in the nation. These improper eligibility decisions can serve as unnecessary obstacles to claimants’ right to benefits and can result in a significant reduction in the overall effectiveness of the UI program. Thus they present a substantial risk of serious detriment to the State and its residents.

EDD has not taken adequate steps to prevent improper denials of UI benefits. Although EDD says that it is evaluating the UI appeals process in hopes of reducing the high rate of issues overturned on appeal, it has not taken sufficient action to address this problem, as evidenced by the fact that approximately half of the issues that claimants appealed between 2017 and 2022 were overturned, as was the case when we previously reported on this issue in August 2014. Thus, these actions are not sufficient to prevent the impaired efficiency and effectiveness of EDD’s UI program from presenting a substantial risk to California residents.

An Audit May Lead to Policy Changes That Significantly Reduce These Risks

Additional audit work by the State Auditor may assist EDD in mitigating the risk presented by its handling of the UI program. In particular, a high-risk audit would provide independently developed and verified information regarding EDD’s management of the UI program and its challenges. A high-risk audit would also include analyses that serve as the basis for recommendations to assist EDD in resolving the risks presented by its management of the UI program. For example, an audit could evaluate EDD’s efforts to identify potentially fraudulent or improper UI claims, which would lead to recommendations on how to effectively address the associated payments and properly account for them in a timelier manner. A deeper examination of EDD’s UI claimant service and its high rate of denied UI claims overturned on appeal could result in recommendations on how to improve the UI claims process and how to reduce the high rate of denied UI claims overturned on appeal.

EDD's response, and State Auditor’s comments

Retained High-Risk Agencies and Issues:

The State’s Management of COVID-19 Federal Funds Continues to Be a High-Risk Issue

Background

As part of its response to the COVID-19 pandemic, the federal government provided the State with nearly $290 billion in relief funds, portions of which must be obligated or spent by December 2024. The effective use of these funds required the State to allocate them to departments quickly and to expedite program changes, including eligibility updates. The State used COVID-19 funds to support programs related to vaccinations, unemployment benefits, housing assistance, and fiscal recovery. State departments received COVID-19 funds to operate more than 35 existing federal programs and to create new state programs, such as the HomeKey program, which provided temporary shelter to people experiencing homelessness or at risk of homelessness during the pandemic. One of the largest recipients of COVID-19 funds was EDD, which used a significant portion of the funds to provide unemployment benefits.

We initially designated the State’s management of federal funds related to COVID-19 as a high-risk statewide issue in August 2020. We based our initial assessment on the confluence of fiscal and programmatic changes that were critical to the State’s response to the pandemic. The State used COVID-19 funds in large part to support significant expansions of critical benefits for people experiencing unemployment, homelessness, and limited income. The rapid growth of programs providing these benefits posed a significant risk to the State and its residents. Specifically, inadequate outreach to people who needed the programs or the flawed execution of expansion efforts would create a risk that Californians would be left without medical care or money to pay for food and housing. Likewise, the swift creation of new programs by state departments posed risks because of the limited time available to implement sufficient internal controls and processes.

To assist in addressing these risks, we performed 11 state high-risk audits related to the management of COVID-19 funds. We found that state departments faced significant hurdles in using this influx of funding to meet the corresponding increase in responsibilities, such as the massive increase in the number of unemployment insurance claims requiring eligibility determinations and the rapid expansion of vendor oversight necessary for programs that provided pandemic-specific goods and services, like personal protective equipment. The scale and expeditious nature of the funding and its uses to provide services led to the high risk of inefficiencies and fraud occurring in programs supported by COVID-19 funds.

In total, our 11 prior state high-risk audits of COVID-19 fund management resulted in 85 recommendations to departments, of which 37 remain unimplemented. For example, our audit of the Board of State and Community Corrections (Board of Corrections) found that the Board of Corrections allocated funds to the California Department of Corrections and Rehabilitation without justification and that its allocation methodology did not consider important elements, such as the impact of the pandemic. The Board of Corrections also failed to make funding available to cities and tribes, even though it had originally committed to do so. We made 10 recommendations to the Board of Corrections in Report 2021-616, October 2021, but as of July 2023, it had only fully implemented three of our recommendations. We will continue to monitor the steps departments take to minimize the remaining risks related to their handling of COVID-19 funds.

Assessment

The management of COVID-19 funds continues to represent a significant risk to the State and its residents and will therefore remain a high-risk issue. In the previous section, we described our concerns with EDD, one of the largest recipients of COVID-19 funds, which used a significant portion of the funds to provide unemployment benefits. Since our last high-risk assessment in August 2021, at least 14 state agencies have received $76 billion in additional federal COVID-19 funding. State agencies will continue to spend some of these funds through December 31, 2024. This influx of resources represents both a significant benefit and risk to the State, as represented by the extent of our previous findings on the management of federal COVID-19 funding and the status of unimplemented recommendations.

The State continues to spend federal COVID-19 funds, meaning circumstances have not significantly changed. Further, a number of recommendations from our previous reports have not yet been implemented. For instance, we recommended that various university campuses review the expenses they incurred in response to the pandemic and submit eligible expenses to the federal government for reimbursement. We also recommended that the Department of Housing and Community Development develop a strategy it can use in emergency situations to more efficiently complete or amend contracts, and make funding available to recipients. These recommendations have not been fully implemented. Moreover, additional audit work by the State Auditor could assist in mitigating the risks associated with the management of federal COVID-19 funds. As with our 11 previous state high-risk audits on COVID-19 fund management, additional audits of this issue could generate recommendations to ensure that such funds are spent prudently, within acceptable time frames, and in accordance with federal and state requirements. Consequently, we will retain this issue on the high-risk list.

