City of Montebello

Although It Is Making Positive Changes, It Remains at High Risk Because of Recent Declines in Its Financial Condition

October 14, 2021

2021-807

The Governor of California

President pro Tempore of the Senate

Speaker of the Assembly

State Capitol

Sacramento, California 95814

Dear Governor and Legislative Leaders:

This follow-up audit report provides an update on the city of Montebello's efforts to address the concerns from our December 2018 report that determined Montebello is a high-risk city because of significant financial and operational risks.

This report concludes that Montebello continues to face challenges related to its financial stability. Montebello's financial situation grew worse in fiscal year 2019–20, spending nearly $11 million more from its general fund than it received in revenue. Moreover, in August 2021, we updated our local high-risk dashboard, which measures the fiscal health of California cities, and determined that in fiscal year 2019–20 Montebello was one of California's 10 cities at greatest risk of financial distress. Montebello currently projects that its fiscal situation will improve, partly due to a new voter-approved sales tax, but it will need to continue to ensure that its spending aligns with revenues.

Though Montebello has attempted to improve its operations in multiple areas since the 2018 audit, such as by updating competitive bidding requirements in its municipal code and improving its golf course operations, we identified continued operational deficiencies related to the management of city-owned hotels and its procurement processes. In one instance, Montebello likely violated state open meeting laws when the city council approved a loan to pay for upgrading one of its hotels without properly notifying the public in advance. Further, Montebello did not always adhere to competitive bidding requirements in its municipal code, and we identified purchases for which city staff did not follow the city's new petty cash and credit card policies and likely violated state law prohibiting the gift of public funds.

To address these concerns, we present several recommendations in this report, such as ensuring that city council agendas include all matters of fiscal policy that the city council will consider in public sessions, and creating a policy to formally document situations where a valid reason exists for staff to deviate from procurement requirements in Montebello's municipal code, when allowed to do so.

Respectfully submitted,

ELAINE M. HOWLE, CPA

California State Auditor

HIGH RISK ISSUES—Follow-Up Audit

| ISSUE | |

|---|---|

| Despite Progress in Some Areas, Montebello's Financial Stability Remains Uncertain | |

| Montebello's Financial Situation Declined in Fiscal Year 2019–20, but It Projects Improvement Over the Next Few Years | |

| Montebello Has Taken Steps to Improve Its Golf Course Operations but Has Yet to Determine the Full Financial Impact of Its Planned Actions | |

| The City Has Resolved Our Previous Concerns About Its Retirement Costs, Although Its Approach Has Created Ongoing Risk | |

| Montebello Continues to Make Questionable Decisions Related to Its Hotels | |

| City Staff Have Not Provided the City Council With Analysis of the Performance of City‑Owned Hotels | |

| The City Council Approved a Multimillion-Dollar Loan for Hotel Renovations Without Properly Including It on a Council Agenda | |

| Montebello Has Not Adopted a Policy to Ensure Its Payment of Hotel Management Fees | |

| Montebello Has Not Fully Resolved Problems With Its Procurement Processes | |

| Montebello Has Not Followed Competitive Bidding Processes That Could Ensure That It Receives the Best Value When Procuring Services | |

| Although Montebello Implemented Petty Cash and Credit Card Policies, Its Staff Members Have Not Consistently Followed Them | |

| Montebello Is Making Progress in Addressing Its Low Salaries | |

| Appendices | |

| Appendix A—Scope, Methodology, and the Status of 2018 Risk Areas | |

| Appendix B—The State Auditor's Local High-Risk Program | |

| Agency Response | |

| City of Montebello | |

| California State Auditor's Comments on the Response From the City of Montebello | |

Risks the City of Montebello Faces

In December 2018, we issued an audit report titled City of Montebello: Its Structural Deficit and Poor Operational Processes Threaten the City's Financial Stability and Delivery of Public Services, Report 2018-802. In that report, we concluded that concerns related to Montebello's business activities and retirement costs, its lax oversight of the two hotels it owns, and its poor contracting and staffing put it at high risk for waste, fraud, abuse, and mismanagement. As we describe in Appendix B, state law requires that we issue an audit report at least once every three years with recommendations for improvement when we designate a city as high risk. In this follow-up audit, we found that although the city has made progress in addressing our recommendations, it remains a high-risk city because of its financial decline during fiscal year 2019–20 and its continued operational deficiencies.

Montebello's financial situation grew worse in fiscal year 2019–20, the most recent year for which it has audited financial statements. The city ended that year having spent nearly $11 million more from its general fund than it received in revenue. In August 2021, when we updated our local high-risk dashboard, which measures more than 400 California cities according to 10 financial indicators, Montebello's ranking in terms of its risk of facing fiscal distress rose from 81st in fiscal year 2018–19 to 7th in fiscal year 2019–20. Although it currently projects improvements in its financial situation for fiscal years 2020–21 and 2021–22, it will need to leverage its new sources of revenue—including a new sales tax its residents recently approved—to achieve year-over-year financial stability.

Operationally, Montebello has made significant positive changes in the nearly three years since our December 2018 report. It hired a new, permanent city manager and a director of finance, and it substantially updated its municipal procurement codes in response to our audit. It has also taken actions to control its retirement costs, although one of the approaches it has taken—issuing bonds to address its pension liabilities—still has the potential to negatively affect its finances. Finally, it has begun planning to improve the golf facilities it owns, as we recommended during our previous audit.

Nonetheless, it still needs to improve its oversight of its hotels and its procurement practices, as well as its adherence to state requirements regarding public meetings and the use of public funds. For example, we identified an instance where Montebello likely violated state open meeting laws when the city council approved a loan to pay for upgrading one of its hotels without properly notifying the public in advance. Montebello also used public funds to purchase about $7,600 worth of gifts for its employees, which we think constitutes a gift of public funds. The California Constitution prohibits such gifts of public funds. After we brought this issue to Montebello's attention, city officials raised private funds to cover the cost of the gifts. We also identified poor adherence to competitive bidding requirements and to the petty cash and credit card policies the city developed following our 2018 audit. For example, we noted likely split transactions—where an individual or individuals make multiple small transactions in order to avoid procurement requirements on higher dollar amounts—in both petty cash and credit cards.

To help Montebello continue to address the risks we identified, we make multiple recommendations to the city, including the following:

- The city council should ensure that it includes on the council meeting agenda all matters of fiscal policy it will consider during a public session, as state law requires, and that it discusses these matters in the public forum.

- The city should revise its municipal code to prohibit the purchases of employee gifts with public funds.

- The city should create a policy by January 2022 requiring staff to formally document situations when a valid reason exists for deviating from procurement requirements in its municipal code, when the code allows it to do so.

- The city should update its credit card policy by January 2022 to prohibit splitting payments to avoid the transaction limits and to require city council approval for any transactions above the limits.

Agency's Proposed Corrective Action

The city agreed with most of our recommendations, although it disagreed with many of the findings supporting those recommendations. The city did not provide a corrective action plan; thus we expect it to submit one by December 13, 2021.

Despite Progress in Some Areas, Montebello's Financial Stability Remains Uncertain

Montebello's Financial Situation Declined in Fiscal Year 2019–20, but It Projects Improvement Over the Next Few Years

In our December 2018 audit, we found that the city had struggled to generate sufficient ongoing revenue to meet its expenses. Moreover, we determined that although the city was supporting its general fund through one‑time revenue sources, its retirement costs and business activities—such as its golf course—could prove to be a significant drain on its resources. Montebello's finances improved slightly in the years immediately following the 2018 audit. However, its financial situation then declined dramatically in fiscal year 2019–20, in part because of the economic repercussions of the COVID-19 pandemic (pandemic). Partly as a result of a new tax its voters recently passed, the city currently projects improvement in the upcoming years.