Status: Retained on high-risk list

EDD's response, Finance's response

Late Financial Reporting Continues to Increase Risk to the State

Background

The accuracy and timeliness of the State’s financial reporting is of vital importance to the State and its residents. A key method the State uses to provide fiscal oversight and transparency is the mandatory Annual Comprehensive Financial Report (ACFR) that the State Controller’s Office (State Controller) prepares. The ACFR is composed of financial statements from the State’s many departments and agencies, which collectively represent the financial position of the State. The report, which includes the State Auditor’s annual opinion of its accuracy, provides an important resource for stakeholders, such as the State’s creditors, to use when making decisions about the State’s ability to borrow money affordably. Further, billions of dollars in federal grants are contingent on the State’s timely filing of the ACFR for federal review.

To support its financial reporting needs, the State has focused significant effort on modernizing its financial management infrastructure through the implementation of a project known as the Financial Information System for California (FI$Cal). The scope, schedule, and budget of this nearly $1 billion information technology (IT) project has undergone numerous revisions since it began in 2005. However, despite nearly two decades of continued effort, many state entities have historically struggled to use the system to submit timely data for the ACFR.

In Report 2019-601, January 2020, the State Auditor added to the state high-risk list the State’s inability to produce timely financial reports during the transition to FI$Cal. At the time, we noted that since fiscal year 2017–18, the State had issued financial statements late, which could affect the State’s credit rating. The COVID-19 pandemic also created new financial complexities that affected the State’s financial reporting, such as the increased pandemic-related spending by the Employment Development Department (EDD) and its Unemployment Insurance fund. In Report 2021-601, August 2021, our assessment of high-risk issues to the State, we noted that the State Controller continued to issue the ACFR late.

Assessment

The State has not made sufficient progress in addressing late financial reporting; therefore, this issue will remain on the state high-risk list. The State Controller issued the State’s financial statements for fiscal year 2020–21 later than in previous years—twelve months after its traditional deadline and six months after a general extension on financial reporting that the federal government provided because of the pandemic. Further, the State’s financial reporting for fiscal year 2021–22 is already past due. This continued trend of late reporting reduces the efficiency and effectiveness of the State’s financial oversight. The State’s late financial reporting could also negatively affect its credit rating, which could increase the cost associated with borrowing. According to the State Treasurer, the State borrowed $5.6 billion in general obligation bonds in fiscal years 2021–22. Thus, even a small increase in the interest rate, as might happen with a downgraded bond rating, could cost the State millions annually in increased borrowing costs.

In addition to late financial reporting, the State is experiencing a decline in expected revenue. Although its financial reports in fiscal years 2017–18 through 2020–21 reported general fund surpluses, the Governor’s fiscal year 2023–24 budget had to address a budget shortfall of approximately $31.7 billion. Combining late financial reporting with a diminished financial outlook increases the risk that credit agencies will downgrade the State’s credit rating.

The State has made some limited progress in addressing underlying issues that have contributed to its late financial reporting but not enough progress to warrant removing the issue from the high-risk list. As we noted when we designated the State’s financial reporting as high-risk in January 2020, the transition to FI$Cal has been a key component in financial reporting delays. As of 2023, 152 of 162 state departments are now using the FI$Cal system for their financial reporting, with an additional two departments—the California Department of Technology and the Department of Rehabilitation—currently undergoing a two-year transition. Some departments are doing a better job of submitting their financial statements to the State Controller in a timely manner. For fiscal year 2021–22, departments filed year‑end financial statements within 30 days of the deadline for 1,400 funds, or about 80 percent of all the State’s funds. A fund is a group of self-balancing accounts created with a particular purpose and that has a prescribed authority for expending monies in it. For example, an agency’s general fund is used to finance its daily operations.

However, as we noted in our internal control and compliance audit Report 2021‑001.1, March 2023, six large departments of material importance to the State’s overall financial reporting did not perform monthly reconciliations of their accounts to the records of the State Controller in a timely manner during fiscal year 2020–21. Moreover, similar to the previous two fiscal years, the Department of Health Care Services (DHCS) did not fully reconcile its banking activity using FI$Cal before submitting its fiscal year 2020–21 financial reports to the State Controller. In fact, DHCS reported encountering significant challenges during its financial reporting, including that its procedures for completing bank reconciliations to FI$Cal were still under development.

The State Controller echoed these concerns in the fiscal year 2020–21 ACFR, published in March 2023, which noted that the transition to FI$Cal has affected financial reporting for several years but also included steps that the Controller is taking to improve financial reporting. The State Controller reported that it is collaborating with other state agencies to understand the root causes of delays and to develop mitigation strategies. The State Controller also explained that its own transition to the FI$Cal system remains underway and that its completion will lead to measurable advancements in financial reporting. Even so, an approved budget change proposal the State Controller submitted in January 2023 indicates that it anticipates only minimal annual improvements to its reporting timeline of between one and two months earlier each fiscal year. However, as of June 2023, the State Controller has indicated that it will seek to move the issuance date of the ACFR closer to its traditional deadline by three months for its reporting on fiscal year 2021–22.

The State has not made sufficient progress in resolving the problem of its late financial reporting to justify our removing this issue from the high-risk list. Financial reporting remains late, meaning there is no change in circumstances, and the State’s planned corrective actions are still in process. Moreover, state law requires the State Auditor to evaluate both the State Controller’s and the Department of FI$Cal’s efforts to implement the system. The result of this statutory audit work will likely further inform our future designations of this issue as an area of high risk.

Status: Retained on high-risk list

FI$Cal's response, Finance's response, State Auditor's comments to FI$Cal, and State Auditor's comments to Finance

The State’s Information Security Remains a High-Risk Issue

Background

Information security is the protection of the confidentiality, integrity, and availability of the State’s information assets, including data, processing capabilities, and information technology (IT) infrastructure. State law generally requires state entities that are under the Governor’s direct authority (reporting entities) to comply with the information security practices that the California Department of Technology (CDT) prescribes and to report annually to CDT on compliance with these practices. However, state law exempts entities that fall outside of the Governor’s direct authority (nonreporting entities), such as constitutional offices and those in the judicial branch, from following CDT policies and procedures.

We first identified information security as a high-risk issue in Report 2013-601, September 2013, when we concluded that CDT was performing limited reviews of the security controls that reporting entities had implemented. In a subsequent high-risk audit, Report 2015-611, August 2015, we noted that many reporting entities had poor controls over their information systems. In our state high-risk assessment, Report 2017-601, January 2018, we reported that CDT had made improvements to its oversight but that reporting entities still showed significant room for improvement. Finally, in Report 2021-601, August 2021, we reported that a federally‑sponsored nationwide security review noted that state entities in California self-reported ratings below the federally recommended minimum level.

Report 2022-114, April 2023, reiterated many of our previous concerns with the State’s information security. Our audit found weaknesses in CDT’s strategic planning, oversight of information security and IT projects, and that CDT has not ensured that the State’s IT systems are adequately protected from cyberattacks. This inadequate protection has the potential to compromise individuals’ identities, shut down critical government functions, and cost the State millions of dollars to remedy.

Assessment

CDT has not sufficiently improved its oversight of information security to mitigate the risks we have identified; therefore, this issue will remain on the state high-risk list. CDT is responsible for providing direction for the State’s information security efforts and for reviewing the security of reporting entities. However, CDT has yet to determine the effectiveness of cybersecurity programs for all of the entities for which it has oversight responsibility. To determine the effectiveness of information security for reporting entities at higher risk, CDT relies on a four-year oversight lifecycle. This process generally includes a compliance audit, a follow-up review, and two technical assessments. However, as we said in Report 2022-114, April 2023, CDT has the capacity to complete only 13 compliance audits each year, which equates to only 52 reviews of reporting entities during a four-year cycle, or not quite half of the 107 reporting entities for which it is responsible.

To prioritize its compliance audits, CDT uses a risk-based methodology to determine the 52 entities it has the capacity to audit. However, we are concerned about CDT’s limited capacity. Our previous audits have recommended that CDT increase its capacity to conduct its IT audits by hiring more staff or contracting for additional audit support. In March 2023, the Legislative Analyst’s Office raised a similar concern about limited capacity, noting that resolving staffing-related issues in information security is important if state entities are to improve their information security compliance and maturity. However, CDT explained that it does not have any immediate plans to hire additional staff or contractors. Instead, CDT reports that it hopes to find increased efficiencies through a new IT system, which does not currently exist, that would allow CDT to more efficiently conduct its audits.

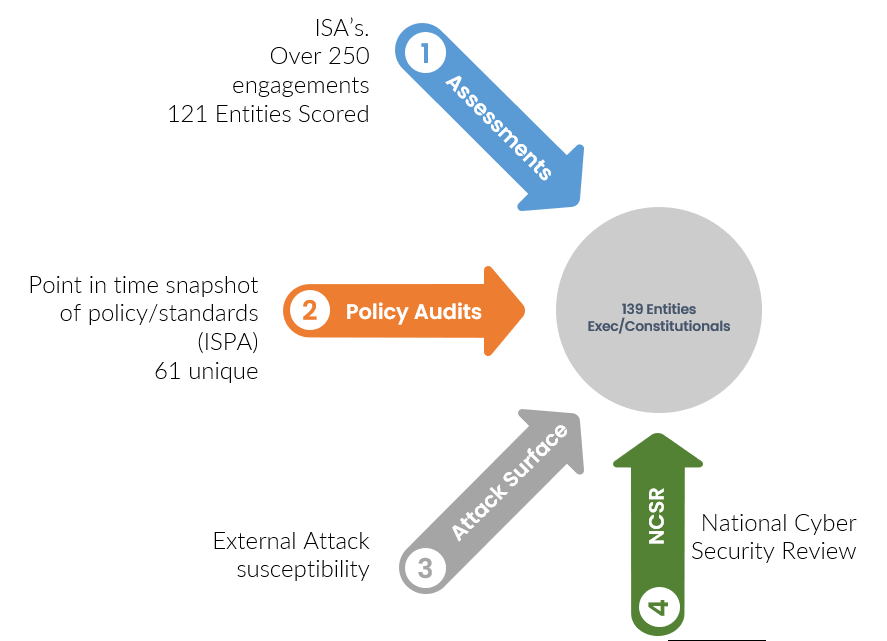

In addition, most nonreporting entities are also lagging behind in information security. We evaluated nonreporting entities’ compliance with their selected security standards in 2021. As Figure 1 illustrates, we surveyed 32 nonreporting entities for Report 2021-601, August 2021, and found that although 29 had adopted information security frameworks or standards, only four reported achieving full compliance.