Montebello's most recent audited financial statements are from fiscal year 2019–20 and show that the city had total expenses across all of its funds of about $137 million. In that fiscal year, its spending exceeded its revenue: it finished that year with a $14.7 million operating deficit across all of its funds and a $10.8 million operating deficit in its general fund. As Figure 1 shows, this is a significant decline from its fiscal year 2018–19 general fund surplus of about $2.9 million.

Figure 1

Montebello Experienced a Significant Gap Between Revenue and Expenditures During Fiscal Year 2019–20, but Expects It to Narrow in Fiscal Year 2020–21

Source: Analysis of Montebello's audited financial statements from fiscal years 2017–18, 2018–19, and 2019–20, and unaudited city financial information for fiscal year 2020–21.

Its fiscal year 2019–20 deficits were the result of both a decline in revenue and an increase in spending. Its overall revenue decreased by about $3.5 million because of lower sales tax collections and reduced hotel occupancy, much of which the city attributes to the pandemic. The city also noted in its financial statements that it experienced a $1.5 million reduction in cannabis licensing revenue from fiscal year 2018–19. At the same time, Montebello's expenses increased by about $12 million, including a $7.5 million increase in its general fund expenditures. We identified no single reason for this increase; rather, the city's fiscal year 2019–20 financial statements demonstrate its struggle to balance its various spending priorities with its revenue leading up to and during the pandemic. For example, Montebello experienced costs related to issuing and beginning to pay interest on new bonds in late 2019 and 2020, as well as to increasing pension costs. As we discuss later in the report, Montebello used bond proceeds to supplement its pension plan in June 2020. Because this action occurred only days before the end of the fiscal year, it did not significantly reduce the fiscal year 2019–20 contributions Montebello needed to make to its pensions. Also, the action did not eliminate an additional amount the California Public Employees Retirement System (CalPERS) requires cities to contribute annually, that is calculated based on employee payroll data. The city's finance director explained that the bond issuance would significantly reduce pension costs going forward. The city also told us that adapting its administrative practices to COVID-19 was an unforeseen expense.

Because of Montebello's financial decline, our office identified it as one of California's cities that were at the greatest risk of fiscal distress during fiscal year 2019–20. In August 2021, we updated our local high‑risk dashboard based on our review of cities' fiscal year 2019–20 financial statements, the most recent available. As Table 1 shows, we identified key financial indicators related to savings and borrowing—general fund reserves, liquidity, and debt burden—in which Montebello was experiencing elevated risk compared to our previous assessment based on fiscal year 2018–19. The regression in these indicators led us to reclassify Montebello's overall financial risk from moderate to high, indicating an elevated risk of the city being unable to fund services for its residents.

Table 1

In Fiscal Year 2019–20, Montebello Was at High Risk of Fiscal Distress

| Local High-Risk Dashboard Risk Assessment by Fiscal Year | |||

|---|---|---|---|

| 2017–18 | 2018–19 | 2019–20 | |

| Overall Risk Rating | Moderate Risk |

Moderate Risk |

High Risk |

| General Fund Reserves | Moderate | Moderate | High |

| Debt Burden | High | Moderate | High |

| Liquidity | Low | Low | High |

| Revenue Trends | High | Moderate | Moderate |

| Pension Obligations | High | High | High |

| Pension Funding | High | High | Low |

| Pension Costs | Moderate | High | High |

| Future Pension Costs | High | Low | Low |

| Other Post-Employment Benefit (OPEB) Obligations | Low | Low | Low |

| OPEB Funding | High | High | High |

Source: Analysis based on Montebello's financial statements and CalPERS's actuarial reports.

Some of these increases in financial risk are tied to the city's fiscal year 2019–20 reserves. Its lower revenue and higher expenses depleted Montebello's general fund reserves, limiting its ability to respond to further revenue declines or expenditure growth and still maintain services. According to our local high-risk dashboard, Montebello was among the 20 cities with the lowest general fund reserves, relative to city expenditures, in fiscal year 2019–20. We also identified the city's liquidity level as high risk because the general fund's balance of cash and investments was low enough that the city might have difficulty paying the costs of providing services to residents. We further noted that the city's debt burden had become higher risk because its overall debt had increased.

Montebello's elevated risk levels in fiscal year 2019–20 demonstrate that its finances have continued to experience instability after our 2018 audit. However, we note that this analysis represents a specific moment in time during the early months of the pandemic, when many cities were experiencing financial turmoil. In contrast, Montebello's budgets for fiscal years 2020–21 and 2021–22 show that the city is predicting a rebound in its finances from the early days of the pandemic. In fact, the city's budget for fiscal year 2021–22 forecasts revenue growth and anticipates a slight general fund operating surplus. The city is also optimistic that funding from the federal American Rescue Plan Act of 2021—which our office calculated to be more than $16.5 million for Montebello's allocation—will provide it additional resources to meet infrastructure and operational needs. The fiscal year 2021–22 budget does not specifically allocate this federal funding, which the city expected to receive between May 2021 and May 2022. According to its fiscal year 2021–22 budget, the city has received at least half of the anticipated federal COVID relief funds. The city identified several potential uses for these funds, including recovery of previously lost revenue, sewer infrastructure upgrades, and information technology upgrades. According to the budget, this may help Montebello address unmet infrastructure needs and ultimately contribute to the city's financial stability. However, we have not received final financial information for fiscal year 2020–21 and thus cannot assess the city's projections.

One reason for this revenue growth is that the city has an important new funding source: in March 2020, city voters passed a sales tax measure, a step they had been unwilling to take in the past. The city reported that it collected about $7 million in fiscal year 2020–21 from this tax. However, the new sales tax will not necessarily solve all of Montebello's fiscal problems, as fiscal year 2019–20 showed that the city's spending can significantly exceed its revenue by a greater amount than the new tax will raise. Thus, it is important that Montebello continue to evaluate its spending and determine how to best align its expenditures with its revenue. Although Montebello is showing signs of progress in addressing its financial situation, we will continue to assess whether it can leverage new revenue and a stronger economy to achieve year-over-year financial stability.

Montebello Has Taken Steps to Improve Its Golf Course Operations but Has Yet to Determine the Full Financial Impact of Its Planned Actions

For decades, Montebello has owned and operated an 18-hole golf course. Our 2018 report noted that this course had historically required support from the city's general fund in order to operate. We recommended that the city consider recommendations from a consultant it had hired to improve the operations and fiscal self-sufficiency of the course and that it also consider alternative uses for the land. In early 2019, the city council considered and subsequently began to implement some of the consultant's recommendations, including a move to an online booking system. Montebello also entered into a new maintenance contract for the course and replaced its managing operator—developments that the city staff assert have helped strengthen the course's finances. Based on preliminary financial data, the city estimates that fiscal year 2020–21—the first full year under the new operator—will prove to have been one of the course's strongest years in recent history, with revenue about 40 percent higher than the prior year. This allows the city to reduce its general fund subsidy from $751,000 in fiscal year 2019–20 to about $471,000 in fiscal year 2020–21, a significant improvement.