Legislation that went into effect in January 2023 implemented our recommendation to improve the security of nonreporting entities. Nonreporting entities are now required to perform a comprehensive, independent security assessment every two years and to certify their compliance with certain security requirements annually. We will continue to monitor reporting and nonreporting entities’ efforts to improve their security; however, information security continues to present a significant risk to the State.

Figure 1

In 2021 Most Nonreporting Entities Stated That They Were Only Partially Compliant With Their Selected Security Standards

Source: Analysis of survey responses, Report 2021-601, August 2021.

Figure 1 description:

A pie chart shows 32 nonreporting entities by their compliance status with their selected security standards. The chart shows that three entities reported having not adopted framework or standards, 19 entities reported partially complying, and four entities reported having fully complied with all of their selected security standards.

Vulnerabilities in the State’s information security practices can have costly effects on the efficiency and effectiveness of State programs and can affect the privacy of Californians’ data. For example, in December 2022, the Department of Finance fell victim to a cyberattack that was widely reported in the media. In 2021 an employee at the State Controller’s Office unknowingly interacted with a malicious link that appeared to come from a trusted source, thereby providing a hacker with such confidential information as the names, Social Security numbers, and birth dates of state employees. Further, in 2023 data maintained by a CalPERS and CalSTRS contractor was breached, resulting in unauthorized access to confidential information related to retirees and their family members. It is likely that attempts against governmental information assets will only increase in the future. CDT has reported that in the wake of the pandemic, the cybersecurity threat nearly quadrupled in the sophistication of attacks by nation-state adversaries and criminal organizations.

Because cybersecurity threats are significant and oversight of state departments and agencies remains inadequate, we will retain this issue on the high-risk list. The State continues to need improvements in its cybersecurity practices, and although state entities are giving increasing attention to cybersecurity, they have not substantially mitigated the ongoing risk from inadequate information security technology practices. Finally, additional audit work by the State Auditor could assist in mitigating the risk presented by this issue area. For example, the State Auditor could continue to audit CDT and other entities as necessary to determine their compliance with state law and best practices related to cybersecurity.

Status: Retained on the high-risk list

CDT's response and State Auditor's comments

CDT Has Not Made Sufficient Progress in Its Oversight of State Information Technology Projects

Background

The California Department of Technology (CDT) is responsible for approving, overseeing, and monitoring the State’s IT projects. As a component of this effort, CDT regularly reports on the progress of various projects as measured against their objectives, scope, schedule, and cost. Historically, the State has faced challenges in completing IT projects on time and within budget. Currently, CDT uses a four-stage process known as Project Approval Lifecycle (PAL), that is intended to ensure that larger projects—those anticipated to cost more than $5 million—include a strong business case, clear objectives, accurate costs, and realistic schedules. CDT’s goal in using PAL is to improve the quality, value, and likelihood of success for IT projects in California government.

We designated CDT’s oversight of IT projects as high-risk in our initial high‑risk assessment Report 2006-601, May 2007, because of the number of costly and complex projects that were underway and the State’s history of failed IT projects. In part to address these concerns, CDT implemented PAL in 2016. However, our state high-risk assessment, Report 2021-601, August 2021, found PAL’s effectiveness to be unclear since a sufficient number of projects—especially highly complex, and critical projects—had not been completed using PAL. We further noted in our Report 2022‑114, April 2023, that CDT will require new metrics to better track its effectiveness as it uses PAL to support more complex and critical projects.

Assessment

CDT’s oversight of IT projects has yet to demonstrate significant improvement and will therefore remain on the state high-risk list. In Report 2022-114, April 2023, we noted that CDT’s oversight of IT projects has been ineffective at addressing risks on complex projects. During that audit, we reviewed CDT’s oversight of four IT projects and found that although CDT identified deficiencies in three which required immediate corrective action, it had not used its authority to ensure that the problems were resolved.

Moreover, CDT’s use of costly and lengthy approval processes can have negative consequences for agencies. As part of Report 2022-114, April 2023, we surveyed 143 agencies on their experience using the PAL process. Among the many agencies that had used CDT’s project approval processes—63 of those we surveyed—23 percent of those agencies were unsatisfied or very unsatisfied with the project approval process. Several agencies noted that the PAL process is too lengthy and that it delays the approval of projects. Timelines that stretch into multiple years can be costly to agencies and can delay updates to critical IT systems. PAL remains a lengthy process for agencies in 2023, and CDT has not clearly demonstrated its effectiveness.

CDT has not made sufficient progress in resolving issues with its oversight of IT projects to justify its removal from the high-risk list. CDT’s oversight process has been ineffective in addressing previously identified problems and CDT’s process is lengthy, leading to delays; thus, circumstances have not changed substantially. Further, CDT needs to better measure its process to assess its effectiveness; thus, adequate corrective action has not occurred. Finally, additional audit work by the State Auditor could follow up on Report 2022-114, April 2023, to assess CDT’s progress in implementing our recommendations, and generate new recommendations.

Status: Retained on the high-risk list

CDT's response and State Auditor's comments

Climate Change and Aging Water Infrastructure Threaten California’s Water Supply and Public Safety

Background

We added the State’s water infrastructure as a high-risk issue in Report 2013-601, September 2013, noting that the State’s investment in water infrastructure had not kept pace with its needs and was aging. After the near-failure of the Oroville Dam spillway in 2017, we expanded this issue area in Report 2017-601, January 2018, to include dam safety. In our most recent high-risk assessment in Report 2021-601, August 2021, we noted that the State had not made appreciable progress toward addressing deficiencies in its water infrastructure and that safety planning for dams throughout the State remained incomplete.

Much of the State’s water storage is held in surface water, specifically in lakes behind dams. State law vests authority over dams in the State’s jurisdiction with the Department of Water Resources (Water Resources), a department in the California Natural Resources Agency (Natural Resources). Water Resources oversees these dams through its Division of Safety of Dams (Dam Safety Division), which inspects more than 1,200 dams, rates each dam’s condition as Satisfactory, Fair, Poor, or Unsatisfactory, and identifies the downstream hazard that the dam poses, which can range from Low to Extremely High. Condition rating assesses a dam’s physical condition; the downstream hazard rating assesses the impact if the dam fails.

After the Oroville Dam spillway incident in 2017, the Legislature amended state law to require that owners of state-regulated dams with certain levels of downstream hazard develop emergency action plans (emergency plans) to address the potential loss of life and potential property damage of a dam failure. Each emergency plan must include one or more inundation maps, which illustrate the potential flooding that may result from a dam’s failure. The California Governor’s Office of Emergency Services (Emergency Services) is responsible for approving emergency plans, and the Dam Safety Division is responsible for approving inundation maps, which are a component of every plan.

In our high-risk assessment Report 2021-601, August 2021, we focused our review of the sufficiency of California’s water supply by reviewing the progress of a project known as WaterFix, which is no longer proceeding. Our current review focuses in part on a new effort known as the Delta Conveyance Project which would develop new water infrastructure facilities in the Sacramento–San Joaquin Delta (Delta). The Delta Conveyance Project is intended to protect and preserve California’s water supply threatened by sea level rise, climate change, and seismic activity. The Delta Conveyance Project remains a component of Natural Resources’ greater water supply strategy. However, given California’s changing climate and the strategic planning that Water Resources and other agencies completed since our last review, we have expanded our current high-risk assessment to include a review of the State’s water strategies to ensure water availability and a review of certain levees under water infrastructure safety.

Assessment—Water Availability

The State has not yet made sufficient progress in addressing the water availability issue area; therefore, it will remain a high-risk issue. Natural Resources estimates that hotter, drier weather could diminish the State’s existing water supply by up to 10 percent by 2040. With the State consuming between 60 and 90 million acre feet per year, this estimated 10 percent loss due to hotter, drier weather would mean 6 to 9 million acre-feet of water less per year in 2040. However, our limited water supply is already affecting many Californians. For example, although more than a million Californians rely on domestic well water, nearly 2,000 wells were reported dry as of May 2022.

California has recently experienced cycles of drought and water overabundance. For example, California’s $50 billion annual agriculture industry, which employs more than 420,000 people, has felt the effects of repeated droughts. In 2022 the Public Policy Institute of California estimated the economic impact of the 2021 drought at $1.7 billion and 14,600 jobs lost. By contrast, the State experienced record rainfall in 2023, which resulted in the State Water Project’s allocating 100 percent of the planned delivery to water contractors in 2023, whereas in 2021 and 2022, it was able to allocate just 5 percent of the water requested.

This drought-and-flood cycle also affects other elements of the State’s water infrastructure, such as its levees. Specifically, according to California’s Delta Stewardship Council, flooding in the Delta could result in loss of life and property losses in the billions of dollars. Moreover, the probability of a levee failure caused by high water levels is substantial based on historical performance. In the last century, there have been more than 140 levee failures and island inundations in the Delta. Ensuring reliable and safe water supplies is critical for the well-being of people, businesses, and communities throughout California.

The State is working to address these needs; however, progress remains slow. For example, Water Resources is in the process of completing an environmental review for the Delta Conveyance Project. The purpose of the Delta Conveyance Project is to modernize and protect the reliability of State Water Project water deliveries south of the Delta to help mitigate the effects of sea level rise, climate change, and seismic risk. The State Water Project provides clean, affordable drinking water to 27 million Californians and irrigation supplies to 750,000 acres of farmland. However, the Delta Conveyance Project is in a planning phase, and may face future challenges related to funding and the timeline for its completion. Water Resources states that it is on schedule to complete an environmental impact review by the end of 2023. It also states that permitting activities are underway or slated to begin soon. The Delta Conveyance Project is estimated to cost about $16 billion in total and, according to Water Resources, construction will likely begin in 2028 or 2029. While the Governor has recently signed legislation that would streamline various processes related to the environmental impact of specified infrastructure projects, the Delta Conveyance Project was explicitly exempted from these changes.

In addition to its work on the Delta Conveyance Project, the State has taken another important step in addressing its water needs since our last review. In August 2022, a variety of state agencies working cooperatively created a strategic water supply plan to help California adapt to its hotter, drier future.The agencies involved in the strategic plan are the California Natural Resources Agency, the State Water Resources Control Board, the California Environmental Protection Agency, the Department of Food and Agriculture, and the Department of Water Resources. This strategic plan calls for the creation of additional storage space for up to 4 million acre-feet of water to assist California in capitalizing on large storms when they occur. The plan also calls for increased water recycling, more efficient water use and conservation, and other methods that diversify the State’s response to climate change. The plan also specifies a variety of steps to meet these goals, such as expanding both desalination production and existing reservoirs. Although the strategic water supply plan is too recent to assess its effects, the plan notes that the State has supported related projects with budgetary increases of more than $8 billion earmarked for water infrastructure modernization and management. We will monitor the strategic water supply plan’s application and the use of related funding to determine its effects on California’s water resources over time.