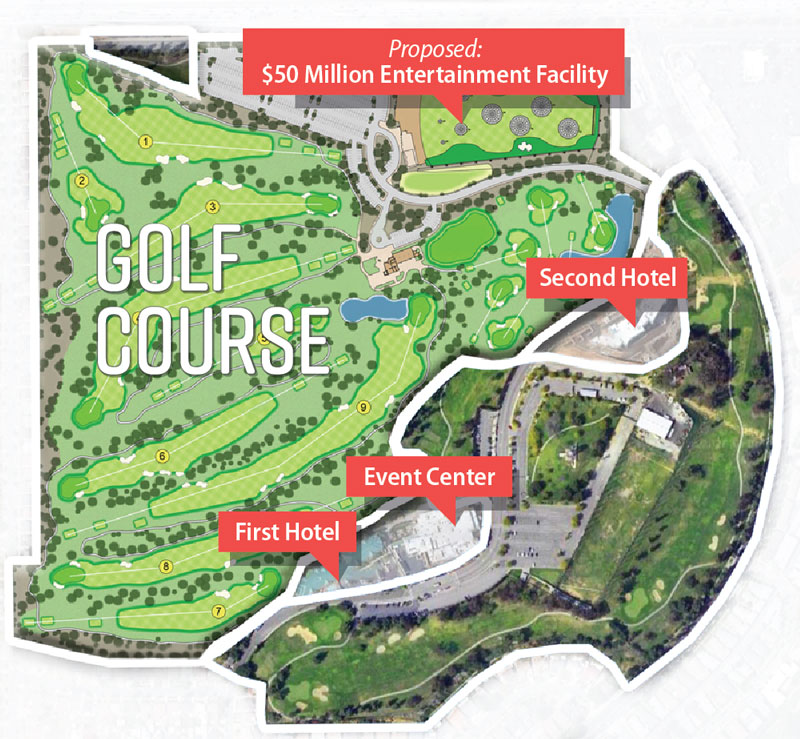

In addition, in March 2021, the city council approved a plan to build a driving range and entertainment facility on a portion of the golf course. Figure 2 shows the location of the planned facility. The city intends to fund this construction by selling up to $50 million in bonds that it will repay over 20 years. To facilitate this plan, the city entered into an agreement with a sports entertainment company, which—once the range and facility are operational—will annually pay the city an amount equal to the city's debt service for the bonds. In addition, beginning during the second year of the range and facility's operations, the sports entertainment company will pay the city increasing annual rent payments that will start at $375,000 in Year 2, reach $1.5 million by Year 5, and exceed $1.7 million by Year 20. The rent revenue that will result from this contract—as well as sales taxes on facility concessions—should be greater than the typical annual golf course deficits, and we estimate that the payments could help the course pay back the nearly $2 million it owes the city's general fund by 2030.

Figure 2

Montebello Plans to Add a Driving Range and Entertainment Facility to Its Golf Course, Near Its Two City-Owned Hotels and Event Center

Source: Montebello's website, financial statements, and driving range development agreement.

However, the city intends to renovate the golf course around the driving range and entertainment facility, citing the need to update aging infrastructure and shrink the course from an 18- to a 9-hole course to allow space for the new driving range and parking. Montebello's finance director estimated that funding this renovation could cost $10 million and require bond financing, which would be part of the $50 million in bond financing needed to pay for the driving range and entertainment facility. If so, the potential profitability of the overall project—the driving range and entertainment facility and the city's new, smaller course—would shrink as the city would have to pay this portion of the debt service costs, which the city has not yet calculated.

It remains to be seen whether or how quickly Montebello can implement these plans, and how much these changes will improve the golf course's finances, as the city may have to change its plans for the golf course to comply with surplus land requirements in state law. State law generally requires local governments, prior to selling or leasing surplus land to a third party, to first notify certain affordable housing developers that surplus land is available for potential construction of affordable housing, or face financial penalties. According to the city manager, the State recently informed the city that the portion of the golf course with the proposed driving range would qualify under this law. He said that the city worked with the State to see if alternative solutions were available; however, they were not able to identify any. Therefore, the city's plans for the golf course are on hold pending the outcome of this months-long process. Regardless, whether Montebello is able to move forward with its plans or will see affordable housing built on the property, the city has shown initiative in considering alternatives for the golf course and working to improve the course's operations.

The City Has Resolved Our Previous Concerns About Its Retirement Costs, Although Its Approach Has Created Ongoing Risk

Montebello has taken actions to control its retirement costs, but one of its chosen courses of action—borrowing to set aside funds to pay pension benefits—still has the potential to negatively affect the city's finances. In 2018 we found that Montebello's growing retirement costs could create a financial burden for the city in future years, and we recommended that it consider ceasing payment of some retirement costs. Montebello subsequently negotiated new contracts that shifted certain retirement costs to its employees—specifically, the city had been paying the share of costs usually paid by the employees. It also retained a financial analyst to assist with potential bond sale opportunities for the city, and in May 2020, it sold $153 million in pension obligation bonds (retirement bonds). Montebello used the proceeds to send a lump‑sum payment to its investment account at CalPERS in June 2020 to fund all existing obligations for promised benefits for employees.

Although retirement bonds have the potential to reduce the city's retirement expenses in the future by replacing them with debt payments, the Government Finance Officers Association (GFOA) and other financial experts have warned that such bonds have significant disadvantages that warrant careful consideration by an issuing entity. For example, CalPERS's investments may not perform as well as Montebello expects in the long term. If this occurs, the city may find itself again in a situation where it does not have enough funds to cover the benefits it owes and—in addition—would now have debt service related to the retirement bonds. In that situation, which Figure 3 illustrates, Montebello might need to seek additional revenue or cut other programs to be able to contribute enough new funds to its pension plan to make up for its investment losses, while also paying the mandatory debt service on its bonds.

Figure 3

A City's Invested Bond Proceeds Need to Grow Faster Than the Interest Rate on Its Pension Obligation Bonds

Source: Bond issuance documents and guidance from the GFOA website.

* Minimum needed growth is based on a city's interest rate for borrowing. Invested bond proceeds need to grow faster on average than the interest rate a city pays to ensure that it makes more money from investment gains than it loses from paying interest on its bonds.

In a 2014 review of retirement bond issuances nationwide, Boston College researchers found that the amount of money governments had saved by issuing bonds depended on the time period and market conditions. According to the researchers, many issuers had realized some savings from their bonds at the time of the review, but issuers from the late 1990s had experienced little or no benefits 15 years later. The researchers further noted that when an issuer such as Montebello is able to report that its pension plan is financially sound because of new funding from bond proceeds, the city council may experience increased political pressure to expand benefits for employees even though the city will still carry the bond debt for decades.

Montebello's finance director asserted that the city may not experience typical risks related to pension obligation bonds because it has a dedicated property tax for employee retirement that could help the city pay the bonds and avoid bond-related impacts to the general fund. Since 1946 the city has had a portion of its property tax allocated to city retirement costs. Nevertheless, taxpayers bear these risks, and if investment growth falls below the interest rate of the bonds, the city could have to pay more of its revenue for retirement expenses.

Montebello Continues to Make Questionable Decisions Related to Its Hotels

City Staff Have Not Provided the City Council With Analysis of the Performance of City‑Owned Hotels

Montebello owns two hotels and an event center, which includes a golf clubhouse. All of these properties are located on the city's golf course. The city has contracts with three separate companies—one for each hotel and one for certain portions of the event center—to manage or operate these facilities. Under these contracts, the city pays the companies an annual fee to manage the properties. In return, the city may receive revenue from the facilities, depending, in part, on the total revenue the companies generate from the facilities. The three companies are under common management by an individual whom we refer to as the hotel operator. City leadership has amended the contracts to manage these facilities several times, and one contract does not expire until 2064. In our 2018 audit, we identified that city leadership had exposed the city's general fund to significant financial risks through its hotels. In this report, we found that the city has continued to be lax in the oversight of its hotels.