Given the current risks and limited progress, the availability of water resources will remain a high-risk issue. The State’s cycle of ongoing drought and flood, as well as the still-pending Delta Conveyance Project and newly created strategic water supply plan for additional water storage, show that circumstances have not changed substantially and that water availability continues to be a high-risk issue. Finally, additional audit work by the State Auditor could assist in mitigating the risk presented by this issue area by proposing methods to streamline project management at the responsible agencies, as we did in Report 2016-132, October 2017, our audit of the WaterFix project. Such additional audit work could examine the State’s progress and barriers toward enhancing water storage, increasing recycling, and expanding desalination.

Status: Retained on high-risk list

California Natural Resources Agency’s response

Assessment—Water Infrastructure Safety

The condition of some of the State’s potentially most hazardous dams and related emergency planning remains a high-risk issue. Failures or incidents at dams could result in significant harm to the State and its residents, through loss of life and flooding of economically important areas. Nevertheless as of June 2023, 88 dams throughout the State have both a condition rating lower than Satisfactory and a downstream hazard rating of Significant or higher. Dams that fall within these classifications have a combined reservoir capacity of more than 7 million acre‑feet of water. Of particular concern, 37 of the 88 dams with condition ratings below Satisfactory are also rated as Extremely High Hazard, meaning that a dam failure would cause considerable loss of human life and significant economic loss. Water Resources indicates that since 2021, 11 dams have received some repairs and that the department has also identified numerous additional deficiencies. The State’s new strategic water supply plan indicates that Water Resources will administer $100 million in new funding for local dam safety projects and flood management, such as improving dam condition ratings. We look forward to assessing the impact this funding has on the issue area.

Since our August 2021 high-risk assessment, Water Resources has made significant progress in approving inundation maps, having approved maps for 805 dams, or 93 percent of the required inundation maps, an increase of more than 13 percentage points. However, Emergency Services’ approval of emergency plans lags behind. Emergency Services has only approved emergency plans—which outline action to be taken during an emergency to minimize or eliminate the potential for loss of life and property damage—for 419 of the nearly 900 dams required to submit such plans, or about 48 percent. Although this number represents progress—an increase from the 107 approved plans in 2021—it will take several years at the current rate of approval for the State to have clear emergency plans in place for all dams that require them. Further, there are 121 dams without approved emergency plans that Water Resources has assessed as having Extremely High downstream hazard ratings, indicating a risk of considerable loss of human life.

In addition to dams, other elements of water infrastructure, such as levees, are also of concern. Levees face serious threats—from storm surges, sea level rise, and earthquakes—that could cause their failure. Water Resources inspects and reports on observable conditions on certain levees and reviews the status of maintenance practices to ensure that local entities are meeting their legal obligations.Water Resources annually inspects Central Valley levees within the State Plan of Flood Control. Results from Water Resources’ 2022 levee maintenance inspections indicated that local agencies’ maintenance of levees had worsened slightly from the previous year. Water Resources reported that 38 of 106 geographical areas received Unacceptable maintenance ratings, and 33 areas received Minimally Acceptable maintenance ratings. A rating of Unacceptable means that one or more deficient conditions exist that may prevent the project from functioning as designed, intended, or required. A Minimally Acceptable rating means that one or more conditions exist in the flood protection project that needs to be improved or corrected.

Maintenance for levees and flood control is generally conducted by levee districts, reclamation districts, or other public agencies.Eighty-four separate Local Management Agencies (LMAs) covering 106 areas within the Sacramento and San Joaquin River watersheds are responsible for the maintenance of levees and other flood protection works. However, Water Resources inspects levee maintenance for certain levees, and a potential failure of California’s flood control system poses a risk to the State. For example, in 2017 and 2019, many levees sustained storm damage. The State responded by developing a rehabilitation program that, in combination with United State Army Corps of Engineers’ efforts, expedited repair on 105 damaged sites, with 21 remaining to be completed.

Because of the current high risks presented and the inadequate progress to mitigate those risks, the State’s water infrastructure will remain a high-risk issue. The significant number of high-hazard dams with condition ratings below Satisfactory shows that circumstances have not changed substantially enough to meet the requirements of our regulations. Further, the high number of emergency plans yet to be approved by Emergency Services shows that significant corrective action has not yet occurred. Finally, audit work by the State Auditor could assist efforts in mitigating the risk presented by this issue area by examining the State’s process for inspecting dams and approving emergency plans.

Status: Retained on high-risk list

CalOES' response, California Natural Resources Agency's response, and State Auditor's comments

Health Care Services Has Not Adequately Addressed Issues With Medi-Cal Eligibility, But It Has Made Improvements to Its MHSA Oversight

Background

The Department of Health Care Services (Health Care Services) is responsible for overseeing the State’s implementation of the federal Medicaid program, known in California as Medi-Cal. Medi-Cal provides comprehensive health services—including preventive, routine, and emergency care—for eligible residents such as low‑income children, pregnant women, and families, and elderly or disabled individuals. As part of this responsibility, Health Care Services is responsible for ensuring that counties’ determinations of eligibility for applicants are appropriate and completed in a timely manner. Health Care Services’ role is pivotal because erroneous determinations of eligibility result in inappropriate expenditures or in residents’ inability to access needed services.