The city's agreements with the hotel management companies give the companies responsibility for collecting hotel revenue, paying hotel expenses, and tracking and reporting on that activity. After the hotels' expenses are paid, the remaining revenue goes first to paying the bonds used to finance hotel construction and to certain reserves and administrative expenses, and then to paying the management companies' fees. Only after all of these expenses are paid can the city receive revenue. In 2018 we found that the city's general fund had yet to receive disbursements from the hotel in operation at that time, which opened nearly two decades ago.

Without detailed financial information about the performance of the city's two hotels, the city council has only limited ability to make informed financial decisions to protect the city's interests. Nonetheless, in our 2018 audit, we found that city staff were not reviewing the financial reports the city requires the hotel operator to submit. We recommended that, to protect the city's interests, its staff should routinely review information the hotel operator submits and should report to the city council at least annually on the performance of hotel operations.

Since we made our recommendation, city staff have presented a financial analysis of one of the city's two hotels to the city council just once, in January 2019. In this presentation, city staff identified several areas of concern, including the operator's failure to submit complete budget projections and the hotel's expenses growing faster than its revenue. The presentation implied that the city would receive cash flow from the hotels but stated that city staff would need to work with the hotel operator to clarify any inconsistencies before incorporating this information into future reports. However, according to the current finance director, the city did not complete any follow-up reports.

Although Montebello hired a consultant to examine the hotels' expenses, it is not clear that the city council ever saw the results or took action in response to them. During our 2018 audit, Montebello's acting city manager stated that the city lacked the hotel industry experience required to determine whether its hotels' expenses were reasonable. Following our audit, the city hired a consultant to compare its hotels' financial performance against a selection of comparable hotels. The consultant found that Montebello's hotels had similar room revenue but expenses at the higher end of the range of those of comparable hotels. Further, based on the consultant's findings, we calculated that the management fees of the two hotels were between 7 percent and 9 percent of revenue in 2018, above the average of about 3 percent for comparable hotels. The consultant provided its report to the city in May 2019—before Montebello hired its current city manager and finance director—but we could find no record that staff ever presented the results to the city council.

The current finance director said that city management believes that preparing specific reports on the performance of hotel operations is unnecessary because the city treats the hotels as it treats other enterprise operations—golf, water, and transit—and that it discusses all of these enterprise operations, along with the entire city's operating and capital budget, when necessary. This perspective is concerning because in 2018 we found problems related to both the golf and water enterprises. Without detailed financial information, the city council risks that it will not detect underperformance, errors, or misstatements in the hotels' finances and cannot protect Montebello's best interests when it considers matters related to its contracts for hotel operations.

The City Council Approved a Multimillion‑Dollar Loan for Hotel Renovations Without Properly Including It on a Council Agenda

In February 2020, the Montebello city council likely violated state law when it approved a loan from its general fund of up to $3.4 million for renovations at one of the hotels without notifying the public by putting the issue on the council agenda for public discussion and approval. Although state law generally prohibits the city council from discussing or taking action on any item not appearing on a posted agenda, it does allow for some exceptions. One such exception is when a city council determines by vote that there is a need to take immediate action and that the need for immediate action came to the attention of the local agency after it posted its agenda. The Montebello city council invoked this exception when it approved the loan for hotel renovations. However, the city council had been aware of the hotel's proposed renovations since at least November 2019, when it voted to refinance the hotel's bond and use the savings to offset expected renovation costs. In addition, according to the hotel operator, the city and the hotel operator discussed these renovations in January 2020, including discussing the likelihood that a loan would be necessary. Given that the city council meets twice a month and is able to call special meetings, we question why the city council did not postpone this issue to a subsequent meeting for which it could have provided proper public notice.

During the February 2020 meeting, the city council approved the loan for hotel renovations without any public discussion. In a report to the city council, city staff indicated that the loan was necessary for the hotel to complete significant renovations to remain in compliance with brand standards imposed by the franchise agreement with the particular hotel brand. However, based on our review of the video of the council meeting, the city council did not appear to make either the document authorizing the loan or the staff report describing the need for it available to the public at the meeting. Through its actions, the city council deprived Montebello's citizens and other stakeholders of their right to remain informed of the decisions of the city council and likely violated the State's open meeting laws.

Montebello's decision to loan general fund money without adequate public consideration and without analysis of the hotels' operations—an issue we discussed in the previous section—limited the city council's and the public's ability to assess the loan in the context of other city priorities. Such priorities should have included whether to preserve the funds to respond to unforeseen fiscal needs, such as the economic repercussions of the pandemic. According to the finance director and the hotel operator, the timing of the loan was fortuitous because the hotel operator was able to take advantage of a hotel shutdown caused by the pandemic to facilitate the renovations, which they assert saved $1 million. However, the city could not have known the extent of the pandemic in February 2020, and given additional information and public input, the council could have made, or at least publicly considered, different choices.

Montebello Has Not Adopted a Policy to Ensure Its Payment of Hotel Management Fees

Montebello still needs to strengthen its processes for paying the management fees that it owes to the two companies responsible for managing the city's hotels. These fees, which the city pays annually from collected hotel revenue, compensate the hotel management companies for services such as maintenance, marketing, and the hiring of hotel staff. In 2018 we found that Montebello had historically delayed payment of these annual management fees even when it had funds available to pay the fees promptly. As a result, the city had accrued $1.6 million in potentially avoidable interest expenses from 2002 through 2017, which the city eventually paid off.

After the audit, the city took steps to substantially eliminate its fee obligations: by June 2020, the remaining outstanding management fees for both hotels pertained to 2019 and 2020 only. In late 2020, during the pandemic, the city resumed its practice of delaying some payments, although the hotel operator offered to waive part of the interest due to one of the management companies. The city made payments toward its outstanding fees in August 2021; however, the finance director acknowledged that, as of September 2021, about $317,000 in deferred fees remained outstanding. The city is working to pay that, as well.

We are concerned that the city has not yet developed policies to ensure prompt payment, as we previously recommended. Instead, the current director of finance asserted that the city's existing hotel-related bond agreements already require it to pay fees when it has revenue available to do so, making an additional policy redundant. However, these agreements were unable to guarantee that Montebello promptly paid its fees in the past and might not prevent it from delaying fees again. Deferring fees and allowing interest to accrue when the means to pay the fees exist is wasteful. Thus, the city's management of the hotel maintenance fees remains an issue requiring monitoring.

Recommendations to Address These Risks

- To ensure public transparency and to provide the city council with the information necessary for making decisions regarding Montebello's hotels, city staff should routinely evaluate hotel operations by reviewing the financial information that the city requires the hotel operator to submit. By December 2021 and at least annually thereafter, city staff should report to the city council and the public on the performance of each hotel's operations, as well as the effect of the hotels on city finances.

- To fulfill its responsibility as the custodian of Montebello's limited resources and to provide increased transparency and opportunities for public involvement, the city council should ensure that it includes on the council meeting agenda all matters of fiscal policy it will consider during a public session, as state law requires, and that it discusses these matters in the public forum.

- To avoid accruing interest on hotel management fees, Montebello should immediately develop and adhere to a policy and process that requires it to pay management fees related to its two hotels in a timely manner.

Montebello Has Not Fully Resolved Problems With Its Procurement Processes

Montebello Has Not Followed Competitive Bidding Processes That Could Ensure That It Receives the Best Value When Procuring Services

Key Exceptions Under Which Competitive Bidding Is Not Required for Professional or Special Services Contracts

- If the service can only be obtained from one source

- If there is an emergency

- If the city council, by four-fifths vote, dispenses with bidding procedures because they are impractical, useless, or uneconomical and doing so would benefit the public welfare

Source: City of Montebello municipal code.

Despite some improvements to its contracting processes, the city still struggles to ensure that it is procuring services at the best possible value. In our 2018 audit, we found that Montebello had not sought competitive bids for certain contracts and that a former city manager had approved contracts that exceeded her approval authority. In 2019 the city council addressed several of our concerns by updating procurement requirements in the city's municipal code, in part by establishing, with limited exceptions, a requirement that the city advertise for competitive bids for professional or special services contracts with an annual value of $50,000 or more, and a process to contact three firms when procuring contracts with a value of less than that amount. The text box lists the allowed exceptions. However, our review of 12 contracts identified several in which the city did not follow its updated requirements or could have benefited from increased city council oversight and adherence to best practices. These findings, which Figure 4 summarizes, indicate that Montebello is still not ensuring that it obtains services at the best value.

Figure 4

When Entering Into Multiple Contracts, Montebello Did Not Follow Requirements or Best Practices

Source: Analysis of Montebello's contracts, city council agendas, and other procurement files.

For example, Montebello violated its municipal code by not soliciting formal bids for a large professional services contract related to its golf course, leaving it unable to demonstrate that the services it received were the best value to taxpayers. In February 2020, the city council approved a $90,000, three‑month contract for a new golf course operator without a formal competitive process, even though the city did not indicate that the service acquired met any of the exceptions to the threshold for competitive bidding of professional services specified in the municipal code. It later entered into a second contract with the same operator for $360,000, again without competitive bidding.

Montebello's municipal code allows the city to award professional or special services contracts without competition in certain circumstances. However, according to the finance director, the city did not formally use any of these exceptions as its justification for the golf course operator contract, although it could have. He stated that city staff believed there would be a shortage of qualified local vendors, they had limited time to enter into a new contract after reaching a settlement with their prior operator, and there was significant public interest in ensuring the golf course remained open. Nevertheless, by failing to follow the competitive process established in its municipal code, or properly documenting the rationale for its decision to contract with a vendor without competition, the city may have denied other potential vendors an opportunity to bid and reduced public assurance that the city received the best value for its money.

Further, as it did when it approved the hotel loan, the city council did not include the golf course contract on its published agenda for the meeting in question, likely violating the State's open meeting laws. As with the hotel loan, the city knew about the need for a golf course operator well in advance of the meeting; the city manager had assured residents that the golf course would have a new manager in a meeting two weeks prior. By omitting this issue from its agenda—as it did when it approved the hotel loan—the city limited the ability of residents to raise concerns about the contract. It is important that the city council follow legal requirements to only discuss or transact business that has been properly placed on the agenda; otherwise, state law allows the district attorney or any interested person to seek voidance of the council's actions that were not given appropriate notice.

We also identified instances in which Montebello did not document that it selected qualified vendors for smaller contracts, although it is taking steps to address this issue. The municipal code, with limited exceptions, requires the city to contact a minimum of three vendors for professional or special service contracts valued below $50,000 annually. However, for three such contracts we reviewed, the city's documentation did not clearly identify whether it had contacted three firms. After we brought these gaps to the attention of city staff, they were able to find and provide additional information indicating that the city complied with procurement requirements for two of these contracts. The current finance director asserted that city staff had historically been inconsistent in documenting their contact with multiple vendors and that its new staff were working to better document this and other steps in the procurement process. Staff members provided examples of templates with fields to indicate that the city had made contact with three vendors, and we verified that two 2021 contracts in our selection properly listed three firms. Without such documentation, the city may not be able to demonstrate that it is getting the best value for its smaller procurements.

Moreover, for two large office technology and support contracts totaling $1.2 million from 2020 and 2021, the city improperly used an alternative process that allows it to purchase supplies, equipment, or services by using the pricing and terms of a contract from another public entity or certain nonprofit associations for those same goods or services. The municipal code allows such a selection to occur without competitive bidding as long as the original purchase contract was the result of competitive bidding or negotiation, the purchase is made within two years of the competitive bid or negotiation, the purchase conforms with the city's specifications for the item or services, and the estimated price of the purchase using the original purchase contract is lower than the estimate for the purchase if made directly by the city. However, the purchase contract the city relied on for both of its agreements was from 2016, more than two years before the 2020 and 2021 office technology and support contracts. The city noted that the original contract had been extended into 2020. We could find no evidence that the extension included a renegotiation. More than two years had passed since the competitive bid or negotiation. As a result, the city likely violated its municipal code. Further, the city lacked assurance that this vendor still offered the best available value on the market; thus it should have either used a normal competitive process or found a more recent contract to serve as the originating contract.

In addition, the city still needs to ensure that contracts receive the appropriate level of approval and that it incorporates best practices when making procurements. For example, in 2019 the former city manager approved a contract for financial advising services with an estimated maximum value of $49,000 without city council approval, which the municipal code allows. However, from December 2019 through June 2020, Montebello authorized more than $90,000 in compensation to its adviser, an amount that otherwise would have required the contract to go before the city council.

According to the finance director, the city council had opportunities to review Montebello's relationship with this adviser because it received a report from the adviser and approved bond documentation that discussed the advising services. He further noted that it would have been difficult for the city to predict the amount of payments related to its eventual bond offerings when it first procured the adviser's contract. Nevertheless, given the adviser's role in assisting with bond transactions worth millions of dollars, the city should have anticipated that its contract for financial advising services would far exceed $49,000. Had it done so, the city would have benefited from input from the city council.

In a similar financial services procurement, the city did not follow GFOA recommendations when it selected its bond underwriter. The GFOA recommends that cities select bond underwriters—entities responsible for buying municipal bonds and reselling them to help cities secure lower debt costs—through a competitive process. However, city staff informed us that, based on its financial adviser's recommendation, Montebello informally selected its underwriter for several large issuances in 2019 and 2020, including the retirement bonds that we discuss previously. The city manager stated that although he would normally prefer to competitively procure an underwriter, the city determined at the time that identifying one quickly to take advantage of favorable market conditions for bond sales was more beneficial. Nonetheless, given that underwriters participate in municipal transactions worth tens or hundreds of millions of dollars, Montebello should have ensured that it followed best practices to competitively select its financing partners.

Montebello also still needs to develop a policy regarding how it will handle contracts with no maximum value. In 2018 we noted that Montebello's former city manager approved a franchise agreement with the hotel franchisor, without council approval, that did not have a value attached, but that could have cost the city a substantial sum in the future. Thus, we expected that it would have received council approval. We noted a small example of the city entering into another agreement without a maximum value when in 2019 the former city manager approved a revenue‑sharing services agreement for instructional fees between the city and an aquatics instructor with no maximum value in the contract and no evidence of city council approval. Although the total cost to the city for this particular contract is unlikely to be large, the city still lacks a process or code provision to handle such services agreements without maximum values. The finance director stated that it would be unusual for a city to require reporting such instructional contracts to the city council or to contain a maximum value because of the unpredictable nature of instructor fee collections. Nonetheless, despite the unpredictable nature of the fees, the city could still include a reasonable "not‑to‑exceed" amount in its contract with the instructor. In the rare case of an agreement that could not include a maximum value, the city could better strengthen its processes by adopting a policy to handle such agreements.