Our office previously issued Report 2018-603, October 2018, and Report 2019‑002, October 2020, which both identified discrepancies between state and county Medi‑Cal eligibility systems resulting in at least $4 billion in questionable payments. We also found that Health Care Services had not implemented the controls or processes necessary to ensure that problems with Medi‑Cal eligibility are corrected, a process for monitoring county welfare agencies’ progress in addressing eligibility discrepancy alerts. In Report 2020-613, July 2021, we reported that despite the COVID-19 public health emergency, Health Care Services could still do more to address chronic Medi-Cal eligibility problems. In our most recent state high-risk assessment, Report 2021-601, August 2021, we reported that Health Care Services remained a high-risk agency, because it had not corrected discrepancies in its Medi‑Cal eligibility system that had resulted from suspended efforts during the COVID-19 public health emergency and that the problem had continued to grow.

Additionally, since 2012 Health Care Services has been responsible for overseeing various aspects of the Mental Health Services Act (MHSA). In 2004 voters enacted the MHSA, which expanded services and treatment for those who suffer from or are at risk of serious mental illness, and is funded by a 1 percent income tax on personal income in excess of $1 million per year. We have included Health Care Services’ oversight of the MHSA on our state high-risk list since 2007 and have performed two audits related to the MHSA. In Report 2012-122, August 2013, we identified deficiencies in state oversight of the implementation of MHSA funding, including county programs’ inadequate collection of the data necessary to determine the effectiveness of MHSA funds. In Report 2017-117, February 2018, we noted that, despite having had responsibility for the MHSA since 2012, Health Care Services had not developed a process to recover unspent MHSA funds from local mental health agencies. As a result, local agencies had amassed hundreds of millions of dollars in unspent MHSA funds that should otherwise have been reallocated to other local mental health agencies, a process called reversion. We recommended that Health Care Services develop guidance for counties on administering their MHSA programs.

Assessment—Medi-Cal Eligibility

Although it has made some progress, Health Care Services has not adequately resolved issues involving Medi‑Cal eligibility. In Report 2020-613, July 2021, we found that the number of eligibility discrepancies between state and county eligibility systems increased during the COVID‑19 pandemic and that Health Care Services was not doing enough to resolve eligibility questions about Medi‑Cal beneficiaries. Health Care Services began taking steps in June 2022 to address eligibility discrepancies by issuing guidance to counties on case processing actions after the May 11, 2023, termination of the public health emergency. Health Care Services is developing additional guidance on the prioritization of resolving high-risk eligibility issues and will be monitoring counties’ efforts through its oversight program, which it plans to launch statewide in May 2024. However, to allow counties to complete public health emergency wind-down activities, Health Care Services does not expect to fully implement our July 2021 recommendations regarding eligibility discrepancies until June 2024.

Although Health Care Services is positioning itself to make progress on this issue, we lack assurance that it has resolved issues related to Medi-Cal beneficiary eligibility. Because of the current risks presented and the lack of demonstrated progress, Health Care Services’ management of Medi-Cal benefits will remain a high-risk issue. Finally, audit work by the State Auditor could assist in mitigating the risk presented by this issue area by following up on recommendations from our prior audits, assessing Health Care Services’ progress in addressing ineligible Medi-Cal recipients, and potentially providing further recommendations.

Status: Retained on high-risk list

Assessment—MHSA

In 2017 the State enacted Assembly Bill 114 to provide counties with a second opportunity to use certain MHSA funds. The amended state law provided that funds subject to reversion as of July 1, 2017, were deemed reverted to the State and reallocated to the county of origin for their originally designated purposes. This effectively provided counties with additional time to spend previously allocated funds. The Legislature also gave small counties—those with fewer than 200,000 residents—two extra years to spend their MHSA funds.

We retained this issue on our high-risk list in August 2021 because Health Care Services had not implemented a sufficient number of our recommendations surrounding this issue to mitigate its risk. However, since that last assessment, Health Care Services has made progress in this area. The department had previously created regulations to improve reporting related to unspent MHSA funds that were subject to reversion. The department reports that it now makes these determinations according to amounts reported by counties in their Annual MHSA Revenue and Expenditure Reports. Health Care Services communicated this process to counties, letting them know that they must generally spend funds allocated to Community Services and Supports, Prevention and Early Intervention, and Innovation components within three fiscal years. In addition, Health Care Services informed counties that they must spend funds allocated to Capital Facilities, Technological Needs, and Workforce Education and Training components within 10 fiscal years.

Our review of submitted MHSA Revenue and Expenditure Reports shows that counties are now using the majority of their MHSA funds within the required timelines. In fiscal year 2021–22, about $5.4 billion was deposited into the MHSA Fund according to the 2023–24 Governor’s budget, and MHSA expenditures amounted to $6.5 billion in that fiscal year. In addition, Health Care Services estimated that $3.5 and $3.4 billion would be deposited into the Mental Health Services fund in fiscal years 2022–23 and 2023–24 respectively and $3.6 and $3.4 billion would be spent in those years. Counties therefore now appear to be spending MHSA funds promptly.

Health Care Services has now fully or partially implemented ten of 11 recommendations from Report 2012-122, August 2013, and six of seven recommendations from Report 2017-117, February 2018. For example, Health Care Services retained a contractor who has provided training and technical assistance to counties.

Although the risk to the State and its residents is serious if Health Care Services mismanages the MHSA, recent legislative changes, combined with the department’s progress in implementing outstanding recommendations, demonstrate that the agency has made sufficient progress toward eliminating the basis upon which we determined that oversight of MHSA funds was high-risk. Therefore, additional audits conducted by the State Auditor would be unlikely to assist in mitigating risks associated with MHSA funds. Accordingly, we are removing Health Care Services’ oversight of the MHSA as a high-risk issue.