Finally, Montebello is not providing the procurement trainings we recommended in 2018, increasing the risk that its staff will not comply with its municipal code to obtain the best value for goods and services. In our 2018 audit, we identified a number of instances in which the city did not follow competitive bidding processes and did not adequately ensure that it received the best value for services. We recommended that the city provide annual training on procurement requirements for all staff involved in the procurement process. Montebello conducted a procurement training for its staff in 2018—during our previous audit—and in 2019, but it has not conducted similar trainings for all staff involved in the procurement process since that time. Instead, it has conducted brief trainings on budget and financial processes for a limited number of staff, including staff in its transit and fire units. Furthermore, these trainings were high-level and contained only limited information on procurement. In fact, the city could provide no evidence of training anyone in its public works department on its new public works procurement requirements.

According to the director of finance, some of the issues we identified regarding specific procurement requirements, such as the need to obtain bids, may stem from a lack of training. He stated that the city has had some staff turnover and that many staff who have been with the city for a long time may not be familiar with all of the new requirements. Although the director of finance provided copies of emails he sent to various city departments reminding them of procurement practices, these email reminders are not a substitute for in-depth training. Additional training for all staff involved in the procurement process would help to ensure that the city's contracts consistently comply with the municipal code and other requirements.

Although Montebello Implemented Petty Cash and Credit Card Policies, Its Staff Members Have Not Consistently Followed Them

Petty Cash

Although Montebello developed a petty cash policy in response to our 2018 audit, its staff members have not consistently adhered to it. Montebello maintains petty cash funds in several departments to reimburse staff for city-related purchases such as office supplies. In our 2018 audit, we found that Montebello's lack of strong policies regarding the use of petty cash, coupled with its poor control over these funds, allowed city staff to be reimbursed for purchases above the city's informal $100 limit and increased the risk of fraud and abuse. The State Controller's Office (State Controller) raised similar concerns about this practice in a report on Montebello in 2011. In March 2019, the city established a policy that prohibits purchases in excess of $100 unless authorized in writing, as well as prohibiting the splitting of purchases to circumvent this limit.

Nonetheless, when we reviewed the city's petty cash transactions, we found evidence of cost splitting to avoid the $100 limit. For example, in one instance, a city employee submitted two separate reimbursement forms, totaling $106, for separate transactions from the same retailer within one minute of each other. In several other instances, city employees submitted multiple petty cash requests for travel and training expenses totaling more than $100. In one such case, an individual submitted three petty cash requests—which totaled more than $100—at the same time for training expenses that took place over the course of a week. When we asked why this individual did not submit an expense claim, the deputy finance director said that the employee assigned to approve the claims may not have been properly trained on the rules—we note a lack of procurement training above—and should have directed the individual to submit a check request instead.

We also identified several petty cash purchases that were over the city's $100 limit and that did not receive approval before the city reimbursed the employees. We reviewed seven transactions that were more than $100 and found that all seven included the appropriate receipts and the finance director's or city manager's initials authorizing the petty cash use. However, in some cases, the purchases were not approved until the city had already reimbursed the employees for the expenses. Waiting until after the funds are spent to authorize a petty cash expenditure defeats the purpose of the policy, which is to ensure that employees use petty cash appropriately. If Montebello continues to allow the use of petty cash over its limit, it should ensure authorization for such expenditures before providing reimbursement.

Credit Cards

In 2018 we found that Montebello's lack of documented credit card policies and procedures had enabled its staff to use city credit cards without following proper purchasing protocols. We recommended that Montebello establish a clear, written credit card policy that outlined appropriate credit card use and the payment approval process. In March 2019, the city established a credit card purchasing policy that specifies positions that will have access to a credit card and that identifies individual card and transaction limits. It also outlines the circumstances under which employees may use city credit cards.

However, we found that city management and staff have not complied with this policy, in part because the city's finance department has established individual credit card limits that exceed the amounts the policy specifies for six of the city's 15 credit cards. For example, the police department has a $10,000 credit limit even though the policy specifies a $5,000 maximum for the chief of police. Similarly, an office manager for the city manager has a credit limit of $10,000, when the policy allows for a maximum of $2,500. According to the deputy director of finance, he increased the police department's and the office manager's limits because they were too low, preventing them from making necessary purchases for their departments. However, if the city's management believes that the limits for some of the departments are too low, it should update the policy rather than circumvent it. By increasing the card limits beyond what the policy specifies, the city has increased the risk that staff will violate its procurement policies and misuse funds.

In addition to cards with excessive limits, we also identified a number of purchases that exceeded the city's credit card transaction limits and municipal code procurement requirements. For example, the credit card policy sets a credit card transaction limit of $3,000 for each of the city's six directors, as well as its fire and police chiefs. Similarly, the city's municipal code requires that purchases totaling $3,000 or more be made with a purchase order or by check, with limited exceptions. However, the police department charged nearly $3,700 in May 2021 and $5,000 in June 2021 to pay for meeting and guest rooms for training at a nearby resort. Likewise, in May 2021, the human resources director used his city credit card to pay a vendor more than $3,300 for food for an employee picnic. According to the deputy director of finance, staff were able to exceed transaction limits because he was new to the bank's online credit card system and had not realized that the transaction limits had not been properly set. He stated that he has since set the limits according to the amounts in the policy and that the system should automatically reject charges over the limits in the future.

Gifts of Public Funds

Montebello's senior management also circumvented the city's credit card policies when it split transactions and made purchases that we think constituted gifts of public funds; however, after we brought this issue to Montebello's attention, city officials raised private funds to cover the cost of the gifts. In December 2020, the human resources director, finance director, and office manager together purchased nearly $6,000 in restaurant gift cards for holiday employee appreciation, splitting the purchase three ways to avoid the limits specified in the credit card policy and in the city's municipal code. In addition, the human resources director used his city credit card to purchase approximately $1,600 in mugs for holiday employee appreciation.

Expenditures by public entities constitute improper gifts of public funds if the expenditures do not serve a public purpose and are provided without consideration. The determination of whether an expenditure serves a public purpose must be made by the governing legislative body, or in this case, Montebello's city council. Absent such a determination, city officials have no authority to spend public funds in this manner. We reviewed the city council agendas and meeting minutes during the time leading up to the purchases and found no evidence that the city council discussed the purchase of gift cards and mugs for holiday employee appreciation or that such purchases served a public purpose. We also did not find that these purchases were connected to any of the city's purposes as set forth in its municipal code, and were provided without consideration. As such, we think these purchases violated the California Constitution, which prohibits gifts of public funds. When we brought these purchases to the city's attention, the city insisted it had not violated state law. However, on October 6, 2021, city officials provided evidence that the city had recently raised the full $7,600 from private individuals and businesses to reimburse these costs. Nevertheless, we think that at the time city officials made the decision to provide gift cards and mugs to employees, they were gifts of public funds.

Montebello's credit card policy makes both the city manager and the finance director responsible for its oversight. When these same individuals circumvent the policy, it reduces the value and authority of that policy. As of September 2021, the city is working to improve its credit card policies and processes, and provided draft documentation showing that it will ban transaction splitting, phase out departmental cards, and adjust the limits to meet current needs.

Absent effective oversight and accountability, the use of Montebello's credit cards has grown significantly, increasing the risk that staff could be misusing city funds. From May through July 2019, staff made about 50 purchases totaling $16,000 on average per month using the city's credit cards. However, from May through July 2021, staff used city credit cards to make purchases of more than $32,000 per month for a variety of goods and services, including travel, office supplies, subscriptions, and repairs. Further, the average number of purchases per month increased by over 150 percent—from 53 to 133.

This increase is likely in part the result of a lack of accountability for credit card use. Montebello's credit card policy authorizes specific individuals to use city credit cards with certain credit and transaction limits. Although some of these individuals do have city credit cards in their name, the city has also issued separate credit cards to its departments, making it more difficult to keep track of who is using them. Montebello also has no policy that requires staff to get approval before using the city's credit cards. According to the finance director, Montebello plans to eliminate its department credit cards and move to having only cards issued to specific individuals, who the city can then hold accountable for their spending. He also said that in light of the larger issues the city has addressed, this is a minor issue, and the city has a process to review and authorize all of the transactions from the monthly statements. Nevertheless, in our review we were able to identify an instance where a vendor charged a city credit card $3,600 for an $1,800 purchase. After we brought it to the staff's attention, the city sought and obtained a refund. Without increased oversight and monitoring, Montebello will have little assurance that staff are appropriately using city funds totaling hundreds of thousands of dollars per year.

Petty cash and credit card purchases may represent small dollar amounts at times, but the nature of these payment methods makes monitoring them more difficult and increases the risk of fraud. Credit cards are becoming a more common way to pay for goods and services, and the GFOA acknowledges that they are convenient. Nevertheless, there have been many cases nationally of credit cards being used as a tool to commit fraud. Similarly, petty cash—because it is held as cash—is less secure than other means of payment. The finance director is correct when he says that these issues are small relative to other issues the city faces; however, their inherent risk warrants providing these transactions with adequate scrutiny.

Montebello Is Making Progress in Addressing Its Low Salaries

In 2018 we found that Montebello had trouble hiring and retaining qualified staff members because it paid low starting salaries compared with neighboring cities. We recommended that it study its staffing levels, complete a salary survey, and increase salaries as necessary. In 2020 the city council approved new salary ranges for its director positions based in part on the ranges in comparable cities. The city also signed an agreement with a consultant for a staff classification and total compensation study. The consultant presented its results to the city council in July 2021.

Montebello plans to negotiate new labor agreements based on this study. However, the cost of implementing these new labor agreements may strain the city's resources. According to the human resources director, preliminary results from the study show that Montebello's salaries are well below the market. The human resources director explained that to remedy the situation, city management is considering three-year agreements with its bargaining units to incrementally move each job classification toward market-rate salaries and total compensation. Management estimates this effort will cost about $4.5 million over three years, with ongoing costs afterwards, which will put an additional strain on the city's limited financial resources and retirement funds. However, the increased salaries should reduce the risks associated with turnover and vacancies and improve the city's ability to hire qualified staff.

Recommendations to Address These Risks

To ensure that it obtains the best value when procuring services, Montebello should do the following:

- Create a policy by January 2022 requiring staff to document when a valid exception exists to the standard procurement requirements in its municipal code. The policy should require that staff report their rationale for using the exception to the requirements to the city council in a public meeting.

- Establish a policy by January 2022 that requires contracts to include a maximum value when feasible. The policy should require the city council to review and approve any agreement that binds the city financially and that does not include a maximum value.

To ensure that its staff understand and are aware of city and state law procurement requirements, Montebello should train all staff involved in procurement regarding these requirements by April 2022 and annually thereafter.

To mitigate the risk of error or fraud, Montebello should provide training at least annually to all staff to reinforce its petty cash policy. To reduce the possibility of abuse of the city's petty cash funds, the city should prohibit petty cash reimbursements that exceed the maximum set in policy.

To reduce the risk of fraud and abuse with its credit cards, Montebello should do the following by January 2022:

- Complete efforts to eliminate departmental credit cards and ensure that every credit card in use is issued to an individual.

- Adopt and adhere to a policy prohibiting splitting payments to avoid the credit card transaction limits and require city council approval for any transactions above the limits.

- Either adjust its credit card limits to align with its municipal code and credit card policy or update the municipal code and policy to meet its current needs.

- Ensure that appropriate controls are in place with the issuing bank to prevent individual transactions and total purchases from exceeding limits established in policy.

To ensure the city does not make gifts of public funds, the city should do the following:

- Prior to making any expenditure that benefits a city employee, city officer, or private party, the city should critically consider whether such expenditure constitutes a valid public purpose of the city, document the city council's deliberation and determination that the expenditure constitutes a valid public purpose for the city, and decline to authorize any expenditures that do not constitute a valid public purpose of the city.

- Revise its municipal code by December 31, 2021 to specify limitations on the types of expenditures the city will approve or authorize in the future to ensure that all city expenditures only serve a valid public purpose of the city. For example, it should prohibit the purchases of employee gifts with public funds.

- Obtain for the City Council and all employees authorized to make expenditures with city funds bi-annual legal and ethics training from an entity that is independent from and not affiliated with the city or the city council, such as from the Attorney General's Office or the District Attorney's Office, regarding the appropriate use of public funds and the prohibition on using public funds to make private gifts.

We conducted this audit under the authority vested in the California State Auditor by Government Code section 8543 et seq. and according to generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives, which are identified as the risk areas specified in the Scope and Methodology section of this report. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Respectfully submitted,

ELAINE M. HOWLE, CPA

California State Auditor

October 14, 2021

Appendix A

Scope, Methodology, and the Status of 2018 Risk Areas

In May 2018, the Joint Legislative Audit Committee (Audit Committee) approved a proposal by the California State Auditor (State Auditor) to perform an audit of Montebello under the local high-risk program. We published the results of our 2018 audit in a report titled City of Montebello: Its Structural Deficit and Poor Operational Processes Threaten the City's Financial Stability and Delivery of Public Services, Report 2018-802. For this follow‑up audit report required by state law, we assessed the progress Montebello has made in addressing the 12 risk areas we identified in the 2018 audit.

The following table shows the 12 risk areas and the methods we used to follow up on Montebello's progress. When we identify a risk area's recommendations as addressed, the city implemented the recommendations we made in 2018-802; however, the area may still present some risk and require monitoring, as we describe in this report. Partially addressed recommendations are those where we noted that the city implemented some of our recommendations in the risk area, but not all; we provide updated recommendations in this report. Pending risk areas are those where the city has not taken action or the city has taken action but the results are not yet known. Resolved refers to those areas where we no longer consider the risk area relevant; we describe the specific reason for these decisions in the middle column of the table. We will base subsequent assessments of Montebello on the revised risk areas presented in this report.