Status: Removed from the high-risk list

Removed High-Risk Agencies and Issues:

CSU and UC Have Made Efforts to Control Tuition and Fees in the Past Decade

Background

We first identified the affordability of higher education as a state high-risk issue in Report 2013-604, December 2013, noting challenges associated with the funding of higher education and the extent of access it provided. In 1960 the State published A Master Plan for Higher Education in California, which provided a roadmap for the future of higher education in the State. Reviews of the plan have reaffirmed its principles and emphasized the need for improved access to affordable higher education. As components of the State’s public higher education system, the University of California (UC), the California State University (CSU), and the California Community Colleges (CCC) each have a responsibility to align its services with the State’s goal of making higher education accessible and affordable to every Californian. However, in 2010 the Legislature identified the ability of the State’s public system of higher education to carry out the master plan as being at risk because of unprecedented population growth and extraordinary social and economic changes.

Although we originally included the CCC as part of this high-risk issue, we removed it in Report 2017-601, January 2018, because it had improved its ability to provide courses and services to students. In Report 2019-601, January 2020, we reported that from 1992 to 2017, undergraduate tuition had increased by about 340 percent at the CSU and 440 percent at UC. In our state high-risk assessment Report 2021‑601, August 2021, we noted that issues related to the affordability of higher education persisted.

Assessment

By taking steps to control tuition and fee increases, the CSU and UC have made sufficient progress toward eliminating the basis on which the State Auditor designated this issue high-risk. For example, both university systems have held their tuition relatively flat since 2013. The CSU did not increase tuition during that time, and UC increased its tuition only two times, once by 3 percent in academic year 2017–18 and once by 4 percent in academic year 2022–23. As of academic year 2022–23, the CSU’s annual tuition is $5,742 and UC’s is $11,982. Similarly, both universities raised their fees moderately. Since 2018 the CSU increased its systemwide fees by $222 and UC increased its systemwide fees by $184.

With support from the State, the CSU and UC were able to avoid significant tuition and fee increases, even as inflation increased by 1.2 percent to 8 percent annually over a five year period. If the two institutions’ tuition had kept pace with inflation during these years, the CSU’s academic year 2022–23 tuition would have been $6,850 and UC’s would have been $13,649. A recent report recommended that the CSU increase its tuition in predictable amounts because of growing costs and insufficient funding from the State to cover its expenditures. In July 2023, the interim chancellor recommended a multiyear tuition proposal that would raise tuition rates by 6 percent beginning in academic year 2024–25, with one-third of the increase dedicated to financial aid. However, the CSU has not yet adopted this initial proposal. UC approved a tuition stability plan that took effect in 2022. The plan allows for the adjustment of tuition for each incoming undergraduate class at a rate slightly above inflation but subsequently holds the tuition rate flat for that class for up to six years.

Financial aid programs also increase access to higher education and have remained a viable option for the majority of resident students in both systems. For the most recent reporting period—academic year 2021–22—a variety of financial aid programs allowed nearly 60 percent of undergraduate students to pay reduced tuition at the CSU. Likewise, student aid allowed 55 percent of UC undergraduate students to pay no tuition. The university systems reported that in 2021–22, nearly 82 percent of CSU undergraduate students received some form of financial assistance, and 70 percent of UC undergraduate students received grants and scholarships.

The CSU and UC have attempted to address other expenses related to attending college that have increased in the past decade. The costs of housing, food, transportation, books, child care, health care, and supplies contribute to the overall cost of higher education. The CSU reports that the average cost of food and housing for its undergraduate students increased between about 3 percent to 6 percent annually from academic years 2018–19 to 2023–24. The average cost of living, which includes food and housing, increased by a total of 12 percent for UC’s undergraduate students during the same period.

Although expenses other than tuition and fees account for about 66 percent of the total cost of attending the CSU and 60 percent of the cost of attending UC, they are often beyond the university systems’ control. However, to help alleviate food and housing insecurity for students, the Legislature appropriated $15 million per year from 2019 through 2022 for UC and between $6.5 million to $31.5 million per year during the same period for CSU. Both university systems have used these funds to offer a wide range of services. For example, both the CSU and UC offer food pantry and food distribution programs, meal voucher programs, CalFresh application assistance, and multiple emergency housing programs.

Although the affordability of higher education continues to be a concern for many Californians, the CSU and UC have slowed the rate of tuition and fee increases in the past decade relative to inflation. Both university systems have also made attempts to mitigate other barriers to higher education—such as costs associated with food and housing—that are often beyond their direct control. Given these ongoing efforts, it is unlikely that a high-risk audit of higher education expenses would result in recommendations leading to a significant reduction in tuition, fees, or other costs such as food and housing.

Status: Removed from the high-risk list

California State University Office of the Chancellor response. The UC did not provide a response.

CalSTRS Has Implemented Corrective Action to Decrease the Risk Posed by Its Unfunded Liability

Background

The California State Teachers’ Retirement System (CalSTRS) provides retirement, disability, and survivor benefits to the State’s more than 1 million public school educators and their families, primarily through a defined benefit pension plan (benefit plan). CalSTRS uses the funding it receives from its members, their employers, and the State to generate investment income, which it uses to help pay retirement benefits. Pension funds operate on a long-term horizon, working to guarantee benefit payments for existing and future retirees. According to CalSTRS, the most financially prudent way to provide such benefits is to fund the benefit plan fully by maintaining sufficient assets to cover all payments the program is obligated to make.