Montebello's Risk Areas From Report 2018-802 and the Methods Used to Evaluate Its Progress in Addressing Them

| Risk Area | Status of the 2018-802 Risk Area and Related Recommendations | Method to Evaluate Progress | |

|---|---|---|---|

| 1 | Montebello relied heavily on one-time revenue to balance its budget. |

— Partially addressed — We made no specific recommendations in this area in Report 2018-802 or in this report. While the city has a new revenue source and is less reliant on one-time revenue, the city's position on the local high-risk dashboard, which we describe in the report, indicates the city's financial condition remains an area of concern. |

Evaluated Montebello's audited financial statements and budgets to determine its financial condition, including how key financial indicators for the city changed on our local high-risk dashboard. |

| 2 | Montebello had not addressed its municipal golf course's increasing debt to the city's general fund. |

— Pending — Montebello addressed our recommendations in Report 2018-802, and we do not make additional recommendations; however, because the city has not finalized its plans for the golf course, it should continue to monitor and report on this risk area. |

|

| 3 | Montebello needed to sell its water system or secure alternative financing because necessary improvements risked burdening the city's general fund. |

— Pending — As of September 2021, a decision on the sale of the water district was still pending at the California Public Utilities Commission. |

Reviewed whether the city had taken action to sell its water system. We determined that the city has taken steps to initiate a sale, though the transaction must be approved by the State. |

| 4 | Montebello's retirement costs risked becoming a financial burden. |

— Addressed — Although we consider this area addressed, the city will continue to experience costs related to its bonds and retirement plans and should continue to monitor those costs carefully. |

Assessed risks related to the city's issuance of retirement bonds based on guidance from the GFOA, other financial experts, and the city's financial adviser. |

| 5 | Montebello's hotel bonds risked impairing the city's general fund. |

— Addressed — In response to our original concern, the city indicated that it did not intend to issue new lease revenue bonds and that it would have its adviser explore ways to reduce costs related to bonds. The city refinanced some of its lease revenue bonds in 2019 in consultation with its adviser, which we conclude is in line with our recommendation to avoid new lease revenue bonds. |

Reviewed the city's financial adviser's report on risks related to hotel bonds and assessed whether the city took action on any of the considerations in the report. |

| 6 | Montebello's mismanagement of hotel revenue cost the city at least $1.6 million. |

— Partially addressed — We make a recommendation related to the payment of management fees with hotel revenue. |

Obtained documentation on the city's outstanding unpaid management fees and interest to determine their balance. |

| 7 | Montebello did not ensure that it received the best value from its agreements with the hotel operator. |

— Partially addressed — We make a recommendation related to annual reports on the hotels' performance. |

Interviewed pertinent city staff and reviewed city council meeting agendas and minutes, hotel budget documents, and one hotel financial report the city prepared in response to our 2018 recommendations. |

| 8 | Montebello needed to do more to monitor the city manager's contracting activities. |

— Partially addressed — We make a recommendation related to appropriate contract approvals. |

Reviewed four contracts approved by the city manager from January 2019 through May 2021 and determined whether each contract amount was within the limits established by Montebello's municipal code, whether the contract contained a maximum value, and whether the city conducted the appropriate approval process for a contract of that value. |

| 9 | Montebello did not always follow competitive bidding processes and did not adequately ensure that it received the best value for services. |

— Partially addressed — We make recommendations related to competitive bidding and procurement training. |

|

| 10 | Montebello did not address some of the deficiencies identified by the State Controller in 2011. |

— Resolved — Because the State Controller report is 10 years old and because we evaluated similar internal control issues in other areas of this report, we consider this issue area resolved and will instead follow up on Montebello's progress based on the findings highlighted in this report. |

Interviewed city staff about Montebello's progress in addressing the State Controller's findings. Staff informed us that the city has not worked to specifically address some of the outstanding findings. |

| 11 | Montebello's poor control over its petty cash and its lack of credit card policies and procedures created risks for fraud. |

— Partially addressed — We make recommendations related to implementing petty cash and credit card policies. |

Interviewed pertinent city staff and reviewed city council meeting agendas and minutes, petty cash and credit card policies and procedures, petty cash logs and requests, credit card statements, and supporting documentation and receipts. We judgmentally selected 10 petty cash and five credit card transactions for additional testing for compliance with city policies. |

| 12 | Montebello's lack of consistent leadership and competitive salaries reduced the effectiveness of its departments. |

— Addressed — Although we consider this area addressed, Montebello will need to monitor how salary increases may affect its financial situation. |

Interviewed pertinent city staff and reviewed city council meeting agendas and minutes, a staffing survey presentation and preliminary data, and city agreements with bargaining units to support city activities in response to our 2018 recommendations. |

Source: Audit records.

Appendix B

The State Auditor’s Local High‑Risk Program

Government Code section 8546.10 authorizes the State Auditor to establish a local high‑risk program to identify, audit, and issue reports on local government entities that are at high risk for potential waste, fraud, abuse, or mismanagement or that have major challenges associated with their economy, efficiency, or effectiveness. Regulations that define high risk and describe the workings of the local high‑risk program became effective on July 1, 2015. Both the statute and regulations require that the State Auditor seek approval from the Audit Committee to conduct high-risk audits of local entities.

As we describe in our 2018 report, following an initial assessment and analysis, we sought and obtained approval from the Audit Committee to conduct an audit of Montebello in May 2018. In December 2018, we published the results of our audit, which concluded that Montebello was a high-risk entity because of the financial risks associated with its enterprise funds and long-term obligations, problematic hotel operations, contracting practices, and staffing deficiencies.

If we designate a local entity as high risk as a result of an audit, it must submit a corrective action plan. If it is unable to provide its corrective action plan in time for inclusion in the audit report, it must provide the plan no later than 60 days after the report's publication. It must then provide written updates every six months after the audit report's issuance regarding its progress in implementing the corrective action plan. This corrective action plan must outline the specific actions the entity will perform to address the conditions causing us to designate it as high risk and its proposed timing for undertaking those actions. We will remove the high-risk designation when we conclude that the entity has taken satisfactory corrective action. State law additionally requires that if the State Auditor determines that a local government entity is high risk, then the State Auditor shall issue an audit report at least once every three years with recommendations for improvement in the local government agency.

Response to the Audit

City of Montebello

September 27, 2021

Elaine M. Howle, CPA

California State Auditor

621 Capitol Mall, Suite 1200

Sacramento, CA 95814

①RE: City of Montebello, Response to State Auditor Report 2021-807

Dear Ms. Howle:

The City of Montebello has made tremendous positive progress in improving its operations and financial standing since the release of your office's audit in December, 2018 (Report 2018-802).

The City has eliminated its $153 million pension unfunded liability, Montebello voters approved a new transaction and use tax which produced $7.6 million in new tax revenue in FY 2020-21, we have made significant progress in right-sizing and improving Golf Course operations, we have established stability of executive management and have begun addressing inequities in salaries. In addition, the City was awarded the GFOA Award for Excellence in Budgeting for the first time in its 100 year history, we refinanced hotel bonds to save millions of dollars for taxpayers, and the City updated its municipal code to address deficiencies in purchasing guidelines. Furthermore, the City created and updated myriad policies to improve internal controls, we continue to evaluate our existing policies and Municipal Code for necessary updates, and have realized many more positive accomplishments in the past two years.

I am proud of the City Council's leadership role in recognizing the importance of remedying the risk areas identified in the 2018 audit. I am also proud of the City's employees who continue to work diligently every day to continue improving Montebello's operations to ensure precious taxpayer dollars are used wisely.

The City is committed to the path of improvement, and recognizes there is concurrence with your office on some recommendations contained in Report 2021-807. However, the City does dispute certain statements and representations of facts contained in this report. The following pages present our response to Report 2021-807, and highlights those areas of disagreement with various findings and observations contained therein along with areas of agreement.

②"Despite Progress in Some Areas, Montebello's Financial Stability Remains Uncertain"

"Montebello's Financial Situation Declines in FY 2019-20 but It Projects Improvement Over the Next Few Years"